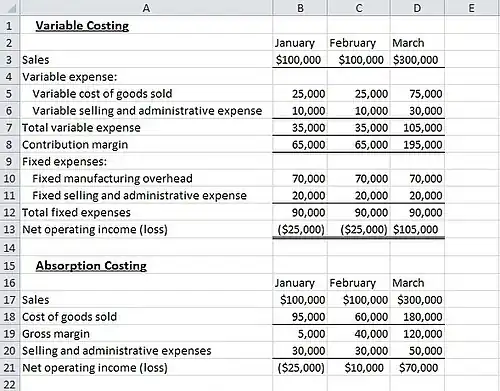

Variable costing

Variable costing is a managerial accounting cost concept. Under this method, manufacturing overhead is incurred in the period that a product is produced. This addresses the issue of absorption costing that allows income to rise as production rises. Under an absorption cost method, management can push forward costs to the next period when products are sold. This artificially inflates profits in the period of production by incurring less cost than would be incurred under a variable costing system.[1] Variable costing is generally not used for external reporting purposes. Under the Tax Reform Act of 1986, income statements must use absorption costing to comply with GAAP.

Variable costing is a costing method that includes only variable manufacturing costs—direct materials, direct labor, and variable manufacturing overhead—in unit product costs.[2]

References

- ABSORPTION VS VARIABLE COSTING LECTURE - BREAKEVEN ANALYSIS

- Managerial Accounting: Ray H. Garrison, Eric W. Noreen, Peter C. Brewer, 14th edition, 2012

- Managerial Accounting: Ray H. Garrison, Eric W. Noreen, Peter C. Brewer, 14th edition, 2012