The law of supply is a fundamental principle of economic theory. It states that an increase in price will result in an increase in the quantity supplied, all else held constant.

An upward sloping supply curve, which is also the standard depiction of the supply curve, is the graphical representation of the law of supply. As the price of a good or service increases, the quantity that suppliers are willing to produce increases and this relationship is captured as a movement along the supply curve to a higher price and quantity combination.

The Law of Supply

Supply has a positive correlation with price. As the market price of a good increases, suppliers of the good will typically seek to increase the quantity supplied to the market.

The rationale for the positive correlation between price and quantity supplied is based on the potential increase in profitability that occurs with an increase in price.

All else held constant, including the costs of production inputs, the supplier will be able to increase his return per unit of a good or service as the price for the item increases. Therefore, the net return to the supplier increases as the spread or difference between the price and the cost of the good or service being sold increases.

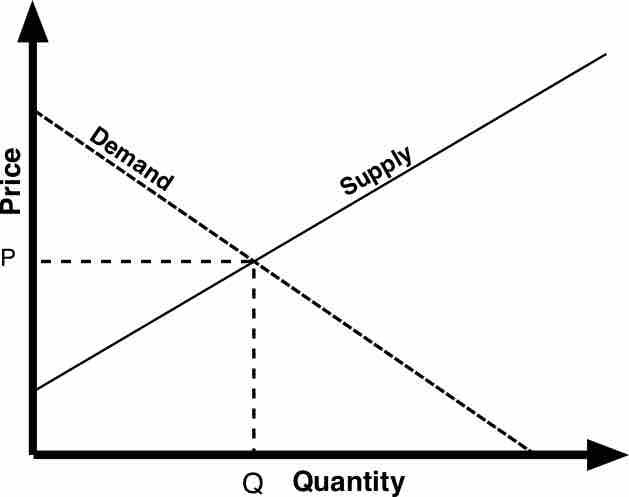

The law of supply in conjunction with the law of demand forms the basis for market conditions resulting in a price and quantity relationship at which both the price to quantity relationship of suppliers and demanders (consumers) are equal. This is also referred to as the equilibrium price and quantity and is depicted graphically at the point at which the demand and supply curve intersect or cross one another. It is the point where there is no surplus or shortage in the market .

Law of Supply and Law of Demand: Equilibrium

The law of supply and the law of demand form the foundation for the establishment of an equilibrium--where the price to quantity combination for both suppliers and demanders are the same.