Exchange-traded fund

An exchange-traded fund (ETF) is a type of investment fund and exchange-traded product, i.e. they are traded on stock exchanges.[1][2][3]

ETFs own financial assets such as stocks, bonds, currencies, futures contracts, and/or commodities such as gold bars. The list of assets that each ETF owns, as well as their weightings, is posted on the website of the issuer daily, or quarterly in the case of active non-transparent ETFs. Many ETFs provide some level of diversification compared to owning an individual stock.

An ETF divides ownership of itself into shares that are held by shareholders. Depending on the country, the legal structure of an ETF can be a corporation, trust, open-end management investment company, or unit investment trust.[4][5] The shareholders indirectly own the assets of the fund and are entitled to a share of the profits, such as interest or dividends, and they would be entitled to any residual value if the fund undergoes liquidation. They also receive annual reports. An ETF generally operates with an arbitrage mechanism designed to keep it trading close to its net asset value, although deviations can occur.[6]

The largest ETFs, which passively track stock market indices, have annual expense ratios as low as 0.03% of the amount invested, although specialty ETFs can have annual fees of 1% or more of the amount invested. These fees are paid to the ETF issuer out of dividends received from the underlying holdings or from selling assets.[7]

In the U.S., there are $5.4 trillion invested in equity ETFs and $1.4 trillion invested in fixed-income ETFs. In Europe, there is $1.0 trillion invested in equity ETFs and $0.4 trillion invested in fixed-income ETFs. In Asia, there are $0.9 trillion invested in equity ETFs and $0.1 trillion invested in fixed-income ETFs. In the first quarter of 2023, trading in ETFs accounted for 32% of the total dollar volume of stock market trading in the U.S., 11% of trading volume in Europe, and 13% of trading volume in Asia.[8]

In the U.S., the largest ETF issuers are BlackRock iShares with a 34% market share, The Vanguard Group with a 29% market share, State Street Global Advisors with a 14% market share, Invesco with a 5% market share, and Charles Schwab Corporation with a 4% market share.[9]

ETFs are regulated by governmental bodies (such as the U.S. Securities and Exchange Commission and the Commodity Futures Trading Commission in the United States) and are subject to securities laws (such as the Investment Company Act of 1940 and the Securities Exchange Act of 1934 in the United States).

Closed-end funds are not considered to be ETFs, even though they are funds and are traded on an exchange. Exchange-traded notes are debt instruments that are not exchange-traded funds.

ETFs vs. mutual funds

ETFs are similar in many ways to mutual funds, except that ETFs are bought and sold from other owners throughout the day on stock exchanges, whereas mutual funds are bought and sold from the issuer based on their price at day's end. ETFs are also more transparent since their holdings are generally published online daily and, in the United States, are more tax efficient than mutual funds.[10][11][12] Unlike mutual funds, ETFs trade on a stock exchange, can be sold short, can be purchased using funds borrowed from a stockbroker (margin), and can be purchased and sold using limit orders, with the buyer or seller aware of the price per share in advance.[13][14]

Costs and fees

Both ETFs and mutual funds charge annual expense ratios that range from 0.03% of the investment value to upwards of 1% of the investment value. Mutual funds generally have higher annual fees since they have higher marketing, distribution and accounting expenses (12b-1 fees).[15] ETFs are also generally cheaper to operate since, unlike mutual funds, they do not have to buy and sell securities and maintain cash reserves to accommodate shareholder purchases and redemptions.[16][17][18][19]

Stockbrokers may charge different commissions, if any, for the purchase and sale of ETFs and mutual funds. In addition, sales of ETFs in the United States are subject to transaction fees that the national securities exchanges must pay to the SEC under section 31 of the Securities Exchange Act of 1934, which, as of February 2023, is $8 per $1 million in transaction proceeds.[20] Many mutual funds can be bought commission-free from the issuer, although some charge front-end or back-end loads, while ETFs do not have loads at all.[21]

Taxation

In the United States, ETFs can be more attractive tax-wise than mutual funds for transactions made in taxable accounts. However, there are no tax benefits to ETFs compared to mutual funds in the United Kingdom and Germany.[22][23][24]

In the U.S., whenever a mutual fund realizes a capital gain that is not balanced by a realized loss (i.e. when the fund sells appreciated shares to meet investor redemptions), its shareholders who hold the fund in taxable accounts must pay capital gains taxes on their share of the gain.[25][26] However, ETF investors generally only realize capital gains when they sell their own shares for a gain.[27]

ETFs offered by The Vanguard Group are actually a different share class of its mutual funds and do not stand on their own; however, they generally do not have any adverse tax issues.[28][29][30][31]

Trading

ETFs can be bought and sold at current market prices at any time during the trading day, unlike mutual funds, which can only be traded at the end of the trading day. Also unlike mutual funds, investors can execute the same types of trades that they can with a stock, such as limit orders, which allow investors to specify the price points at which they are willing to trade, stop-loss orders, margin buying, hedging strategies, and there is no minimum investment requirement. ETFs can be traded frequently to hedge risk or implement market timing investment strategies, whereas many mutual funds have restrictions on frequent trading.[4][32]

Options, including put options and call options, can be written or purchased on most ETFs – which is not possible with mutual funds, allowing investors to implement strategies such as covered calls on ETFs. There are also several ETFs that implement covered call strategies within the funds.[33][34][35]

Many mutual funds must be held in an account at the issuing firm, while ETFs can be traded via any stockbroker. Some stockbrokers do not allow for automatic recurring investments or trading fractional shares of ETFs, while these are allowed by all mutual fund issues.[10]

The most popular ETFs such as those tracking the S&P 500 trade tens of millions of shares per day and have strong market liquidity, while there are many ETFs that do not trade very often, and thus might be difficult to sell compared to more liquid ETFs. The most active ETFs are very liquid, with high regular trading volume and tight bid-ask spreads (the gap between buyer and seller's prices), and the price thus fluctuates throughout the day. This is in contrast with mutual funds, where all purchases or sales on a given day are executed at the same price at the end of the trading day.

Categories of ETFs

- Index ETFs - Most ETFs are index funds: that is, they track the performance of an index generally by holding the same securities in the same proportions as a certain stock market index, bond market index or other economic index. Examples of large Index ETFs include the Vanguard Total Stock Market ETF (NYSE Arca: VTI), which tracks the CRSP U.S. Total Market Index, ETFs that track the S&P 500, which are issued by The Vanguard Group (NYSE Arca: VOO), iShares (NYSE Arca: IVV), and State Street Corporation (NYSE Arca: SPY), ETFs that track the NASDAQ-100 index (Nasdaq: QQQ), and the iShares Russell 2000 ETF (NYSE Arca: IWM), which tracks the Russell 2000 Index, entirely composed of companies with small market capitalizations. Other funds track indices of a certain country or include only companies that are not based in the United States; for example, the Vanguard Total International Stock Index ETF (NYSE Arca: VXUS) tracks the MSCI All Country World ex USA Investable Market Index, the iShares MSCI EAFE Index ETF (NYSE Arca: EFA) tracks the MSCI EAFE Index, and the iShares MSCI Emerging Markets ETF (NYSE Arca: EEM) tracks the MSCI Emerging Markets index. Some ETFs track a specific type of company, such as the iShares Russell 1000 Growth ETF (NYSE Arca: IWF), which tracks the "growth" stocks in the Russell 1000 Index. State Street Corporation has issued ETFs that track the components of the S&P 500 in each industry: for example, the Technology Select Sector SPDR Fund (NYSE Arca: XLK) tracks the components of the S&P 500 that are in the technology industry and The Financial Select Sector SPDR Fund, which tracks the components of the S&P 500 that are in the financial industry. The iShares Select Dividend ETF replicates an index of high dividend paying stocks.[40] Other indexes on which ETFs are based focus on specific niche areas, such as sustainable energy or environmental, social and corporate governance.[41] Most index ETFs invest 100% of their assets proportionately in the securities underlying an index, a manner of investing called replication. Some index ETFs such as the Vanguard Total Stock Market Index Fund, which tracks the performance of thousands of underlying securities, use representative sampling, investing 80% to 95% of their assets in the securities of an underlying index and investing the remaining 5% to 20% of their assets in other holdings, such as futures, option and swap contracts, and securities not in the underlying index, that the fund's adviser believes will help the ETF to achieve its investment objective.[42][43][44][45] Factor ETFs are index funds that use enhanced indexing, which combines active management with passive management in an attempt to beat the returns of an index. Factor ETFs tend to have slightly higher expense ratios and volatility than strictly passive index ETFs.[46][47][48] Synthetic ETFs, which are common in Europe but rare in the United States, are a type of index ETF that does not own securities but tracks indexes using derivatives and swaps. They have raised concern due to lack of transparency in products and increasing complexity; conflicts of interest; and lack of regulatory compliance.[49][50][51] A synthetic ETF has counterparty risk, because the counterparty is contractually obligated to match the return on the index. The deal is arranged with collateral posted by the swap counterparty, which arguably could be of dubious quality. These types of set-ups are not allowed under the European guidelines, Undertakings for Collective Investment in Transferable Securities Directive 2009 (UCITS).[52][53] Counterparty risk is also present where the ETF engages in securities lending or total return swaps.[54] The difference between the performance of an index fund and the index itself is called the tracking error; this difference is usually negative, except during flash crashes and other periods of extreme market turbulence, for index funds that do not use full replication, and for indices that consist of illiquid assets such as high-yield debt.[55][56][4][57][58]

- Actively managed ETFs include active management, whereby the manager executes a specific trading strategy instead of replicating the performance of a stock market index. The securities held by such funds are posted on their websites daily, or quarterly in the cases of active non-transparent ETFs. The ETFs may then be at risk from people who might engage in front running since the portfolio reports can reveal the manager's trading strategy. Some actively managed equity ETFs address this problem by trading only weekly or monthly.[59] The largest actively managed ETFs are the JPMorgan Equity Premium Income ETF (NYSE: JEPI), which charges 0.35% in annual fees, JPMorgan Ultra-Short Income ETF (NYSE: JPST), which charges 0.18% in annual fees, and the Pimco Enhanced Short Duration ETF (NYSE: MINT), which charges 0.36% in annual fees.[60]

- Thematic ETFs are ETFs, including both Index ETFs and actively managed ETFs, that focus on a theme such as disruptive technologies, climate change, shifting consumer behaviors, cloud computing, robotics, electric vehicles, the gig economy, e-commerce, or clean energy.[61][62]

- Bond ETFs are exchange-traded funds that invest in bonds.[63] Bond ETFs generally have much more market liquidity than individual bonds.[64]

- Commodity ETFs invest in commodities such as precious metals, agricultural products, or hydrocarbons such as petroleum and are subject to different regulations than ETFs that own securities.[65][66] Commodity ETFs are generally structured as exchange-traded grantor trusts, which gives a direct interest in a fixed portfolio. SPDR Gold Shares, a gold exchange-traded fund, is a grantor trust, and each share represents ownership of one-tenth of an ounce of gold.[67][68] Most commodity ETFs own the physical commodity. SPDR Gold Shares (NYSE Arca: GLD) owns over 40 million ounces of gold in trust,[69] iShares Silver Trust (NYSE Arca: SLV) owns 18,000 tons of silver,[70] Aberdeen Standard Physical Palladium Shares (NYSE Arca: PALL) owns almost 200,000 ounces of palladium,[71] and Aberdeen Standard Physical Platinum Shares ETF (NYSE Arca: PPLT) owns over 1.1 million ounces of platinum.[72] However, many ETFs such as the United States Oil Fund by United States Commodity Funds (NYSE Arca: USO) only own futures contracts,[73] which may produce quite different results from owning the commodity. In these cases, the funds simply roll the delivery month of the contracts forward from month to month. This does give exposure to the commodity, but subjects the investor to risks involved in different prices along the term structure, such as a high cost to roll.[74][75] They can also be index funds tracking commodity indices.

- Currency ETFs enable investors to invest in or short any major currency or a basket of currencies. They are issued by Invesco and Deutsche Bank among others. Investors can profit from the foreign exchange spot change, while receiving local institutional interest rates, and a collateral yield.[76]

- Leveraged ETFs (LETFs) and Inverse ETFs, use investments in derivatives to seek a daily return that corresponds to a multiple of, or the inverse (opposite) of, the daily performance of an index.[77] For example, Direxion offers leveraged ETFs and inverse exchange-traded funds that attempt to produce 3x the daily result of either investing in (NYSE Arca: SPXL) or shorting (NYSE Arca: SPXS) the S&P 500.[78][79][80][81][82] To achieve these results, the issuers use various financial engineering techniques, including equity swaps, derivatives, futures contracts, and rebalancing, and re-indexing.[83] The rebalancing and re-indexing of leveraged ETFs may have considerable costs when markets are volatile. Leveraged ETFs effectively increase exposure ahead of a losing session and decrease exposure ahead of a winning session.[83][84] The rebalancing problem is that the fund manager incurs trading losses because he needs to buy when the index goes up and sell when the index goes down in order to maintain a fixed leverage ratio.[85][86][87][88][89]

Arbitrage mechanism

ETF shares are created and redeemed when large broker-dealers called authorized participants (AP) act as market makers and purchase and redeem ETF shares directly from the ETF issuer in large blocks, generally 50,000 shares, called creation units. Purchases and redemptions of the creation units are generally in kind, with the AP contributing or receiving securities of the same type and proportion held by the ETF; the lists of ETF holdings are published online.[66]

The ability to purchase and redeem creation units gives ETFs an arbitrage mechanism intended to minimize the potential deviation between the market price and the net asset value of ETF shares. APs provide market liquidity for the ETF shares and help ensure that their intraday market price approximates the net asset value of the underlying assets.[66] Other investors, such as individuals using a retail broker, trade ETF shares on the secondary market.

If there is strong investor demand for an ETF, its share price will temporarily rise above its net asset value per share, giving arbitrageurs an incentive to purchase additional creation units from the ETF issuer and sell the component ETF shares in the open market. The additional supply of ETF shares reduces the market price per share, generally eliminating the premium over net asset value. A similar process applies when there is weak demand for an ETF: its shares trade at a discount from their net asset value.

When new shares of an ETF are created due to increased demand, this is referred to as "ETF inflows." When ETF shares are converted into the component securities, this is referred to as "ETF outflows."[90]

ETFs are dependent on the efficacy of the arbitrage mechanism in order for their share price to track net asset value.

History

ETFs had their genesis in 1989 with Index Participation Shares (IPS), an S&P 500 proxy that traded on the American Stock Exchange and the Philadelphia Stock Exchange. This product was short-lived after a lawsuit by the Chicago Mercantile Exchange was successful in stopping sales in the United States.[91][92][93] The argument against the IPS approach was that it resembled a futures contract because the investments held an index, rather than holding the actual underlying stocks.[94]

In 1990, a similar product, Toronto Index Participation Shares, which tracked the TSE 35 and later the TSE 100 indices, started trading on the Toronto Stock Exchange (TSE) in 1990. The popularity of these products led the American Stock Exchange to try to develop something that would satisfy regulations by the U.S. Securities and Exchange Commission.[95]

Nathan Most and Steven Bloom, under the direction of Ivers Riley, and with the assistance of Kathleen Moriarty,[96] designed and developed Standard & Poor's Depositary Receipts (NYSE Arca: SPY), which were introduced in January 1993.[97][98][99] Known as SPDRs or "Spiders", the fund became the largest ETF in the world. In May 1995, State Street Global Advisors introduced the S&P 400 MidCap SPDRs (NYSE Arca: MDY).

It is a frequent topic in the financial press that ETFs have a quick growth. These popular funds, with assets more than doubling each year since 1995 (as of 2001), have been warmly embraced by most advocates of low–cost index funds. Vanguard is the leading advocate of index funds.[100]

Barclays, in conjunction with MSCI and Funds Distributor Inc., entered the market in 1996 with World Equity Benchmark Shares (WEBS), which became iShares MSCI Index Fund Shares. WEBS originally tracked 17 MSCI country indices managed by the funds' index provider, Morgan Stanley. WEBS were particularly innovative because they gave casual investors easy access to foreign markets. While SPDRs were organized as unit investment trusts, WEBS were set up as a mutual fund, the first of their kind.[101][102]

In 1998, State Street Global Advisors introduced "Sector Spiders", separate ETFs for each of the sectors of the S&P 500.[103] Also in 1998, the "Dow Diamonds" (NYSE Arca: DIA) were introduced, tracking the Dow Jones Industrial Average. In 1999, the influential "cubes" was launched, with the goal of replicate the price movement of the NASDAQ-100 – originally QQQQ but later Nasdaq: QQQ.

The iShares line was launched in early 2000. By 2005, it had a 44% market share of ETF assets under management.[104] Barclays Global Investors was sold to BlackRock in 2009.

In 2001, The Vanguard Group entered the market by launching the Vanguard Total Stock Market ETF (NYSE Arca: VTI), which owns every publicly traded stock in the United States.[105] Some of Vanguard's ETFs are a share class of an existing mutual fund.

iShares issued the first bond funds in July 2002: iShares IBoxx $ Invest Grade Corp Bond Fund (NYSE Arca: LQD), which owns corporate bonds, and a TIPS fund.[106] In 2007, iShares introduced an ETF that owns high-yield debt and an ETF that owns municipal bonds and State Street Global Advisors and The Vanguard Group also issued bond ETFs.

In December 2005, Rydex (now Invesco) launched the first currency ETF, the Euro Currency Trust (NYSE Arca: FXE), which tracked the value of the Euro.[107][108] In 2007, Deutsche Bank's db x-trackers launched the EONIA Total Return Index ETF in Frankfurt tracking the Euro. In 2008, it launched the Sterling Money Market ETF (LSE: XGBP) and US Dollar Money Market ETF (LSE: XUSD) in London. In November 2009, ETF Securities launched the world's largest FX platform tracking the MSFXSM Index covering 18 long or short USD ETC vs. single G10 currencies.[109]

The first leveraged ETF was issued by ProShares in 2006.[77]

In 2008, the SEC authorized the creation of ETFs that use active management strategies.[66] Bear Stearns launched the first actively managed ETF, the Current Yield ETF (NYSE Arca: YYY), which began trading on the American Stock Exchange on March 25, 2008.[110][111][112]

In December 2014, assets under management by U.S. ETFs reached $2 trillion.[113] By November 2019, assets under management by U.S. ETFs reached $4 trillion.[114][115][116] Assets under management by U.S. ETFs grew to $5.5 trillion by January 2021.[117]

In August 2023, a three-judge US court panel for the District of Columbia Court of Appeals in Washington overruled an SEC decision denying Grayscale Investments permission to launch a bitcoin-focused ETF. The court's decision sets the path for a first bitcoin exchange-traded fund in the US.[118][119]

In October 2023, three U.S. investment managers launched the first ETFs tied to the value of Ethereum.[120]

History of Gold ETFs

The first gold exchange-traded product was Central Fund of Canada, a closed-end fund founded in 1961. It amended its articles of incorporation in 1983 to provide investors with a product for ownership of gold and silver bullion. It has been listed on the Toronto Stock Exchange since 1966 and the American Stock Exchange since 1986.[121]

The idea of a gold ETF was first conceptualized by Benchmark Asset Management Company Private Ltd in India, which filed a proposal with the Securities and Exchange Board of India in May 2002. In March 2007 after delays in obtaining regulatory approval.[122] The first gold exchange-traded fund was Gold Bullion Securities launched on the ASX in 2003, and the first silver exchange-traded fund was iShares Silver Trust launched on the NYSE in 2006. SPDR Gold Shares, a commodity ETF, is in the top 10 largest ETFs by assets under management.[123]

Effects on price stability

Purchases and sales of commodities by ETFs can significantly affect the price of such commodities.[124][125]

Per the International Monetary Fund, "some market participants believe the growing popularity of exchange-traded funds (ETFs) may have contributed to equity price appreciation in some emerging economies and warn that leverage embedded in ETFs could pose financial stability risks if equity prices were to decline for a protracted period."[50]

ETFs can be and have been used to manipulate market prices, such as in conjunction with short selling that contributed to the United States bear market of 2007–2009.[126]

New regulations to force ETFs to be able to manage systemic stresses were put in place following the 2010 flash crash, when prices of ETFs and other stocks and options became volatile, with trading markets spiking and bids falling as low as a penny a share [127] in what the Commodity Futures Trading Commission (CFTC) investigation described as one of the most turbulent periods in the history of financial markets.[128][129]

These regulations proved inadequate to protect investors in the August 24, 2015, flash crash,[127] "when the price of many ETFs appeared to come unhinged from their underlying value." "ETFs were consequently put under even greater scrutiny by regulators and investors."[127] Analysts at Morningstar, Inc. claimed in December 2015 that "ETFs are a "digital-age technology" governed by "Depression-era legislation."[127]

Perception and adoption of ETFs in the European market

The first European ETF came on the market in 2000, and the European ETF market has seen tremendous growth since. At the end of March 2019, the asset under management in the European industry stood at €760bn, compared with an amount of €100bn at the end of 2008.[130] The market share of ETFs has increased significantly in recent years. At the end of March 2019, ETFs accounted for 8.6% of total AUM in investment funds in Europe, up from 5.5% five years earlier.[130]

The use of ETFs has also evolved over time, as shown by regular observations of investment professionals’ practices in Europe.[131] EDHEC surveys show an increasing propagation of ETF adoption over the years, especially for traditional asset classes. While ETFs are now used across a wide spectrum of asset classes, in 2019, the main use is currently in the area of equities and sectors, for 91% (45% in 2006 [132]) and 83% of the survey respondents, respectively. This is likely to be linked to the popularity of indexing in these asset classes as well as to the fact that equity indices and sector indices are based on highly liquid instruments, which makes it straightforward to create ETFs on such underlying securities. The other asset classes for which a large share of investors declare using ETFs are commodities and corporate bonds (68% for them both, to be compared with 6% and 15% in 2006, respectively), smart beta-factor investing, and government bonds (66% for them both, to be compared with 13% for government bonds in 2006). Investors have a high rate of satisfaction with ETFs, especially for traditional asset classes. In 2019, we observed 95% satisfaction for both equities and government bond assets.

The role of ETFs in the asset allocation process

Over the years, EDHEC survey results have consistently indicated that ETFs are used as part of a truly passive investment approach, mainly for long-term buy-and-hold investment rather than tactical allocation. However, over the past three years, the two approaches have gradually become more balanced, and, in 2019, European investment professionals declared that their use of ETFs for tactical allocation is actually greater than for long-term positions (53% and 51%, respectively).

ETFs, which originally replicated broad market indices, are now available in a wide variety of asset classes and a multitude of market sub-segments (sectors, styles, etc.). If gaining broad market exposure remains the main focus of ETFs for 73% of users in 2019, 52% of respondents will use ETFs to obtain specific sub-segment exposure. The diversity of ETFs increases the possibilities of using ETFs for tactical allocation. Investors can easily increase or decrease their portfolio exposure to a specific style, sector, or factor at a lower cost with ETFs. The more volatile the markets are, the more interesting it is to use low-cost instruments for tactical allocation, especially since cost is a major criterion for selecting an ETF provider for 88% of respondents.

Expectations for ETF future developments in Europe

Despite the high current adoption rate of ETFs and the already high maturity of this market, a high percentage of investors (46%) still plan to increase their use of ETFs in the future, according to the EDHEC 2019 survey responses. Investors are planning to increase their ETF allocation to replace active managers (71% of respondents in 2019), but they are also seeking to replace other passive investing products through ETFs (42% of respondents in 2019). Lowering costs is the main motivation for increasing the use of ETFs for 74% of investors. Investors are especially demanding further developments of ETF products in the areas of ethical, SRI, and smart beta equity and factor indices. In 2018, ESG ETFs enjoyed growth of 50%, reaching €9.95bn, with the launch of 36 new products, compared to just 15 in 2017.[130] However, 31% of the EDHEC 2019 survey respondents still require additional ETF products based on sustainable investment, which appears to be their top concern.

Investors are also demanding ETFs related to advanced forms of equity indices, namely those based on multi-factor and smart beta indices (30% and 28% of respondents, respectively), and 45% of respondents would like to see further developments in at least one category related to smart beta equity or factor indices (smart beta indices, single-factor indices, and multi-factor indices). Consistent with the desire to use ETFs for passive exposure to broad market indices, only 19% of respondents show any interest in the future development of actively managed equity ETFs.

Notable issuers of ETFs

- AdvisorShares: issues actively managed ETFs only, majority owned by Fund.com

- ARK Investment Management: issues actively managed ETFs that invest in companies involved in disruptive innovation

- Banco Itau: issues ETFs in Brazil

- BetaShares: issues ETFs in Australia

- Bips Investment Managers: issues Bips (Beta Investment Performance Securities) in South Africa

- BlackRock: issues iShares

- BNP Paribas: issues EasyETFs in Europe

- Boost ETP: issues short (inverse) and leveraged exchange-traded products including 3X equity and commodity products in Europe

- Charles Schwab Corporation: issues ETFs

- Deutsche Bank: issues Xtrackers ETFs, and manages PowerShares DB commodity- and currency-based ETFs

- ETF Securities: issues ETFs primarily in Australia

- Franklin Templeton Investments: Issues LibertyShares® ETFs

- Global X Funds: issues ETFs

- Guggenheim Partners: issues specialty Guggenheim Funds ETFs

- Indo Premier Investment Management: issues Premier ETFs in Indonesia Stock Exchange

- Invesco: issues Invesco ETFs, as well as BLDRS based on American depositary receipts

- Lyxor Asset Management: issues Lyxor ETFs in France

- Natixis Investment Managers: issues Active International Minimum Volatility ETF (MVIN) and Active Short Duration Income ETF (LSST)

- Standard Life Aberdeen: issues commodity ETFs

- State Street Global Advisors: issues SPDRs

- The Vanguard Group: issues Vanguard ETFs, formerly known as VIPERs

- United States Commodity Funds: issues commodity ETFs such as the United States Oil Fund

- WisdomTree Investments: issues specialty ETFs

See also

- Exchange for ETF (EFETF) – a method in which market makers exchange their ETFs for futures contracts.

- Exchange-traded note (ETN)

- List of American exchange-traded funds

References

- "ETFs 101". Fidelity Investments.

- "Exchange-Traded Funds (ETFs)". U.S. Securities and Exchange Commission.

- "Add an ETF without breaking the bank". The Vanguard Group.

- "Actively Managed Exchange-Traded Funds - SEC Release No. IC-25258, 66 Fed. Reg. 57614". November 8, 2001. Archived from the original on May 3, 2017. Retrieved August 27, 2017.

- "SPDR ETFs: Basics of Product Structure". State Street Global Advisors. July 30, 2014. Archived from the original on February 20, 2017.

- "17 CFR Parts 239, 270, and 274 Exchange-Traded Funds; Proposed Rule" (PDF). U.S. Securities and Exchange Commission. March 18, 2008. Archived from the original (PDF) on July 6, 2017. Retrieved August 27, 2017.

- "ETF Fees: How are They Deducted & How Much Do They Cost?". SoFi. January 15, 2021.

- "Global ETF Market Facts". BlackRock.

- "Market share of largest providers of Exchange Traded Funds (ETFs) in the United States". Statista.

- "ETFs vs. mutual funds". Charles Schwab Corporation.

- "Benefits of ETFs". Fidelity Investments.

- "Benefits and considerations of ETFs". Charles Schwab Corporation.

- Keller, Burton (August 5, 2019). "Are Active ETFs a Threat to Mutual Funds?". ThinkAdvisor.

- Boyte-White, Claire (March 5, 2020). "The Right Time to Change From Mutual Funds to ETFS". Investopedia.

- "ETFs vs. mutual funds: Cost comparison". Fidelity Investments.

- "How ETFs Work" (PDF). WisdomTree Investments.

- "ETF vs. Mutual Funds: What Are the Differences?". Entrepreneur. January 26, 2023.

- "ETFs vs. Mutual Funds: What's the difference?". TD Bank.

- Kenton, Will; Kim, Paul (May 26, 2022). "ETFs and mutual funds can instantly diversify your portfolio, but they differ in how they're traded, managed and taxed". Business Insider.

- "New Rate for Fees Paid Under Section 31 of the Exchange Act". Financial Industry Regulatory Authority. February 14, 2023.

- Iachini, Michael (January 28, 2020). "ETF vs. Mutual Fund: It Depends on Your Strategy". Charles Schwab Corporation.

- Lodge, Steve (April 16, 2010). "Are ETF dividends taxed differently?". Financial Times. Archived from the original on December 10, 2022.

- "Stocks and Shares ISA: A low cost and tax-efficient way to invest". The Vanguard Group.

- "Ultimate Guide to Private Pension Plans in Germany". www.horizon65.com. March 16, 2023. Retrieved March 16, 2023.

- Wallace, Karen (December 5, 2019). "What You Need to Know About Capital Gains Distributions". Morningstar, Inc.

- McGowan, Lee (July 7, 2020). "What Are Mutual Fund Capital Gains Distributions?". Dotdash.

- Iachini, Michael (August 6, 2019). "ETFs and Taxes: What You Need to Know". Charles Schwab Corporation.

- Johnson, Ben (January 15, 2020). "Vanguard's Unique ETF Structure Presents Unique Tax Risks". Morningstar, Inc.

- Mider, Zachary R.; Massa, Annie; Cannon, Christopher (May 1, 2019). "Vanguard Patented a Way to Avoid Taxes on Mutual Funds". Bloomberg News.

- "System and method for supporting a new financial instrument for use in closed end funds". 1997 – via Google Patents.

- Johnson, Ben; Benz, Christine (April 11, 2018). "Should You Worry About the Tax Efficiency of Vanguard ETFs?". Morningstar, Inc.

- Gastineau, Gary (2002). The Exchange-Traded Funds Manual. Wiley. p. 227. ISBN 978-0-471-21894-4.

- Nibley, Brian (March 5, 2021). "Pros and Cons of a Covered Call ETF—and When to Buy". SoFi.

- Heinzl, John (July 25, 2014). "Don't be tempted by covered call ETF yields". The Globe and Mail.

- "It's Looking Like a Fine Time to Consider Covered Call ETFs". Nasdaq. July 23, 2021.

- "SEC Adopts New Rule to Modernize Regulation of Exchange-Traded Funds" (Press release). U.S. Securities and Exchange Commission. September 26, 2019.

- Peirce, Hester (May 21, 2019). "A Quarter Century of Exchange-Traded Fun!". U.S. Securities and Exchange Commission.

- Riquier, Andrea (January 31, 2020). "What is a 'non-transparent' ETF, and why would anyone want to own one?". MarketWatch.

- "ETF Education: How Transparent Are ETFs?". ETF.com. January 22, 2018.

- "Banner Year of Dividend Growth Sends Cash to Dividend ETFs". Yahoo! Finance. January 7, 2015. Archived from the original on March 5, 2016.

- "Sector-Fund Investing". Morningstar, Inc. Archived from the original on February 1, 2014.

- Burns, Scott (October 28, 2009). "Our Take on the Bond ETF Dilemma". Morningstar, Inc.

- Fuller, Stacy L. (April 16, 2008). "The Evolution of Actively Managed Exchange-Traded Funds" (PDF). Review of Securities & Commodities Regulation.

- "Frequently Asked Questions About ETF Basics and Structure". Investment Company Institute.

- "How Vanguard Index Funds Work". Investopedia.

- "'Enhanced' Index ETFs That Are Outperforming the S&P 500". ETFtrends.com. Yahoo! Finance. July 7, 2013.

- "Fidelity ETFs". Fidelity Investments.

- "iSHARES FACTOR ETFs". iShares.

- "Potential financial stability issues arising from recent trends in Exchange-Traded Funds (ETFs)". Financial Stability Board. April 2011.

- "Global Financial Stability Report: Durable Financial Stability: Getting There from Here". International Monetary Fund. April 2011.

- Ramaswamy, Srichander (April 2011). "Market structures and systemic risks of exchange-traded funds. Working paper 343" (PDF). Bank for International Settlements.

- "Synthetic Exchange-Traded Fund: What it is, How it Works". Investopedia. August 23, 2022.

- Grill, Michael; Lambert, Claudia; Marquardt, Philipp; Watfe, Gibran; Weistroffer, Christian (November 2018). "Counterparty and liquidity risks in exchange-traded funds". European Central Bank.

- Hurlin, Christophe; Iseli, Grégoire; Perignon, Christophe; Yeung, Stanley (July 6, 2014). "The Counterparty Risk Exposure of ETF Investors". SSRN. SSRN 2462747.

{{cite journal}}: Cite journal requires|journal=(help) - Avellaneda, Marco; Zhang, Stanley (April 13, 2011). "Path-Dependence of Leveraged ETF Returns" (PDF). SIAM Journal of Financial Math. pp. 586–603. Archived (PDF) from the original on June 10, 2013.

- Guo, Kevin; Leung, Tim (2015). "Understanding the Tracking Errors of Commodity Leveraged ETFs". SSRN. Fields Institute Communications. 74: 39–63. arXiv:1610.09404. doi:10.1007/978-1-4939-2733-3_2. ISBN 978-1-4939-2732-6. SSRN 2389411.

- Salisbury, Ian (November 21, 2008). "Some ETFs Fall Short on Pricing; Certain Trades Slip Below Value of Holdings". The Wall Street Journal.

- Salisbury, Ian (February 19, 2010). "ETFs Were Wider Off the Mark in 2009". The Wall Street Journal.

- Hoffman, David (April 21, 2008). "Active ETFs are, well, less active; Dynamics of trading translate into little active management". Investment News. Archived from the original on January 9, 2015. Retrieved August 20, 2020.

- Greifeld, Katherine (April 25, 2023). "JPMorgan Overthrows JPMorgan for Crown of Largest Actively Managed ET". Bloomberg News.

- Liu, Evie (July 31, 2020). "Thematic ETFs Invest in the Hottest Trends. How Not To Get Burned". Barron's.

- Shin, Melissa (February 12, 2020). "Where do thematic funds fit in a portfolio?". Advisor's Edge.

- Chen, James (May 13, 2020). "Bond ETF". Investopedia.

- Norris, Emily (January 25, 2018). "Bond ETFs: A Viable Alternative". Investopedia.

- "CFTC Issues COVID-19 Customer Advisory on Commodity ETPs and Funds" (Press release). Commodity Futures Trading Commission. May 22, 2020.

- "17 CFR Parts 239, 270, and 274 Exchange-Traded Funds; Proposed Rule" (PDF). U.S. Securities and Exchange Commission. March 18, 2008. Archived from the original (PDF) on July 6, 2017. Retrieved August 27, 2017.

- "SPDR® GOLD TRUST 2016 Grantor Trust Tax Reporting Statement" (PDF). SPDR Gold Shares.

- Ferri, Rick (May 12, 2014). "Exchange-Traded Confusion". Forbes.

- "Key information". SPDR Gold Shares.

- "iShares Silver Trust". iShares.

- "Aberdeen Standard Physical Palladium Shares ETF and ETFS Physical Platinum". Standard Life Aberdeen.

- "Aberdeen Standard Physical Platinum Shares ETF". Standard Life Aberdeen.

- "Portfolio". United States Oil Fund.

- Lauricella, Tom (November 2, 2009). "Gold Mutual Funds Vs. Gold ETFs: It Depends on the Goal". The Wall Street Journal. Archived from the original on January 9, 2015.

- Kay, Bradley (August 25, 2009). "The Future of Commodity ETFs". Morningstar, Inc. Archived from the original on September 27, 2011.

- Chen, James (November 7, 2019). "Currency ETF". Investopedia.

- Spence, John (May 29, 2006). "ProFunds readies first leveraged ETFs - ETF Investing". MarketWatch.

- "SPXL SPXS". Direxion.

- Chen, James (July 21, 2020). "Inverse ETF". Investopedia.

- Reeves, Jeff (April 15, 2020). "10 Inverse ETFs to Buy". U.S. News & World Report.

- "Inverse ETFs". Fidelity Investments.

- Kennedy, Mark (March 11, 2020). "What to Know Before Buying Inverse and Short ETFs". Dotdash.

- Bojinov, Stoyan (April 24, 2015). "Leveraged ETF Rebalancing: An ETFdb.com Guide". ETFdb.com.

- Maxey, Daisy (August 4, 2009). "Fidelity the Latest to Caution on ETFs". The Wall Street Journal. Archived from the original on March 7, 2015.

- Yates, Tristan (April 16, 2020). "Dissecting Leveraged ETF Returns". Investopedia.

- Leung, Tim; Sircar, Ronnie (September 25, 2014). "Implied Volatility of Leveraged ETF Options". Applied Mathematical Finance. 22 (2): 162–188. doi:10.1080/1350486X.2014.975825. S2CID 218146570. SSRN 2164518.

- Hunnicutt, Trevor (May 2, 2017). "U.S. SEC approves request to list quadruple-leveraged ETFs". Reuters.

- "SEC reconsiders approval of quadruple leveraged ETF: sources". Reuters. May 16, 2017. Archived from the original on December 12, 2017.

- Michaels, Dave; Dieterich, Chris (May 16, 2017). "Quadruple-Levered ETF? SEC Hits Pause on Its Approval of an Exotic Investment". The Wall Street Journal.

- "A Primer on ETF Primary Trading and the Role of Authorized Participants" (PDF). BlackRock. March 2017.

- Gastineau, Gary (2002). The Exchange-Traded Funds Manual. Wiley. p. 32. ISBN 978-0-471-21894-4.

- Berman, David (February 19, 2017). "The Canadian investment idea that busted a mutual-fund monopoly". The Globe and Mail.

- Coumarianos, John (February 3, 2020). "ETFs Not Reflecting Net Asset Value is a Feature, Not a Bug". Barron's.

- Eichenwald, Kurt (October 26, 1989). "Index-Participation Appeal Declined". The New York Times. Retrieved May 8, 2022.

- McFeat, Tom (December 29, 2010). "The rise of the ETF". CBC News. Retrieved January 31, 2020.

- Greifeld, Katie (December 20, 2022). "Kathleen Moriarty, ETF Industry's 'SPDR Woman,' Dies at 69". MSN. Bloomberg News.

- Carrel, Lawrence (September 9, 2008). ETFs for the Long Run. Wiley. ISBN 9780470138946. ISBN 978-0-470-13894-6

- Bayot, Jennifer (December 10, 2004). "Nathan Most Is Dead at 90; Investment Fund Innovator". The New York Times. Archived from the original on November 5, 2012.

- "S&P Depositary Receipts Start Trading on Amex / BRIEFCASE / The International Herald Tribune". The New York Times. January 30, 1993. Retrieved May 8, 2022.

- Gastineau, Gary L. (April 30, 2001). "Exchange-Traded Funds: An Introduction". The Journal of Portfolio Management. 27 (3): 88–96. doi:10.3905/jpm.2001.319804. ISSN 0095-4918. S2CID 260586913.

- Wiandt, Jim; McClatchy, William (2002). Exchange Traded Funds. Wiley. p. 82. ISBN 0-471-22513-4.

- Fabozzi, Frank (2003). The Handbook of Financial Instruments. Wiley. p. 532. ISBN 0-471-22092-2.

- Burke, John (October 19, 2018). "How State Street Could Reclaim the ETF Throne".

- Moore, Rebecca (June 7, 2006). "ETFs Show Increasing Popularity in First Half of 2005". PlanSponsor.

- "Vanguard Total Stock Market ETF (VTI)". The Vanguard Group.

- "iShares Bond Funds". U.S. Securities and Exchange Commission.

- Spence, John (June 8, 2005). "First currency ETF filed". MarketWatch.

- Martin, Neil A. (July 7, 2008). "Putting the World at Your Fingertips". The Wall Street Journal.

- Kaminska, Izabella (November 13, 2009). "Introducing collateralised currency securities (updated)". Financial Times.

- "Bear Stearns Announces the Launch of the First Actively Managed Exchange Traded Fund" (Press release). Business Wire. March 10, 2008.

- "Bear Stearns Announces the Start of Trading of the First Actively Managed Exchange Traded Fund" (Press release). PR Newswire. March 25, 2008.

- Jaffe, Chuck (April 27, 2008). "Bear Stearns Current Yield (YYY)". The Seattle Times.

- Weinberg, Ari I. (January 5, 2015). "Another Milestone-Leaping Year for ETFs". The Wall Street Journal.

- Gurdus, Lizzy (November 9, 2019). "ETF assets rise to record $4 trillion and top industry expert says it's still 'early days'". CNBC.

- Horch, AJ (May 29, 2020). "Here's why investors started pouring trillions into exchange-traded funds". CNBC.

- Greifeld, Katherine; Ballentine, Claire (June 17, 2020). "Crisis Lessons Drowned Out as $4 Trillion ETF Market Booms". Bloomberg News.

- Rekenthaler, John (January 21, 2021). "Farewell, Mutual Funds". Morningstar, Inc.

- Morrow, Allison (August 29, 2023). "Crypto assets soar as US court clears a path for bitcoin ETFs | CNN Business". CNN. Retrieved August 29, 2023.

- Lang, Hannah (August 29, 2023). "US court says SEC wrong to deny Grayscale's spot bitcoin ETF proposal". Reuters. Retrieved August 29, 2023.

- VanEck, ProShares, Bitwise launch ETFs tied to ether futures | Yahoo! Finance

- "CENTRAL FUND CLOSES APPROXIMATELY US$57 MILLION SHARE ISSUE" (PDF) (Press release). Central Fund of Canada. March 5, 2008.

- "Benchmark, UTI MF get Sebi nod for gold ETFs". The Economic Times. January 18, 2007.

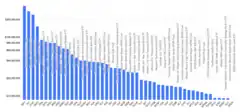

- "Largest ETFs: Top 100 ETFs By Assets". ETFdb.

- McCrank, John (April 28, 2011). "ETF Edge-Rise of gold ETFs raises concern of price collapse". Reuters.

- Ivanov, Stoyu I. (July 2011). "The influence of ETFs on the price discovery of gold, silver and oil". Journal of Economics and Finance.

- "5 Common Misconceptions About ETFs". Investopedia.

- Weinberg, Ari I. (December 6, 2015). "Should You Fear the ETF? ETFs are scaring regulators and investors: Here are the dangers—real and perceived". The Wall Street Journal. Archived from the original on December 7, 2015.

- Kirilenko, Andrei; Kyle, Albert S.; Samadi, Mehrdad; Tuzun, Tugkan (May 5, 2014), The Flash Crash: The Impact of High Frequency Trading on an Electronic Market (PDF), archived (PDF) from the original on April 2, 2015.

- Ackerman, Andrew; Krouse, Sarah (September 21, 2015). "SEC Takes Aim at Risk in Asset Management". The Wall Street Journal.

- "A Guided Tour of the European ETF Market Place (April)". Morningstar, Inc. April 2019.

- Le Sourd, Veronique; Martellini, Lionel (September 2019). "The EDHEC European ETF, Smart Beta and Factor Investing Survey 2019". EDHEC-Risk Institute.

- Amenc, Noël; Giraud, Jean-René; Goltz, Felix; Le Sourd, Véronique; Martellini, Lionel; Ma, Xiaoyan (October 2006). "The EDHEC European Survey 2006. EDHEC-Risk Institute (October)". EDHEC-Risk Institute.

Further reading

- Carrell, Lawrence. ETFs for the Long Run: What They Are, How They Work, and Simple Strategies for Successful Long-Term Investing. Wiley, September 9, 2008. ISBN 978-0-470-13894-6

- Ferri, Richard A. The ETF Book: All You Need to Know About Exchange-Traded Funds. Wiley, January 4, 2011. ISBN 0-470-53746-9

- Humphries, William. Leveraged ETFs: The Trojan Horse Has Passed the Margin-Rule Gates. 34 Seattle U.L. Rev. 299 (August 31, 2010), available at Seattle University Law Review.

- Koesterich, Russ. The ETF Strategist: Balancing Risk and Reward for Superior Returns. Penguin Books, May 29, 2008. ISBN 978-1-59184-207-1

- Lemke, Thomas P.; Lins, Gerald T. & McGuire, W. John. Regulation of Exchange-Traded Funds. LexisNexis, 2015. ISBN 978-0-7698-9131-6

External links

- A brief history of ETFs – Trackinsight

- Exchange Traded Funds (ETF) – Australian Stock Exchange (ASX)

- Exchange Traded Funds (ETF) – Johannesburg Stock Exchange (JSE)

- Exchange Traded Funds (ETF) – London Stock Exchange (LSE)

- Exchange Traded Funds (ETF) – Toronto Stock Exchange (TSX)

- Exchange Traded Products – New York Stock Exchange

- Funds + ETFs – NASDAQ Stock Market

- The ETF Hall of Fame: 25 People Who Revolutionized the ETF Industry – ETF Database

- What are ETFs? – Trackinsight