In economics, the marginal product of labor (MPL) is the change in output that results from employing an added unit of labor. This is not always equivalent to the output directly produced by that added unit of labor; for example, employing an additional cook at a restaurant may make the other cooks more efficient by allowing more specialization of tasks, creating a marginal product that is greater than that produced directly by the new employee. Conversely, hiring an additional worker onto an already crowded factory floor may make the other employees less productive, leading to a marginal product that is lower than the work done by the additional employee.

When production is discrete, we can define the marginal product of labor as ΔY/ΔL where Y is output. If a factory that is initially producing 100 widgets hires another employee and is then able to produce 106 widgets, the MPL is simply six. When production is continuous, the MPL is the first derivative of the production function in terms of L. Graphically, the MPL is the slope of the production function.

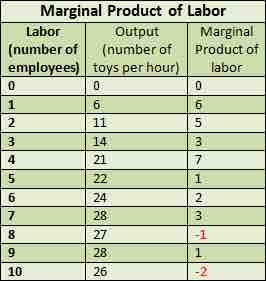

gives another example of marginal product of labor. The second column shows total production with different quantities of labor, while the third column shows the increase (or decrease) as labor is added to the production process.

Marginal Product of Labor

This table shows hypothetical returns and marginal product of labor. Note that in reality this firm would never hire more than seven employees, since a negative marginal product is bad for the firm regardless of the wage rate.

The law of diminishing marginal returns ensures that in most industries, the MPL will eventually be decreasing. The law states that "as units of one input are added (with all other inputs held constant) a point will be reached where the resulting additions to output will begin to decrease; that is marginal product will decline. " The law of diminishing marginal returns applies regardless of whether the production function exhibits increasing, decreasing or constant returns to scale. The key factor is that the variable input is being changed while all other factors of production are being held constant. Under such circumstances diminishing marginal returns are inevitable at some level of production.