Low-volatility anomaly

In investing and finance, the low-volatility anomaly is the observation that low-volatility stocks have higher returns than high-volatility stocks in most markets studied. This is an example of a stock market anomaly since it contradicts the central prediction of many financial theories that taking higher risk must be compensated with higher returns.

Furthermore, the Capital Asset Pricing Model (CAPM) predicts a positive relation between the systematic risk-exposure of a stock (also known as the stock beta) and its expected future returns. However, some narratives of the low-volatility anomaly falsify this prediction of the CAPM by showing that stocks with higher beta have historically under-performed the stocks with lower beta.[1]

Other narratives of this anomaly show that even stocks with higher idiosyncratic risk are compensated with lower returns in comparison to stocks with lower idiosyncratic risk.[2]

The low-volatility anomaly has also been referred to as the low-beta, minimum-variance, minimum volatility anomaly.

History

The CAPM was developed in the late 1960s and predicts that expected returns should be a positive and linear function of beta, and nothing else. First, the return of a stock with average beta should be the average return of stocks. Second, the intercept should be equal to the risk-free rate. Then the slope can be computed from these two points. Almost immediately these predictions were empirically challenged. Studies find that the correct slope is either less than predicted, not significantly different from zero, or even negative.[3][1] Economist Fischer Black (1972) proposed a theory where there is a zero-beta return which is different from the risk-free return.[4] This fits the data better. It still presumes, on principle, that there is higher return for higher beta. Research challenging CAPM's underlying assumptions about risk has been mounting for decades.[5] One challenge was in 1972, when Michael C. Jensen, Fischer Black and Myron Scholes published a study showing what CAPM would look like if one could not borrow at a risk-free rate.[6] Their results indicated that the relationship between beta and realized return was flatter than predicted by CAPM.[7] Shortly after, Robert Haugen and James Heins produced a working paper titled “On the Evidence Supporting the Existence of Risk Premiums in the Capital Market”. Studying the period from 1926 to 1971, they concluded that "over the long run stock portfolios with lesser variance in monthly returns have experienced greater average returns than their ‘riskier’ counterparts".[8][9]

Evidence

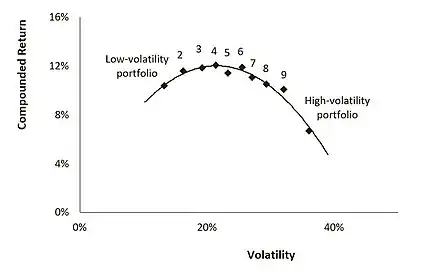

The low-volatility anomaly has been documented in the United States over an extended 90-year period. Volatility-sorted portfolios containing deep historical evidence since 1929 are available in an online data library[10] The picture contains portfolio data for US stocks sorted on past volatility and grouped into ten portfolios. The portfolio of stocks with the lowest volatility has a higher return compared to the portfolio of stocks with the highest volatility. A visual illustration of the anomaly, since the relation between risk and return should be positive. Data for the related low-beta anomaly is also online available. The evidence of the anomaly has been mounting due to numerous studies by both academics and practitioners which confirm the presence of the anomaly throughout the forty years since its initial discovery in the early 1970s. The low-volatility anomaly is found across sectors, but also within every sector.[11] Examples include Baker and Haugen ( 1991),[12] Chan, Karceski and Lakonishok (1999),[13] Jagannathan and Ma (2003),[14] Clarke De Silva and Thorley, (2006)[15] and Baker, Bradley and Wurgler (2011).[16] Besides evidence for the US stock market, there is also evidence for international stock markets. For global equity markets, Blitz and van Vliet (2007),[17] Nielsen and Subramanian (2008),[18] Carvalho, Xiao, Moulin (2011),[19] Blitz, Pang, van Vliet (2012),[20] Baker and Haugen (2012),[21] all find similar results.[22][23][24]

Explanations

Several explanations have been put forward to explain the low-volatility anomaly. They explain why low risk securities are more in demand creating the low-volatility anomaly.

- Constraints: Investors face leverage constraints and shorting constraints. This explanation was put forward by Brennan (1971) and tested by Frazzini and Pederson (2014).[25]

- Relative performance: Many investors want to consistently beat the market average, or benchmark as discussed by Blitz and van Vliet (2007) and Baker, Bradley, and Wurgler (2011).

- Agency issues: Many professional investors have misaligned interests when managing client money. Falkenstein (1996) and Karceski (2001) give evidence for mutual fund managers.

- Skewness preference: Many investors like lottery-like payoffs. Bali, Cakici and Whitelaw (2011) test the ‘stocks as lotteries’ hypothesis of Barberis and Huang (2008).

- Behavioral biases. Investors are often overconfident and use the representative heuristic and overpay for attention grabbing stocks.[26]

For an overview of all explanations put forward in the academic literature also see the survey article on this topic by Blitz, Falkenstein, and Van Vliet (2014) and Blitz, Van Vliet, and Baltussen (2019).[27][28]

Also see

References

- van der Grient, Bart; Blitz, David; van Vliet, Pim (July 1, 2011). "Is the Relation between Volatility and Expected Stock Returns Positive, Flat or Negative?". Rochester, NY. doi:10.2139/ssrn.1881503. S2CID 153743404. SSRN 1881503.

{{cite journal}}: Cite journal requires|journal=(help) - Ang, Andrew; Hodrick, Robert J.; Xing, Yuhang; Zhang, Xiaoyan (2006). "The Cross-Section of Volatility and Expected Returns" (PDF). The Journal of Finance. 61 (1): 259–299. doi:10.1111/j.1540-6261.2006.00836.x. ISSN 1540-6261. S2CID 1092843.

- Fama, Eugen (1973). "Risk, return, and equilibrium: Empirical tests". Journal of Political Economy. 81 (3): 607–636. doi:10.1086/260061. S2CID 13725978.

- Black, Fischer (1972). "Capital market equilibrium with restricted borrowing". The Journal of Business. 45 (3): 444–455. doi:10.1086/295472.

- Arnott, Robert, (1983) “What Hath MPT Wrought: Which Risks Reap Rewards?,” The Journal of Portfolio Management, Fall 1983, pp. 5–11; Fama, Eugene, Kenneth French (1992), “The Cross-Section of Expected Stock Returns”, Journal of Finance, Vol. 47, No. 2, June 1992, pp. 427- 465; see Roll, Richard, S.A. Ross, (1994), “On the Cross-Sectional Relation Between Expected Returns and Betas”, Journal of Finance, March 1994, pp. 101–121; see Ang, Andrew, Robert J. Hodrick, Yuhang Xing & Xiaoyan Zhang (2006), “The cross section of volatility and expected returns”, Journal of Finance, Vol. LXI, No. 1, February 2006, pp. 259–299; see also Best, Michael J., Robert R. Grauer (1992), “Positively Weighted Minimum-Variance Portfolios and the Structure of Asset Expected Returns”, The Journal of Financial and Quantitative Analysis, Vol. 27, No. 4 (Dec., 1992), pp. 513–537; see Frazzini, Andrea and Lasse H. Pedersen (2010) “Betting Against Beta” NBER working paper series.

- Black, Fischer; Jensen, Michael (1972). "The capital asset pricing model: Some empirical tests". Studies in the Theory of Capital Markets. 81 (3): 79–121.

- Jensen, Michael C., Black, Fischer and Scholes, Myron S.(1972), “The Capital Asset Pricing Model: Some Empirical Tests”, Studies in the theory of Capital Markets, Praeger Publishers Inc., 1972; see also Fama, Eugene F., James D. MacBeth, “Risk, Return, and Equilibrium: Empirical Tests”, The Journal of Political Economy, Vol. 81, No. 3. (May – Jun., 1973), pp. 607–636.

- Haugen, Robert A., and A. James Heins (1975), “Risk and the Rate of Return on Financial Assets: Some Old Wine in New Bottles.” Journal of Financial and Quantitative Analysis, Vol. 10, No. 5 (December): pp.775–784, see also Haugen, Robert A., and A. James Heins, (1972) “On the Evidence Supporting the Existence of Risk Premiums in the Capital Markets”, Wisconsin Working Paper, December 1972.

- Haugen, Robert A., and A. James Heins, (1972) “On the Evidence Supporting the Existence of Risk Premiums in the Capital Markets”, Wisconsin Working Paper, December 1972.

- Van Vliet, Pim; de Koning, Jan (2017). High returns from low risk: a remarkable stock market paradox. Wiley. doi:10.1002/9781119357186. ISBN 9781119351054.

- De Carvalho, Raul Leote; Zakaria, Majdouline; Lu, Xiao; Moulin, Pierre (January 1, 2015), Jurczenko, Emmanuel (ed.), "11 - Low-Risk Anomaly Everywhere: Evidence from Equity Sectors", Risk-Based and Factor Investing, Elsevier, pp. 265–289, ISBN 978-1-78548-008-9, retrieved August 18, 2023

- R. Haugen, and Nardin Baker (1991), “The Efficient Market Inefficiency of Capitalization-Weighted Stock Portfolios”, Journal of Portfolio Management, vol. 17, No.1, pp. 35–40, see also Baker, N. and R. Haugen (2012) “Low Risk Stocks Outperform within All Observable Markets of the World”.

- Chan, L., J. Karceski, and J. Lakonishok (1999), “On Portfolio Optimization: Forecasting Covariances and Choosing the Risk Model”, Review of Financial Studies, 12, pp. 937–974.

- Jagannathan R. and T. Ma (2003). “Risk reduction in large portfolios: Why imposing the wrong constrains helps”, The Journal of Finance, 58(4), pp. 1651–1684.

- Clarke, Roger, Harindra de Silva & Steven Thorley (2006), “Minimum-variance portfolios in the US equity market”, Journal of Portfolio Management, Fall 2006, Vol. 33, No. 1, pp.10–24.

- Baker, Malcolm, Brendan Bradley, and Jeffrey Wurgler (2011), “Benchmarks as Limits to Arbitrage: Understanding the Low-Volatility Anomaly”, Financial Analyst Journal, Vol. 67, No. 1, pp. 40–54.

- Blitz, David C., and Pim van Vliet. (2007), The Volatility Effect: Lower Risk without Lower Return, Journal of Portfolio Management, vol. 34, No. 1, Fall 2007, pp. 102–113. SSRN: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=980865

- Nielsen, F and R. Aylur Subramanian, (2008), “Far From the Madding Crowd – Volatility Efficient Indexes”, MSCI Research Insight.

- Carvalho, Raul Leote de, Lu Xiao, and Pierre Moulin,(2011) “Demystifying Equity Risk-Based Strategies: A Simple Alpha Plus Beta Description”, The Journal of Portfolio Management”, September 13, 2011.

- Blitz, David, Pang, Juan and Van Vliet, Pim, “The Volatility Effect in Emerging Markets” (April 10, 2012). Available at SSRN: http://ssrn.com/abstract=2050863.

- Baker, Nardin and Haugen, Robert A., “Low Risk Stocks Outperform within All Observable Markets of the World” (April 27, 2012). Available at SSRN: http://ssrn.com/abstract=2055431

- "Low Risk, High Return? - May 2014 - SagePoint Financial" (PDF). SagePoint Financial. Archived from the original (PDF) on May 4, 2015.

- "Why Low Beta Stocks Are Worth a Look". Portfolio Investing Blog: Portfolioist. Archived from the original on June 6, 2014.

- "The Greatest Anomaly in Finance: Low-Beta Stocks Outperform". Investing Daily. Archived from the original on May 31, 2014.

- Frazzini, Andrea and Pedersen, Lasse (2014). Betting against beta. Journal of Financial Economics, 111(1), 1-25.

- Blitz, David; Huisman, Rob; Swinkels, Laurens; Van Vliet, Pim (2019). "Media Attention and the Volatility Effect". Finance Research Letters. forthcomin. doi:10.2139/ssrn.3403466. hdl:1765/120091. S2CID 198634762.

- Blitz, David; Falkenstein, Eric; Van Vliet, Pim (2014). "Explanations for the Volatility Effect: An Overview Based on the CAPM Assumptions". The Journal of Portfolio Management. 40 (3): 61–76. doi:10.3905/jpm.2014.40.3.061. S2CID 201375041.

- Blitz, David; Van Vliet, Pim; Baltussen, Guido (2019). "The Volatility Effect Revisited". doi:10.2139/ssrn.3442749. S2CID 202931436.

{{cite journal}}: Cite journal requires|journal=(help)