The difficulty with accounting has less to do with the math as it does with its concepts. There is no more difficult yet vital concept to understand than that of debits and credits. Debits and credits are at the heart of the double-entry bookkeeping system that has been the foundation stone on which the financial world's accounting system has been built for well over 500 years. Given the length of time, is it any wonder that confusion has surrounded the concept of debits and credits? The English language and its laws have morphed to bring new definitions for two words that, in the accounting world, have their own significance and meaning.

For a better conceptual understanding of debits and credits, let us look at the meaning of the original Latin words. The English translators took theirs word credit and debit from the Latin words credre and debere, respectively. Credre means "to entrust," and debere means "to owe. " When we look closely into these two concepts we see that they are actually two sides of the same coin. In a closed financial system, money cannot just materialize. If money is received by someone it must have come from someone. That is, if someone entrusts an amount of money to someone else, then that person receiving the entrusted money would owe the same amount of money in return (i.e., the credre must equal the debere).

The Accounting Definition

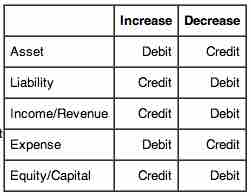

Debits and credits serve as the two balancing aspects of every financial transaction in double-entry bookkeeping. Debits are entered on the left side of a ledger, and credits are entered on the right side of a ledger. Whether a debit increases or decreases an account depends on what kind of account it is. In the accounting equation Assets = Liabilities + Equity, if an asset account increases (by a debit), then one must also either decrease (credit) another asset account or increase (credit) a liability or equity account.

Another way to help remember debit and credit rules, is to think of the accounting equation as a tee (T), the vertical line of the tee (T) goes between assets and liabilities. Everything on the left side (debit side) increases with a debit and has a normal debit balance; everything on the right side (credit side) increases with a credit and has a normal credit balance. (Note: a normal balance does not always mean the accounts balance will be on that side, it's simply a way of remembering which side increases it).

Accounting Equation

The extended accounting equation allows for revenue and expenses as well.

Assets = Liabilities + Owner's Equity + Revenue – Expenses

As you already know the first part of the equation, let's focus on the new classifications, revenue and expenses.

- Revenue is treated like capital, which is an owner's equity account, and owner's equity is increased with a credit, and has a normal credit balance.

- Expenses reduce revenue, therefore they are just the opposite, increased with a debit, and have a normal debit balance.

Each transaction (let's say $100) is recorded by a debit entry of $100 in one account, and a credit entry of $100 in another account. When people say that "debits must equal credits" they do not mean that the two columns of any ledger account must be equal. If that were the case, every account would have a zero balance (no difference between the columns), which is often not the case. The rule that total debits equal the total credits applies when all accounts are totaled.

Perspective

It is important for us to consider perspective when attempting to understand the concepts of debits and credits. For example, one credit that confuses most newcomers to accounting is the one that appears on their own bank statement. We know that cash in the bank is an asset, and when we increase an asset we debit its account. Then how come the credit balance in our bank accounts goes up when we deposit money? The answer is one that is fundamental to the accounting system. Each firm records financial transactions from their own perspective.

Think about the bank's perspective for a moment. How do they view the money we have just deposited? Whose money is it? It's ours; therefore, from the bank's perspective the deposit is viewed as a liability (money owed by the bank to others). When we deposit money into our accounts, the bank's liability increases, which is why the bank credits our account.

In summary: An increase (+) to an asset account is a debit and an increase (+) to a liability account is a credit; conversely, a decrease (-) to an asset account is a credit and a decrease (-) to a liability account is a debit.

What is debited and credited is also a matter of transaction type. In accounting, these are divided into three types of accounts. The rule of debit and credit depends on the type of account you are talking about:

- Personal account: Debit the receiver and credit the giver

- Real account: Debit what comes in and credit what goes out

- Nominal account: Debit all expenses & losses and credit all incomes & gains

Debit and credit rules

Debit and credit rules