The bond price can be calculated using the present value approach. Bond valuation is the determination of the fair price of a bond. As with any security or capital investment, the theoretical fair value of a bond is the present value of the stream of cash flows it is expected to generate. Therefore, the value of a bond is obtained by discounting the bond's expected cash flows to the present using an appropriate discount rate. In practice, this discount rate is often determined by reference to similar instruments, provided that such instruments exist. The formula for calculating a bond's price uses the basic present value (PV) formula for a given discount rate .

Bond Price

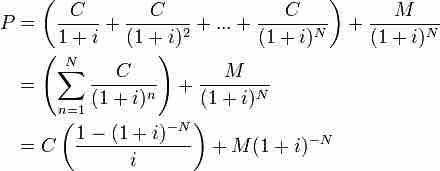

Bond price is the present value of coupon payments and face value paid at maturity.

F = face value, iF = contractual interest rate, C = F * iF = coupon payment (periodic interest payment), N = number of payments, i = market interest rate, or required yield, or observed / appropriate yield to maturity, M = value at maturity, usually equals face value, and P = market price of bond.

The bond price can be summarized as the sum of the present value of the par value repaid at maturity and the present value of coupon payments. The present value of coupon payments is the present value of an annuity of coupon payments.

An annuity is a series of payments made at fixed intervals of time. The present value of an annuity is the value of a stream of payments, discounted by the interest rate to account for the payments being made at various moments in the future. The present value is calculated by:

i is the number of periods and n is the per period interest rate.