Stock-flow consistent model

Stock-flow consistent models (SFC) are a family of macroeconomic models based on a rigorous accounting framework, which guarantees a correct and comprehensive integration of all the flows and the stocks of an economy. These models were first developed in the mid-20th century but have recently become popular, particularly within the post-Keynesian school of thought.[1][2] Stock-flow consistent models are in contrast to dynamic stochastic general equilibrium models, which are used in mainstream economics.

Background and history

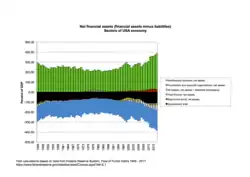

The ideas for an accounting approach to macroeconomics go back to Knut Wicksell,[3] John Maynard Keynes (1936)[4] and Michał Kalecki.[5][6] The accounting framework behind stock-flow consistent macroeconomic modelling can be traced back to Morris Copeland's development of flow of funds analysis back in 1949.[1][7] Copeland wanted to understand where the money to finance increases in Gross National Product came from, and what happened to unspent money if GNP declined. He developed a set of tables to show the relationship between flows of income and expenditure and changes to the stocks of outstanding debt and financial assets held in the US economy.[1][8]

James Tobin and his collaborators used features of stock-flow consistent modelling including the social accounting matrix and discrete time to develop a macroeconomic model that integrated financial and non-financial variables.[1] He outlined the following distinguishing features of his approach in his Nobel lecture[9]

- Modelling changes between discrete short-run time periods rather than a long run equilibrium

- Tracking changes in stocks of assets held by different groups

- Multiple assets with different rates of return,

- Modelling of monetary policy operations

- Subjecting the demand functions to "adding up constraints"

Also Robert Clower based his Keynesian price and business cycle theories on stock-flow relations.[10][11][12] A similar approach was developed in Germany by Wolfgang Stützel as Balances Mechanics.[13]

.jpg.webp)

The current SFC models mainly emerged from the separate economic tradition of the Post Keynesians, Wynne Godley being the most famous contributor in this regard.[1] Godley argued in favour of wider adoption of stock-flow consistent methods, expressing the view that they would improve the transparency and logical coherence of most macro models.[14] The Post Keynesians aimed at developing a macroeconomic theory that rejects the classical dichotomy, the neutrality of money and general equilibrium theory. Instead, they wanted to model the financial stocks and flows and their relations, the sectoral balances.[2][15][16]: 18 [17] From some models of "monetary circuit theory", far-reaching consequences were derived, such as the thesis of a "monetary growth imperative", which, however, could be explained by inconsistent accounting.[18][19] By respecting accounting constraints, "black holes" have to be avoided, where money vanishes without an offsetting entry in the balance sheet.[20][21]

The models gained popularity at the beginning of the 21st century and especially after the beginning of the financial crisis of 2007–08,[1] as some authors had foreseen the critical developments with accounting models.[22][23] Wynne Godley, one of the pioneers of the SFC approach since the 1970s,[22][24] had warned since 2000 in publications[25][26] that the US housing market would weaken and cause a recession.[22] In DSGE models, which dominate macroeconomics, crises usually cannot arise because of behavioural assumptions such as rational expectations and intertemporal optimisation. Although they treat stock and flow variables consistently, they usually model only individual stock variables such as physical capital, while monetary variables such as credit relations and debt are neglected.[23][27] Therefore, attempts are made to analyse financial crises using stock-flow consistent models based on the accounting approach.[28][29][30]

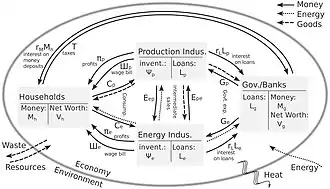

While ecological aspects were not considered by post-Keynesian authors like Godley or Lavoie, SFC models are now widely used within Ecological Macroeconomics.[5] In addition to cash flows, resource or energy flows and stocks or an ecosystem with renewable resources are modeled.[31][32][33][34] References are made in particular to the flow-fund models of Nicholas Georgescu-Roegen.[32][34] Other approaches[1] integrate concepts of SFC models into agent-based modeling (ABM)[5][35][36] or input–output models.[31][37]

Current researchers in the SFC approach to macroeconomic modelling are based in University of Limerick, Levy Economics Institute and University of Oxford.

Structure of the models

SFC models usually consist of two main components: an accounting part and a set of equations describing the laws of motion of the system. The consistency of the accounting is ensured by the use of three matrices: i) the aggregate balance sheets, with all the initial stocks, ii) the transaction flow, recording all the transactions taking places in the economy (e.g. consumption, interests payments); iii) the stock revaluation matrix, showing the changes in the stocks resulting from the transactions (the transaction flow and the stock revaluation matrix are often merged in the full integration matrix). The matrices are built respecting intuitive principles. Someone's asset is someone else's liability and someone's inflow is someone else's outflows. Furthermore, each sector and the economy as a whole must respect their budget constraint. No fund can come from (or end up) nowhere.

The second component of SFC models, the behavioural equations, include the main theoretical assumption of the model. Most of the papers in the existing literature are based on post-Keynesian theory. However, the behavioural equations are not restricted to a single school of thought.[nb 1]

Most SFC models are formulated in discrete time,[1] but can also be formulated in continuous time as differential equations or differential-algebraic equations.[20][39]

Simple models can be solved analytically and investigated by means of concepts of dynamical system theory such as bifurcation analysis.[1][31][18] More complex models must be numerically simulated.[1]

Advantages and disadvantages

The comprehensive accounting framework has several advantages. Tracking all the monetary flows taking place in an economy and the way they accumulate, allows for a consistent integration of the real and the financial side of the economy (for a detailed discussion see Godley and Lavoie, 2007). Furthermore, as balance sheets are updated in any period, SFC models can be used to identify unsustainable processes, for example a prolonged deficit of a sector will result in an unsustainable stock of debt. These models were used by Wynne Godley in forecasting, showing promising results.[40] Moreover, from a modelling perspective, the consistent accounting framework prevents the modellers from leaving "black holes" i.e., unexplained parts of the model.

Example of SFC model

Flow of funds between sectors in a closed economy

| Households | Firms | Government | Rest of the World | Σ | |

|---|---|---|---|---|---|

| Consumption | -C | +C | 0 | ||

| Govt. Expenditures | +G | -G | 0 | ||

| [OUTPUT] | [Y] | ||||

| Wages | +W | -W | 0 | ||

| Taxes | -T | +T | 0 | ||

| Changes in Money | -ΔHh | +ΔHs | 0 | ||

| Σ | 0 | 0 | 0 |

The above table shows the flow of funds between different sectors for a closed economy with no explicit financial sector from a model by Wynne Godley and Marc Lavoie.[41] The minus (-) sign in the table represents that the sector has paid out while the plus (+) sign indicates the receipts of that sector, e.g., -C for the household sector shows that the household has paid for their consumption whereas the counter party of this transaction is the firm which receives +C. This implies that the firms have received the payments from the households. Similarly, all the respective flows in the economy are reported in the flow of funds. More advanced SFC models consist of a financial sector including banks and is further extended to an open economy by introducing the Rest of World sector. Introducing the financial sector enables in tracing the flow of loans between the sectors, which in turn helps in determining the level of debt every sector holds. These models become more complicated as new sectors and assets are added to the system.

The model structure

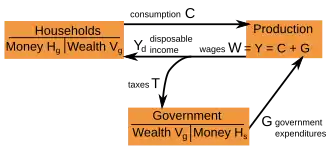

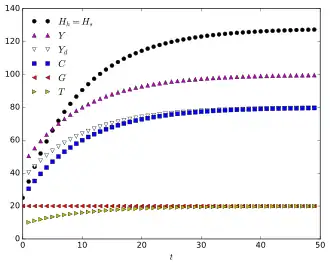

Once the accounting framework is fulfilled then the structure of the model, based on stylized facts, is defined. The set of equations in the model defines relationship between different variables, not determined by the accounting framework. The model structure basically helps in understanding how the flows are connected from a behavioral perspective or in simple words how the behavior of a sector affects the flow of funds in the system, e.g., the factors that affect the consumption (C) of the household is not clear from the flow of funds but can be explained by the model. The model structure with a set of equations for a simple closed economy is given by:

Y = C + G

T = θY

YD = Y – T

C = α1 Y + α2 Ht-1

ΔHs = G – T

ΔHh = YD – C

H = ΔH + Ht-1

Y (Income), C (Consumption), G (Government Expenditures), T (Taxes), YD (Disposable Income), ΔH (Changes in stock of money) and θ is the tax rate on the income of household sector. α1 is the household consumption out of disposable income. α2 is the household consumption out of previous wealth.

The SFC models are solved in different ways depending on the aspect of research but in general initial values are assigned to the stocks and then the model is calibrated or estimated.

Sources

- Wynne Godley, Marc Lavoie: Monetary Economics. An Integrated Approach to Credit, Money, Income, Production and Wealth. Palgrave Macmillan, New York 2012, ISBN 978-0-230-30184-9.

- Dimitri B. Papadimitriou, Gennaro Zezza: Contributions in Stock-flow Modeling: Essays in Honor of Wynne Godley. Palgrave Macmillan, London 2012, ISBN 978-1-349-33340-0, doi:10.1057/9780230367357.

- Eugenio Caverzasi, Antoine Godin: Post-Keynesian stock-flow-consistent modelling: a survey. In: Cambridge Journal of Economics 39(1), 2015, pp. 157–187, doi:10.1093/cje/beu021.

- Michalis Nikiforos, Gennaro Zezza: Stock-Flow Consistent Macroeconomics Models: A Survey. In: Journal of Economic Surveys 31(5), 2017, pp. 1204–1239, doi:10.1111/joes.12221.

- Emilio Carnevali, Matteo Deleidi, Riccardo Pariboni, Marco Veronese Passarella: Stock-Flow Consistent Dynamic Models: Features, Limitations and Developments. In: Philip Arestis, Malcolm Sawyer (eds.): Frontiers of Heterodox Macroeconomics, Palgrave Macmillan, Cham 2019, pp. 223–276. doi:10.1007/978-3-030-23929-9 6.

- Oliver Richters, Erhard Glötzl: Modeling economic forces, power relations, and stock-flow consistency: a general constrained dynamics approach. In: Journal of Post Keynesian Economics, 2020, doi:10.1080/01603477.2020.1713008

Notes

- " "According to Gennaro Zezza the accounting consistency should be a requirement for all macro model. Models with post-Keynesian behavioural assumption should therefore be a sub class of macro model labelled stock-flow-consistent post-Keynesian models"[38]

References

- Eugenio Caverzasi, Antoine Godin: Post-Keynesian stock-flow-consistent modelling: a survey In: Cambridge Journal of Economics 39(1), 2015, pp. 157–187, doi:10.1093/cje/beu021.

- Michalis Nikiforos, Gennaro Zezza: Stock-Flow Consistent Macroeconomics Models: A Survey. In: Journal of Economic Surveys 31(5), 2017, pp. 1204–1239, doi:10.1111/joes.12221.

- Knut Wicksell: Interest and Prices. Augustus M. Kelley Publishers, New York 1936/1898.

- John Maynard Keynes: The General Theory of Employment, Interest and Money. Palgrave Macmillan, London 1936.

- Emilio Carnevali, Matteo Deleidi, Riccardo Pariboni, Marco Veronese Passarella: Stock-Flow Consistent Dynamic Models: Features, Limitations and Developments. In: Philip Arestis, Malcolm Sawyer (eds.): Frontiers of Heterodox Macroeconomics, Palgrave Macmillan, Cham 2019, pp. 223–276. doi:10.1007/978-3-030-23929-9 6.

- Dirk Ehnts: The balance sheet approach to macroeconomics. In: Samuel Decker, Wolfram Elsner, Svenja Flechtner (eds.): Principles and Pluralist Approaches in Teaching Economics. Routledge, London / New York 2019, pp. 243–255, doi:10.4324/9781315177731-16.

- Morris A. Copeland: Social accounting for moneyflows. In: The Accounting Review 24(3), 1949, pp. 254–264, JSTOR 240684.

- Jacob Cohen: Copeland's money flows after twenty-five years: a survey. In: Journal of Economic Literature 10(1), 1972, pp. 1–25, JSTOR 2720888.

- James Tobin: Money and finance in the macro-economic process, Nobel Memorial Lecture, 1981.

- Robert W. Clower: Stock-flow analysis. In: David L. Sills, Robert K. Merton: International Encyclopedia of the Social Sciences 15, pp. 273–277, Macmillan and Free Press, New York 1968, OCLC 491474972.

- Robert W. Clower, D. W. Bushaw: Price Determination in a Stock-Flow Economy. In: Econometrica 22(3), pp. 328–343, JSTOR 1907357.

- Romain Plassard: The origins, development, and fate of Clower's "stock-flow" general-equilibrium programme. In: European Journal of the History of Economic Thought 25(1), Mai 2018, pp. 1–32, doi:10.1080/09672567.2018.1425468.

- Wolfgang Stützel: Volkswirtschaftliche Saldenmechanik. Mohr, Tübingen 1958, ISBN 978-3161509551.

- C.H. Dos Santos. "Notes on the Stock Flow Consistent Approach to Macroeconomic Modeling" (PDF). Retrieved 14 December 2014.

- Claudio H. Dos Santos, Gennaro Zezza: A simplified, 'benchmark', Stock-Flow Consistent Post-Keynesian growth model. In: Metroeconomica 59(3), 2008, pp. 441–478, doi:10.1111/j.1467-999X.2008.00316.x

- Wynne Godley, Francis Cripps: Macroeconomics. Oxford University Press 1983.

- Wynne Godley, Marc Lavoie: Monetary Economics. Palgrave Macmillan, New York 2012, ISBN 978-0-230-30184-9.

- Oliver Richters, Andreas Siemoneit: Consistency and Stability Analysis of Models of a Monetary Growth Imperative. In: Ecological Economics 136, 2017, pp. 114–125, doi:10.1016/j.ecolecon.2017.01.017.

- Gennaro Zezza: Godley and Graziani: Stock-flow Consistent Monetary Circuits. In: Dimitri B. Papadimitriou, Gennaro Zezza (eds.): Contributions in Stock-flow Modeling. Palgrave Macmillan, Basingstoke, pp. 154–172, doi:10.1057/9780230367357 8.

- Oliver Richters, Erhard Glötzl: Modeling economic forces, power relations, and stock-flow consistency: a general constrained dynamics approach. In: Journal of Post Keynesian Economics, 2020, doi:10.1080/01603477.2020.1713008.

- Wynne Godley: Money, finance and national income determination: an integrated approach, 1996, Working Paper 167, The Levy Economics Institute of Bard College.

- Dirk J. Bezemer: Understanding financial crisis through accounting models. In: Accounting, Organizations and Society 35(7), 2010, pp. 676–688, doi:10.1016/j.aos.2010.07.002.

- Michalis Nikiforos, Gennaro Zezza: Stock-flow Consistent Macroeconomic Models: A Survey. Levy Economics Institute of Bard College, Working Paper 891, 2017.

- Dimitri B. Papadimitriou, Gennaro Zezza: Contributions in Stock-flow Modeling: Essays in Honor of Wynne Godley. Palgrave Macmillan, London 2012, ISBN 978-1-349-33340-0, doi:10.1057/9780230367357.

- Wynne Godley, Randall Wray: Is goldilocks doomed? In: Journal of Economic Issues 34(1), 2000, pp. 201–206, doi:10.1080/00213624.2000.11506253.

- Wynne Godley, Gennaro Zezza: Debt and lending: A Cri de Coeur. Levy Institute at Bard College Policy Notes 4, 2006.

- David Colander, Peter Howitt, Alan Kirman, Axel Leijonhufvud, Perry Mehrling: Beyond DSGE Models: Toward an Empirically Based Macroeconomics. In: The American Economic Review 98(2), 2008, pp. 236–240, doi:10.2307/29730026.

- Edwin Le Heron: Confidence and financial crisis in a post-Keynesian stock flow consistent model. In: European Journal of Economics and Economic Policies: Intervention 8(2), 2011, pp. 361–387, doi:10.4337/ejeep.2011.02.09.

- Marco Passarella: A simplified stock-flow consistent dynamic model of the systemic financial fragility in the 'New Capitalism'. In: Journal of Economic Behavior & Organization 83(3), 2012, pp. 570–582, doi:10.1016/j.jebo.2012.05.011.

- Eugenio Caverzasi, Antoine Godin: Financialisation and the sub-prime crisis: a stock-flow consistent model. In: European Journal of Economics and Economic Policies: Intervention 12(1), 2015, pp. 73–92, doi:10.4337/ejeep.2015.01.07.

- Matthew Berg, Brian Hartley, Oliver Richters: A Stock-Flow Consistent Input-Output Model with Applications to Energy Price Shocks, Interest Rates, and Heat Emissions. In: New Journal of Physics 17(1), 2015, 015011, doi:10.1088/1367-2630/17/1/015011.

- Yannis Dafermos, Maria Nikolaidi, Giorgos Galanis: A stock-flow-fund ecological macroeconomic model. In: Ecological Economics 131, 2017, pp.191–207, doi:10.1016/j.ecolecon.2016.08.013.

- Yannis Dafermos, Maria Nikolaidi, Giorgos Galanis: Climate change, financial stability and monetary policy. In: Ecological Economics 152, 2018, pp. 219–234, doi:10.1016/j.ecolecon.2018.05.011.

- Jonathan Barth, Oliver Richters: Demand-driven ecological collapse: a stock-flow fund-service model of money, energy, and ecological scale. In: Samuel Decker, Wolfram Elsner, Svenja Flechtner (eds.): Principles and Pluralist Approaches in Teaching Economics. Routledge, London / New York 2019, pp. 169–190, doi:10.4324/9781315177731-12.

- Alessandro Caiani, Antoine Godin, Eugenio Caverzasi, Mauro Gallegati, Stephen Kinsella, Joseph E. Stiglitz: Agent Based-Stock Flow Consistent Macroeconomics: Towards a Benchmark Model. In: Journal of Economic Dynamics and Control 69, 2016, pp. 375–408, doi:10.1016/j.jedc.2016.06.001.

- Stephen Kinsella, Matthias Greiff, Edward J. Nell: Income distribution in a stock-flow consistent model with education and technological change. In: Eastern Economic Journal 37(1), 2011, pp. 134–149, doi:10.1057/eej.2010.31.

- Jung Hoon Kim, Marc Lavoie: A two-sector model with target-return pricing in a stock-flow consistent framework. In: Economic Systems Research 28(3), 2016, pp. 403–427, doi:10.1080/09535314.2016.1196166.

- Claudio H. Dos Santos: Cambridge and Yale on Stock-Flow Consistent Macroeconomic Modeling. Department of Economics, New School University, New York 2002.

- Soon Ryoo: Long waves and short cycles in a model of endogenous financial fragility. In: Journal of Economic Behavior & Organization 74(3), 2010, pp. 163–186, doi:10.1016/j.jebo.2010.03.015.

- Wynne Godley (1999). "Seven Unsustainable Processes" (PDF). Special Report.

- Wynne Godley, Marc Lavoie: Monetary Economics, Palgrave MacMillan 2007.

External links

- Lavoie, Marc "Stock Flow Consistent Modeling", video and slides