Price/Earnings Ratio

In stock trading, the price-to-earnings ratio of a share (also called its P/E, or simply "multiple") is the market price of that share divided by the annual earnings per share (EPS).

The P/E ratio is a widely used valuation multiple used as a guide to the relative values of companies; a higher P/E ratio means that investors are paying more for each unit of current net income, so the stock is more "expensive" than one with a lower P/E ratio. The P/E ratio can be regarded as being expressed in years. The price is in currency per share, while earnings are in currency per share per year, so the P/E ratio shows the number of years of earnings that would be required to pay back the purchase price, ignoring inflation, earnings growth, and the time value of money.

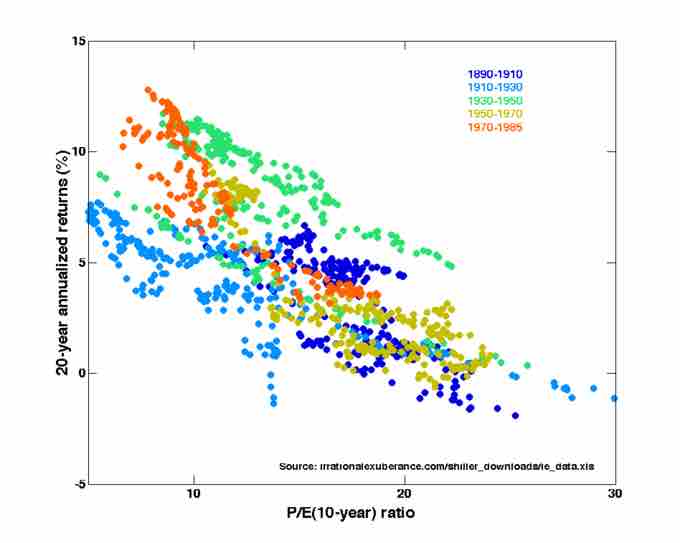

Price-Earning Ratios as a Predictor of Twenty-Year Returns

The horizontal axis shows the real price-earnings ratio of the S&P Composite Stock Price Index as computed in Irrational Exuberance (inflation adjusted price divided by the prior ten-year mean of inflation-adjusted earnings). The vertical axis shows the geometric average real annual return on investing in the S&P Composite Stock Price Index, reinvesting dividends, and selling twenty years later. Note that over the last century, as the P/E ratio has decreased, annualized returns have increased.

P/E ratio = Market price per share / Annual earnings per share

The price per share in the numerator is the market price of a single share of the stock. The earnings per share in the denominator may vary depending on the type of P/E. The types of P/E include the following:

- Trailing P/E or P/E ttm: Here, earning per share is the net income of the company for the most recent 12 month period, divided by the weighted average number of common shares in issue during the period. This is the most common meaning of P/E if no other qualifier is specified. Monthly earnings data for individual companies are not available, and usually fluctuate seasonally, so the previous four quarterly earnings reports are used, and earnings per share are updated quarterly. Note, each company chooses its own financial year so the timing of updates will vary from one to another.

- Trailing P/E from continued operations: Instead of net income, this uses operating earnings, which exclude earnings from discontinued operations, extraordinary items (e.g. one-off windfalls and write-downs), and accounting changes. Longer-term P/E data, such as Shiller's, use net earnings.

- Forward P/E, P/Ef, or estimated P/E: Instead of net income, this uses estimated net earnings over the next 12 months. Estimates are typically derived as the mean of those published by a select group of analysts (selection criteria are rarely cited). In times of rapid economic dislocation, such estimates become less relevant as the situation changes (e.g. new economic data is published, and/or the basis of forecasts becomes obsolete) more quickly than analysts adjust their forecasts.

By comparing price and earnings per share for a company, one can analyze the market's stock valuation of a company and its shares relative to the income the company is actually generating. Stocks with higher (or more certain) forecast earnings growth will usually have a higher P/E, and those expected to have lower (or riskier) earnings growth will usually have a lower P/E. Investors can use the P/E ratio to compare the value of stocks; for example, if one stock has a P/E twice that of another stock, all things being equal (especially the earnings growth rate), it is a less attractive investment. Companies are rarely equal, however, and comparisons between industries, companies, and time periods may be misleading. P/E ratio in general is useful for comparing valuation of peer companies in a similar sector or group.

The P/E ratio of a company is a significant focus for management in many companies and industries. Managers have strong incentives to increase stock prices, firstly as part of their fiduciary responsibilities to their companies and shareholders, but also because their performance based remuneration is usually paid in the form of company stock or options on their company's stock (a form of payment that is supposed to align the interests of management with the interests of other stock holders). The stock price can increase in one of two ways: either through improved earnings, or through an improved multiple that the market assigns to those earnings. In turn, the primary driver for multiples such as the P/E ratio is through higher and more sustained earnings growth rates.

Companies with high P/E ratios but volatile earnings may be tempted to find ways to smooth earnings and diversify risk; this is the theory behind building conglomerates. Conversely, companies with low P/E ratios may be tempted to acquire small high growth businesses in an effort to "rebrand" their portfolio of activities and burnish their image as growth stocks and thus obtain a higher P/E rating.