Aggregate supply

In economics, aggregate supply (AS) or domestic final supply (DFS) is the total supply of goods and services that firms in a national economy plan on selling during a specific time period. It is the total amount of goods and services that firms are willing and able to sell at a given price level in an economy. It's natural counterpart is aggregate demand.

| Part of a series on |

| Macroeconomics |

|---|

.JPG.webp) |

Analysis

There are two main reasons why the amount of aggregate output supplied might rise as price level P rises, i.e., why the AS curve is upward sloping:

- The short-run AS curve is drawn given some nominal variables such as the nominal wage rate, which is assumed fixed in the short run. Thus, a higher price level P implies a lower real wage rate and thus an incentive to produce more output. In the neoclassical long run, on the other hand, the nominal wage rate varies with economic conditions. (High unemployment leads to falling nominal wages which restore full employment.) Hence, in the long run, the aggregate supply curve is vertical.

- An alternative model starts with the notion that any economy involves a large number of heterogeneous types of inputs, including both fixed capital equipment and labour. Both main types of inputs can be unemployed. The upward-sloping AS curve arises because (1) some nominal input prices are fixed in the short run and (2) as output rises, more and more production processes encounter bottlenecks. At low levels of demand, there are large numbers of production processes that do not use their fixed capital equipment fully. Thus, production can be increased without much in the way of diminishing returns and the average price level need not rise much (if at all) to justify increased production. The AS curve is flat. On the other hand, when demand is high, few production processes have unemployed fixed inputs. Thus, bottlenecks are general. Any increase in demand and production induces increases in prices. Thus, the AS curve is steep or vertical.

Different scopes

There are generally three alternative degrees of price-level responsiveness of aggregate supply. They are:

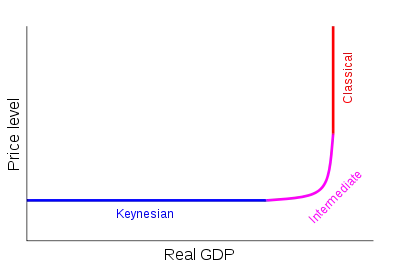

- Short-run aggregate supply (SRAS) — During the short-run, firms possess one fixed factor of production (usually capital), and some factor input prices are sticky. The quantity of aggregate output supplied is highly sensitive to the price level, as seen in the flat region of the curve in the above diagram.

- Long-run aggregate supply (LRAS) — Over the long run, only capital, labour, and technology affect the LRAS in the macroeconomic model because at this point everything in the economy is assumed to be used optimally. In most situations, the LRAS is viewed as static because it shifts the slowest of the three. The LRAS is shown as perfectly vertical, reflecting economists' belief that changes in aggregate demand (AD) have an only temporary change on the economy's total output.

- Medium run aggregate supply (MRAS) — As an interim between SRAS and LRAS, the MRAS form slopes upward and reflects when capital, as well as labor usage, can change. More specifically, medium run aggregate supply is like this for three theoretical reasons, namely the Sticky-Wage Theory, the Sticky-Price Theory and the Misperception Theory. The position of the MRAS curve is affected by capital, labour, technology, and wage rate.

In the standard aggregate supply-aggregate demand model, real output (Y) is plotted on the horizontal axis and the price level (P) on the vertical axis. The levels of output and the price level are determined by the intersection of the aggregate supply curve with the downward-sloping aggregate demand curve.

Data

In the United Kingdom, aggregate supply data is published in the Office for National Statistics' Input–output supply and use tables.[1]

Policy interventions

Aggregate supply is targeted by government "supply-side policies", which are intended to increase productive efficiency and hence national output. Some examples of supply-side policies include education and training, research and development, supporting small/medium entreprise, reducing business taxes, undertaking labour market reforms to diminish frictions that may hold down output, and investment in infrastructure. For example, the United Kingdom's 2011 Autumn Statement incorporated a series of supply-side measures which the government was undertaking "to rebalance and strengthen the economy in the medium term", which included extensive infrastructure investment and development of a more educated workforce.[2] Supply-side reforms in the 2015 Budget addressed the nation's digital communications infrastructure, transport, energy and the environment.[3] In a speech to the G20 in February 2016, Mark Carney, Governor of the Bank of England, urged G20 members "to develop a coherent and urgent approach to supply-side policies".[4]

Continuing "supply-side reforms" were proposed by Liz Truss and Chancellor Kwasi Kwarteng as part of their 2022 economic programme,[5][6] with reference to "a comprehensive package of supply-side reform and tax cuts" being made in the Growth Plan announced on 23 September 2022,[7] and further supply side growth measures promised for October and early November, including measures affecting the planning system, business regulation, childcare, immigration, agricultural productivity and digital infrastructure.[8] However, Larry Elliott in The Guardian has described this combination of reforms, reduced regulation and tax cuts as "one huge gamble".[9] The September Growth Plan commitments were mostly reversed by the Autumn Statement of 17 November 2022, although a limited number of initiatives relating to "supply side growth" were included in the latter statement.[10]

Within the UK government, HM Treasury's work on "the supply side" is led by the Enterprise and Growth Unit,[11] working in conjunction with other government departments and public bodies.[12] Sir John Kingman, a former civil servant who has been described as the "champion of HM Treasury's supply-side activism",[13] has referred to concern with "the supply side" as the "third mission" of the Treasury,[14] presenting former Chancellor of the Exchequer Nigel Lawson as a notable example of "those who believe in the importance of supply-side reform".[13]

"Supply-side pessimism" reflects a concern that productive capacity is lost when unused (e.g. during a recession), so that the economy loses the ability to recover aggregate supply when demand recovers. For example, unused factories are not kept in a state of readiness to be used when an economic upturn begins, or workers miss out on the skills and training which they would normally acquire whilst in work.[15] Spencer Dale, a British economist who sat on the Bank of England's Monetary Policy Committee between 2008 and 2014, took a pessimistic view of supply-side capabilities during the recession of 2012.[15] Cambridge economist Bill Martin reported on productivity pessimism in 2012, noting that there was an established debate about whether there had been a permanent loss of productive capacity,[16] which was reflected as a continuing level of "uncertainty ... related to the prospects for labour productivity and effective supply" as the economy recovered in 2013.[17]

See also

References

- Office for National Statistics, Input–output supply and use tables, last published 29 October 2021, accessed 4 October 2022

- H M Treasury, Autumn Statement 2011, November 2011, Annex A, pp. 53, 59

- H M Treasury, Budget 2015, published 18 March 2015, accessed 21 August 2022, pp. 94-100

- Mark Carney, Governor of the Bank of England, 'Redeeming an unforgiving world', G20 conference speech, February 2016, quoted in H M Treasury, Budget 2016, published 16 March 2016, accessed 21 August 2022, page 15

- Elliott, L., How is Liz Truss's government challenging 'Treasury orthodoxy'?, The Guardian, published 13 September 2022, accessed 14 September 2022

- HM Treasury, Chancellor Kwasi Kwarteng sets out economic priorities in first meeting with market leaders, updated 7 September 2022, accessed 14 September 2022

-

This article incorporates text published under the British Open Government Licence: HM Treasury, The Growth Plan 2022, published 23 September, p. 9

This article incorporates text published under the British Open Government Licence: HM Treasury, The Growth Plan 2022, published 23 September, p. 9 - This article incorporates text published under the British Open Government Licence: HM Treasury, Update on Growth Plan implementation, published 26 September 2022, accessed 8 October 2022

- Elliott, L., History suggests Kwarteng's gargantuan economic gamble won't end well, The Guardian, published 23 September 2022, accessed 26 September 2022

- HM Treasury, Autumn Statement 2022, sections 2.4, 5.70-5.75, published 17 November 2022, accessed 18 November 2022

- House of Commons Treasury Committee, Oral evidence: the work of the Treasury, HC 912, statement by Sir Tom Scholar, published 1 December 2021, accessed 21 September 2022

- HM Treasury Careers, Role of HM Treasury, accessed 23 September 2022

- Ross, M., John Kingman, champion of HM Treasury's supply-side activism, warns of Brexit threat, Global Government Forum, published 24 October 2016, accessed 21 September 2022

- Kingman, J., The Treasury and the Supply Side, a lecture given for the Strand Group, an arm of the Policy Institute at Kings College London, October 2016, accessed 21 September 2022

- Jones, C., Cohen, N., Battle rages over supply shock risks to economy, Financial Times, 5 June 2012, accessed 26 August 2022

- Martin, B., Is the British economy supply constrained? A critique of productivity pessimism, published July 2011, accessed 26 August 2022

- Monetary Policy Committee of the Bank of England, Minutes of the meeting held on 31 July and 1 August 2013, published 14 August 2013, accessed 26 August 2022

- Krugman, Paul; Wells, Robin; Olney, Martha (2007). Essentials of Economics. New York: Worth. ISBN 0716758792.

External links

- Elmer G. Wiens: Classical & Keynesian AD-AS Model - An on-line, interactive model of the Canadian Economy