Special-purpose acquisition company

A special purpose acquisition company (SPAC; /spæk/), also known as a "blank check company", is a shell corporation listed on a stock exchange with the purpose of acquiring (or merging with) a private company, thus making the private company public without going through the initial public offering process, which often carries significant procedural and regulatory burdens.[1][2] According to the U.S. Securities and Exchange Commission (SEC), SPACs are created specifically to pool funds to finance a future merger or acquisition opportunity within a set timeframe; these opportunities usually have yet to be identified while raising funds.[3]

In the US, SPACs are registered with the SEC and considered publicly-traded companies. The general public may buy their shares on stock exchanges before any merger or acquisition takes place. For this reason they have at times been referred to as the "poor man's private equity funds".[4] The majority of companies pursuing SPACs do so on the Nasdaq or New York Stock Exchange in the US, although other exchanges, such as the Euronext Amsterdam, Singapore Exchange, and Hong Kong Stock Exchange, have also overseen a small volume of SPAC deals.[5]

Despite the popularity and growth in the number of SPACs, academic analysis shows investor returns on SPAC companies post-merger are almost uniformly negative, although investors in SPACs and merged companies with may earn excess returns immediately after the merger.[6] Proliferation of SPACs usually accelerates around periods of economic bubbles, such as the "everything bubble" between 2020 and 2021.[7]

Characteristics

Mechanics

SPACs generally trade as units or as separate common shares and warrants on the Nasdaq and New York Stock Exchange (as of 2008) once the public offering has been declared effective by the SEC, distinguishing the SPAC from a blank check company formed under SEC Rule 419.[8] Commonly, units are denoted with the letter "u" (for unit) appended to the ticker symbol of SPAC shares.[9]

Trading liquidity of the SPAC's securities provide investors with a flexible exit strategy. In addition, the public currency enhances the position of the SPAC when negotiating a business combination with a potential merger or acquisition target. The common share price must be added to the trading price of the warrants to get an accurate picture of the SPAC's performance.

By market convention, 85% to 100% of the proceeds raised in the IPO for the SPAC are held in trust to be used at a later date for the merger or acquisition.[10] A SPAC's trust account can only be used to fund a shareholder-approved business combination or to return capital to public shareholders at a charter extension or business combination approval meeting.

Each SPAC has its own liquidation window within which it must complete a merger or an acquisition; past this deadline the SPAC will dissolve and return assets to its stockholders. In practice, SPAC sponsors often extend the life of a SPAC by making a contribution to the trust account to entice shareholders to vote in favor of a charter amendment that delays the liquidation date.

In addition, the target of the acquisition must have a fair market value that is equal to at least 80% of the SPAC's net assets at the time of acquisition. Previous SPAC structures required a positive shareholder vote by 80% of the SPAC's public shareholders for the transaction to be consummated.[11] However, current SPAC provisions do not require a shareholder vote for the transaction to be consummated unless as follows:

| Purchase of assets | No |

| Purchase of stock of target not involving a merger with the company | No |

| Merger of target with a subsidiary of the company | No |

| Merger of the company with a target | Yes |

Governance

To allow for stockholders of the SPAC to make an informed decision on whether they wish to approve the business combination, the company must make full disclosure to stockholders of the target business, including complete audited financials, and terms of the proposed business combination via an SEC merger proxy statement. All common share stockholders of the SPAC are granted voting rights at a shareholder meeting to approve or reject the proposed business combination. A number of SPACs have also been placed on the London Stock Exchange AIM exchange. These SPACs do not have the aforementioned voting thresholds.

Since the financial crisis, protections for common shareholders have been implemented, allowing stockholders to vote in favor of a deal and still redeem their shares for a pro-rata share of the trust account. (This is significantly different from the blind pool – blank check companies of the 1980s, which were a form of limited partnership that did not specify what investment opportunities the company plans to pursue.) The assets of the trust are only released if a business combination is approved by the voting shareholders, or a business combination is not consummated within the amount of time allowed by a company's articles of incorporation.

Management

The SPAC is usually led by a management team composed of three or more members with prior private equity, mergers and acquisitions, and/or operating experience. The management team of a SPAC typically receives 20% of the equity in the vehicle at the time of offering, exclusive of the value of the warrants. The equity is usually held in escrow for two to three years, and management normally agrees to purchase warrants or units from the company in a private placement immediately prior to the offering. The proceeds from this sponsor investment (usually equal to between 2% and 8% of the amount being raised in the public offering) are placed in the trust and distributed to public stockholders in the event of liquidation.

No salaries, finder's fees, or other cash compensation are paid to the management team prior to the business combination, and the management team does not participate in a liquidating distribution if it fails to consummate a successful business combination. In many cases, management teams agree to pay for the expenses in excess of the trusts if there is a liquidation of the SPAC because no target has been found. Conflicts of interest are minimized within the SPAC structure because all management teams agree to offer suitable prospective target businesses to the SPAC before any other acquisition fund, subject to pre-existing fiduciary duties. The SPAC is further prohibited from consummating a business combination with any entity affiliated with an insider, unless a fairness opinion from an independent investment banking firm states that the combination is fair to the shareholders.

Banking

SPAC Research, an entity running a SPAC database, maintains an underwriter league table which can be sorted by bookrunner volume or other criteria for any year or selection of years.[12] As of January 2021 I-Bankers Securities Inc. stated that it had participated in 132 SPAC IPOs as lead or co-manager since 2004.[13] In the years leading up to 2021, bulge bracket banks started participating in more SPAC IPOs, with Cantor Fitzgerald & Co. and Deutsche Bank Securities Inc. on the cover of 30 SPAC IPOs from 2015 to August 2019.[14] Citigroup, Credit Suisse, Goldman Sachs, and BofA have all built a significant SPAC practice, while Cantor Fitzgerald led all SPAC underwriters in 2019 by book-running 14 SPACs that raised over US$3.08 billion in IPO proceeds.[12]

SPACs in Europe

In July 2007, Pan-European Hotel Acquisition Company N.V. was the first SPAC offering listed on the Euronext Amsterdam, raising approximately €115 million. I-Bankers Securities has been the underwriter with CRT Capital Group as lead-underwriter.[15][16] That listing on NYSE Euronext (Amsterdam) was followed by Liberty International Acquisition Company, raising €600 million in January 2008. Liberty is the third largest SPAC in the world and the largest outside the U.S.A. The first German SPAC was Germany1 Acquisition Ltd., which raised $437.2 million at Euronext Amsterdam with Deutsche Bank and I-Bankers Securities as underwriters.[17][13] Loyens & Loeff served as legal counsels in The Netherlands.[15]

In March 2021, a report prepared by Lord Hill for the Chancellor of Exchequer recommended a series of changes to London company listing rules to make them more favorable to SPAC listings.[18] Among the report's proposals is to reduce the percentage of shares that must be offered to the public from 25% to 15%.[19]

SPACs in Asia

On March 18, 2022, Aquila Acquisition Corp debuted on the Hong Kong Exchanges and Clearing Limited (HKEX). The IPO received lukewarm reception by investors, with shares down 3% in the two-week period post-IPO. Despite this decrease, there is a high demand for SPAC public offerings in Hong Kong, with HKEX reporting that they have received applications for 11 additional SPAC IPOs.[20]

SPACs in emerging markets

Emerging market focused SPACs, particularly those seeking to consummate a business combination in China, have been incorporating a 30/36 month timeline to account for the additional time that it has taken previous similar entities to successfully open their business combinations.

History

| History of private equity and venture capital |

|---|

.jpg.webp) |

| Early history |

| (origins of modern private equity) |

| The 1980s |

| (leveraged buyout boom) |

| The 1990s |

| (leveraged buyout and the venture capital bubble) |

| The 2000s |

| (dot-com bubble to the credit crunch) |

| The 2010s |

| (expansion) |

| The 2020s |

| (COVID-19 recession) |

Since the 1990s, SPACs have existed in the technology, healthcare, logistics, media, retail and telecommunications industries. Their history began with investment bank GKN Securities, specifically, founders David Nussbaum,[21] Roger Gladstone, and Robert Gladstone, who later founded EarlyBirdCapital with Steve Levine and David Miller (currently managing partner of Graubard Miller law firm) and who developed the template.

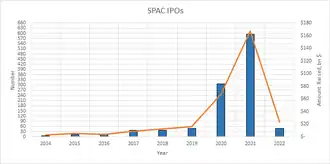

SPAC IPOs have seen resurgent interest since 2014, with increasing amounts of capital flowing to them:[14]

| Year | Proceeds (in billions) | Number of Deals |

|---|---|---|

| 2014 | 1.8 | 12 |

| 2015 | 3.9 | 20 |

| 2016 | 3.5 | 13 |

| 2017 | 10.1 | 34 |

| 2018 | 10.7 | 46 |

| 2019 | 13.6 | 59 |

| 2020 | 83.4 | 248 |

| 2021 | 162.5 | 613 |

| 2022 | 13.4 | 86 |

The success of SPACs in building equity value for their shareholders has drawn interest from investors such as Bill Ackman who had backed three SPACs as of 2015, including the SPAC that took Burger King public.[22][23][24][25]

Regulation

In the US the SPAC public offering structure is governed by the Securities and Exchange Commission (SEC). A public offering for a SPAC is typically filed with the SEC under an S-1 registration statement (or an F-1 for a foreign private issuer) and is classified by the SEC under SIC code 6770 - Blank Checks. Full disclosure of the SPAC structure, target industries or geographic regions, management team biographies, share ownership, potential conflicts of interest and risk factors are standard material covered in the S-1 registration statement. It is believed that the SEC has studied SPACs to determine whether they require special regulations to ensure that these vehicles are not abused as blind pool trusts and blank-check corporations have been over the years. Many believe that SPACs do have corporate governance mechanisms in place to protect shareholders. SPACs listed on the American Stock Exchange are required to be Sarbanes-Oxley compliant at the time of the offering, including such mandatory requirements as a majority of the board of directors being independent, and having audit and compensation committees.

Statistics

According to an industry study published in January 2019, from 2004 through 2018, approximately $49.14 billion was raised across 332 SPAC IPOs in the US. In that period, 2018 was the largest year for SPAC issuance since 2007, with 46 SPAC IPOs raising approximately $10.74 billion. SPACs seeking an acquisition in the energy sector raised $1.4bn in 2018, after raising a record $3.9bn in 2017. NASDAQ was the most common listing exchange for SPACs in 2018, with 34 SPACs raising $6.4bn. GS Acquisition Holdings Corp. and Churchill Capital Corp. raised the largest SPACs of 2018, with $690mm each in IPO proceeds.[26] In 2019, 59 SPAC IPO's raised $13.6 billion.[27] Nearly 250 SPACs raised more than $83 billion in 2020. In the first month of 2021 there were 75 SPACs.[28]

In a March 2020 event, Allison Lee, acting chair of the SEC, said that the "investment returns don't match the hype surrounding the SPAC bubble".[29]

Past Performance

A study found that as of the 1st of December 2022, American-listed SPACs that completed their mergers between July 2020 and December 2021 had a mean share price of $3.85. This constitutes a fall of over 60% from the standard $10 per share that SPAC shareholders could have received if they redeemed their shares. It was also found that “The average post-merger SPAC during this period underperformed the average traditional IPO by 26% ”.[30] Another study, focusing on a longer timeframe of U.S. SPACs from December 2012 until June 2021 found average stock price decreases of 14.1% after 1 year of the merger announcement and 18% after 2 years.[31]

See also

References

- Domonoske, Camila (2020-12-29). "The Spectacular Rise Of SPACs: The Backwards IPO That's Taking Over Wall Street". NPR. Archived from the original on 2021-02-22.

So what is a SPAC? A "special purpose acquisition company" is a way for a company to go public without all the paperwork of a traditional IPO, or initial public offering. In an IPO, a company announces it wants to go public, then discloses a lot of details about its business operations. After that, investors put money into the company in exchange for shares. A SPAC flips that process around. Investors pool their money together first, with no idea what company they're investing in. The SPAC goes public as a shell company. The required disclosures are easier than those for a regular IPO, because a pile of money doesn't have any business operations to describe. Then, generally, the SPAC goes out and looks for a real company that wants to go public, and they merge together. The company gets the stock ticker and the pile of money much more quickly than through a normal IPO.

- Broughton, Kristin; Maurer, Mark (September 22, 2020). "Why Finance Executives Choose SPACs: A Guide to the IPO Rival". The Wall Street Journal. Retrieved 22 February 2021.

- "Blank Check Company". SEC.gov. U.S. Securities and Exchange Commission. Retrieved 26 August 2020.

- Ren, Shuli (March 8, 2021). "SPACs Are 'the Poor Man's Private Equity Funds'". Bloomberg Businessweek (4691): 72. ISSN 0007-7135. Retrieved 9 March 2021.

- "Are SPAC mergers still a healthy option for tech companies aiming to go public?". KrASIA. 2022-03-23. Retrieved 2022-03-27.

- Li, Yun (10 February 2021). "Unusual first-day rallies in SPACs raise bubble concern: 'Every single one of them has gone up'". CNBC. Retrieved 18 February 2021.

- Naumovska, Ivana (February 18, 2021). "The SPAC Bubble Is About to Burst". Harvard Business Review. Retrieved 22 February 2021.

- "17 CFR § 230.419 - Offerings by blank check companies". LII / Legal Information Institute. Retrieved 2021-02-23.

- Langager, Chad. "What are the fifth-letter identifiers on the Nasdaq?". Investopedia. Retrieved 2021-02-13.

- "SPACs explained | Fidelity". www.fidelity.com. Retrieved 2021-02-26.

- "Special Purpose Acquisition Company (SPAC) – Definition". WGP Global.

- "Underwriter League". SPAC Research. Retrieved 18 January 2021.

- "Completed Transactions". I-Bankers Securities. Retrieved 18 January 2021.

- "Special Purpose Acquisition Company Database | SPAC Research". SPAC Research. Retrieved 27 March 2022.

- "Data". www.afm.nl. Retrieved 2021-03-07.

- "Mondo Visione - Worldwide Exchange Intelligence". mondovisione.com.

- Cowie, Dawn (July 23, 2008). "Germany1 Acquisition raises $437.2 million". Wall Street Journal – via www.wsj.com.

- Thomas, Daniel; Stafford, Philip (March 3, 2021). "UK listing rules set for overhaul in dash to catch Spacs wave". THE FINANCIAL TIMES LTD. Archived from the original on 2022-12-11. Retrieved 3 March 2021.

- BBC News (March 3, 2021). "Hill review: London takes aim at Amsterdam with new listing rules". BBC.co.uk. BBC. Retrieved 3 March 2021.

- "Hong Kong Tests the Waters with SPAC IPOs". thediplomat.com. Retrieved 2022-04-27.

- "Trust Me". Forbes. Retrieved 2021-11-28.

- Gara, Antoine (2014-08-27). "Ackman's Pershing Square a Quiet Winner in Burger King's Tim Hortons Deal". TheStreet.com. New York. Retrieved 2020-07-02.

- Bill, Ackman (25 August 2014). "Ackman and Burger King". Bloomberg.com.

- Bill, Ackman. "Bill Ackman invests $350 million in SPAC". Forbes.

- Bill, Ackman. "Ackman in Platform Specialty SPAC".

- SPAC Research, SPAC Market Trends, January 2019

- "US SPAC IPO Issuance". SPACResearch.com. SPAC WIRE LLC. Retrieved 27 June 2020.

- Saldanha, Ruth (January 28, 2021). "SPACs Party Like It's 2020". Morningstar.com. Retrieved 2021-02-12.

- Bain, Benjamin (11 March 2021). "SPAC Investment Returns Don't Match 'Hype,' SEC Chief Says". Bloomberg News. Retrieved 13 March 2021.

- "Was the SPAC Crash Predictable?". Yale Journal on Regulation. Retrieved 2023-09-08.

- Kiesel, Florian; Klingelhöfer, Nico; Schiereck, Dirk; Vismara, Silvio (March 2023). "SPAC merger announcement returns and subsequent performance". European Financial Management. 29 (2): 399–420. doi:10.1111/eufm.12366. ISSN 1354-7798.

Bibliography

- Feldman, David N. (2018). Regulation A+ and Other Alternatives to a Traditional IPO. Hoboken, New Jersey: Wiley. ISBN 9781119416166.

- Klausner, Michael; Ohlrogge, Michael; Ruan, Emily (2021). "A Sober Look at SPACs". Stanford Law and Economics Olin Working Paper. 559.

- Pollard, Troy (2016). "Sneaking in the back door? An evaluation of reverse mergers and IPOs". Review of Quantitative Finance and Accounting. 47 (2): 305–341. doi:10.1007/s11156-015-0502-8. S2CID 54029302.

- Sjostrom, W. K. Jr. (2007–2008). "The Truth About Reverse Mergers". Entrepreneurial Business Law Journal. 2: 743–751.

External links

| Investment types |  | ||||||

|---|---|---|---|---|---|---|---|

| History | |||||||

| Terms and concepts |

| ||||||

| Investors | |||||||

| Related financial terms | |||||||

| |||||||