Components of the Cash Flow Statement

In financial accounting, a cash flow statement, also known as statement of cash flows or funds flow statement, is a financial statement that shows how changes in balance sheet accounts and income affect cash and cash equivalents, and breaks the analysis down to operating, investing, and financing activities. Essentially, the cash flow statement is concerned with the flow of cash in and out of the business. The statement captures both the current operating results and the accompanying changes in the balance sheet and income statement. For businesses that use cash basis accounting, the cash flow statement and income statement provide the same information, since cash inflows are considered income and cash outflows consist of expense payments or other types of payments (i.e. asset purchases).

The cash flow statement is partitioned into three segments, namely:

- Cash flow resulting from operating activities

- Cash flow resulting from investing activities

- Cash flow resulting from financing activities.

- It also may include a disclosure of non-cash financing activities.

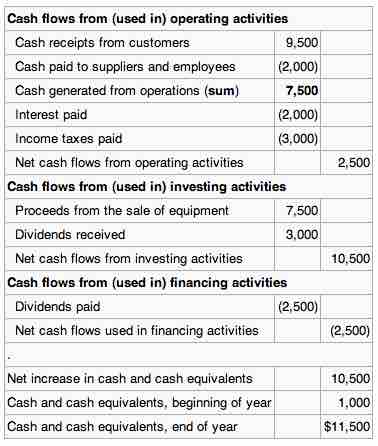

Statement of cash flows

Statement of cash flows includes cash flows from operating, financing and investing activities.

Operating activities include the production, sales, and delivery of the company's product as well as collecting payments from its customers. This could include purchasing raw materials, building inventory, advertising, and shipping the product.

Investing activities are purchases or sales of assets (land, building, equipment, marketable securities, etc.), loans made to suppliers or received from customers, and payments related to mergers and acquisitions.

Financing activities include the inflow of cash from investors, such as banks and shareholders and the outflow of cash to shareholders as dividends as the company generates income. Other activities that impact the long-term liabilities and equity of the company are also listed in the financing activities section of the cash flow statement.

Non-cash investing and financing activities are disclosed in footnotes to the financial statements. Under the U.S. General Accepted Accounting Principles (GAAP), non-cash activities may be disclosed in a footnote or within the cash flow statement itself. Non-cash financing activities may include leasing to purchase an asset, converting debt to equity, exchanging non-cash assets or liabilities for other non-cash assets or liabilities, and issuing shares in exchange for assets.