Zero interest-rate policy

Zero interest-rate policy (ZIRP) is a macroeconomic concept describing conditions with a very low nominal interest rate, such as those in contemporary Japan and in the United States from December 2008 through December 2015 and again from March 2020 until March 2022 as a result of the COVID-19 pandemic. ZIRP is considered to be an unconventional monetary policy instrument and can be associated with slow economic growth, deflation and deleverage.[1]

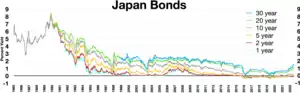

Inverted yield curve in 1990

Zero interest-rate policy starting in 1995

Negative interest rate policy started in 2014

Overview

Under ZIRP, the central bank maintains a 0% nominal interest rate. The ZIRP is an important milestone in monetary policy because the central bank is typically no longer able to reduce nominal interest rates. ZIRP is very closely related to the problem of a liquidity trap, where nominal interest rates cannot adjust downward at a time when savings exceed investment.

However, some economists—such as market monetarists—believe that unconventional monetary policy such as quantitative easing can be effective at the zero lower bound.

Others argue that when monetary policy is already used to the maximal extent, governments must be willing to use fiscal policy to create jobs. The fiscal multiplier of government spending is expected to be larger when nominal interest rates are zero than they would be when nominal interest rates are above zero. Keynesian economics holds that the multiplier is above one, meaning government spending effectively boosts output. In his paper on this topic, Michael Woodford finds that, in a ZIRP situation, the optimal policy for government is to spend enough in stimulus to cover the entire output gap.[2]

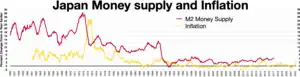

Chris Modica and Warren Sulmasy find that the ZIRP policy follows from the need to refinance a high level of US public debt and from the need to recapitalize the world's banking system in the wake of the Financial crisis of 2007–2008.[3]

Zero lower bound

The zero lower bound problem refers to a situation in which the short-term nominal interest rate is zero, or just above zero, causing a liquidity trap and limiting the capacity that the central bank has to stimulate economic growth. This problem returned to prominence with the Japan's experience during the 1990s and more recently with the subprime crisis. The belief that monetary policy under the ZLB was effective in promoting economy growth has been critiqued by economists Paul Krugman, Gauti Eggertsson and Michael Woodford among others. Milton Friedman, on the other hand, argued that a zero nominal interest rate presents no problem for monetary policy, as a central bank can increase the monetary base only if it continues buying bonds.[4]

See also

References

- Roubini, Nouriel (January 14, 2016). "Troubled Global Economy". Time Magazine. time.com. Retrieved February 5, 2016.

- Woodford, Michael (2011). "Simple Analytics of the Government Expenditure Multiplier". American Economic Journal. 3 (1): 1–35. CiteSeerX 10.1.1.183.9546. doi:10.1257/mac.3.1.1. S2CID 11575586.

- Modica, Chris; Sulmasy, Warren (March 27, 2013). "Why the Federal Reserve Bank Has a Near Zero Interest Rate Policy". Yahoo! Finance. Archived from the original on June 30, 2013.

- "Milton Friedman's Keynote address at the Bank of Canada" (PDF).

Further reading

- Eggertsson, Gauti B.; Woodford, Michael (2003). "The Zero Bound on Interest Rates and Optimal Monetary Policy". Brookings Papers on Economic Activity. 2003 (1): 139–211. CiteSeerX 10.1.1.603.7748. doi:10.1353/eca.2003.0010. JSTOR 1209148. S2CID 153895795.