Passbook

A passbook or bankbook is a paper book used to record bank or building society transactions on a deposit account.

Traditionally, a passbook was used for accounts with a low transaction volume, such as savings accounts. A bank teller or postmaster would write the date, amount of the transaction and the updated balance and enter his or her initials by hand. In the late 20th century, small dot matrix or inkjet printers were introduced that were capable of updating the passbook at the account holder's convenience, either at an automated teller machine or a passbook printer, either in a self-serve mode, by post, or in a branch.

History

Passbooks appeared in the 18th century, allowing customers to hold transaction information in their own hands for the first time. Until then, transactions were recorded in ledgers at the bank only, so customers had no history of their own deposits and withdrawals.

The passbook, which was around the size of a passport, ensured that customers had control over their own information, and was called a "passbook" because it was used as a way to identify the account holder without needing further identification. It also regularly passed between the bank and the account holder for updating.[1]

.jpg.webp)

Usage

Credits and deposits

To add credit to an account by bringing cash to a bank in person, the account holder can fill a small credit slip or deposit slip. The total value of notes and coins is counted and entered on the slip, along with the date and the payer's name. The cash and details are counted and checked by the teller at the bank; if everything is in order, the deposit is credited to the account, the credit slip is then kept by the bank, and the credit slip booklet is stamped with the date and then returned to the account holder. An account holder uses his passbook to record their history of transactions with his bank.

Debits and withdrawals

Withdrawals normally required the account holder to visit the branch where the account was held, where a debit slip or withdrawal slip would be prepared and signed. If the teller did not know the account holder, the signature on the slip and the authorities would be checked against the signature card at the branch, before money was paid out. In the 1980s, banks adopted the black light signature system for passbooks, which enabled withdrawals to be made from passbooks at a branch other than the one where an account was opened, unless prior arrangements were made to transfer the signature card to the other branch. Under this system, the passbook's owner would sign in the back of the passbook in an invisible ink and the signing authorities would also be noted. At the paying branch, the signature on the withdrawal slip would be checked against the signature in the book, which required a special ultraviolet reader to read.[2] Today, the customer is more commonly verified by PIN and commonly through an automated teller machine.

Direct banking

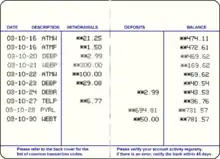

For people who feel uneasy with telephone or online banking, the use of a passbook is an alternative to obtain, in real-time, the account activity without waiting for a bank statement. However, unlike some bank statements, some passbooks offer fewer details, replacing easy-to-understand descriptions with short codes.[1]

Gallery of passbooks

- Passbook gallery

Saffron Building Society passbook

Saffron Building Society passbook German Postsparbuch, cover

German Postsparbuch, cover German Postsparbuch

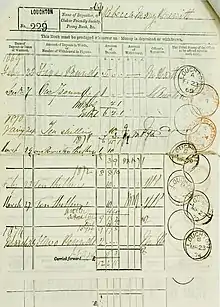

German Postsparbuch Bank account book, issued by Petty and Postlethwaite for use in Cumbria, UK. 1st entry 1831, last entry in 1870. On display at the British Museum in London.

Bank account book, issued by Petty and Postlethwaite for use in Cumbria, UK. 1st entry 1831, last entry in 1870. On display at the British Museum in London..jpg.webp) Steitz Savings and Loan Association Mortgage Loan Passbook (1987)

Steitz Savings and Loan Association Mortgage Loan Passbook (1987)

See also

- Bank statement

- Cheque book

- Deposit account

- Sberkassa, the bankbook heritage from the Soviet Union

References

- "Back to the future' savings passbook trumps the internet". The Telegraph. June 12, 2012.

- "Commonwealth Bank – The School Bank (1951)". Australia Screen. Retrieved 23 December 2012.