Corporate Taxes

Income taxes in the United States are an enormous and complex issue. Corporate taxes are especially complicated because of the inherent complexities of corporations themselves. Corporations may be taxed on their incomes, property, or their very existence. The types and rates of taxes vary depending on the jurisdiction in which the corporation is organized or acts. Maryland, for example, imposes a tax on corporations organized within its borders based on the number of shares of capital stock they issue.

Legal Forms of Corporations

Corporate taxation differs depending upon the legal form of the corporation. Which legal form to take is driven by the objectives of the company, but taxation also plays a vital role. Tax law contains built-in trade-offs for each corporate form, and companies often must give up some liability protection or flexibility.

Sole Proprietorship

A sole proprietorship is a business entity that is owned and run by a single individual. There is no legal distinction between the owner and the business. They are one in the same for tax purposes. The individual reports all income and expenses for the business on his or her personal income tax statement. In other words, the business is not taxed as a separate entity.

There is no method for sheltering tax in a sole proprietorship. Earnings are taxed regardless if they are actually distributed. In addition, the individual is held liable for the actions of the business, meaning claimants can pursue the personal property of the individual should solvency issues arise.

Partnership

A partnership is a business entity with two or more owners. For tax purposes, partnerships are treated similarly to a sole proprietorship - the owners pay tax on their "distributive share" of the business's taxable income. The partners must agree on how the income of the business will be allocated. Partners are jointly liable for the operations of the business. Thus, one partner may pursue one or any number of other partners in the case of personal damages or losses.

C Corporation

A C corporation refers to any corporation that is taxed separately from its owners. Although vastly outnumbered by sole proprietorships and partnerships, most of the largest companies in the U.S. are C corporations. Owners of C corporations are personally protected from any liability of the company - an idea known as the corporate veil. In return, the earnings of a C corporation are taxed both on the entity level and the individual level.

S Corporation

The S corporation is a hybrid entity wherein the income, deductions and tax credits of the business are taxed at the shareholder level as opposed to the entity level. However, owners enjoy the same limited liability awarded to C corporations. In exchange for this luxury, rules are placed on the types of corporations that can elect S status:

- The corporation must have only one class of stock.

- It must be a domestic corporation (owned by U.S. citizens).

- It must not have more than 100 shareholders (spouses are considered to be one shareholder).

- Shareholders generally cannot include corporations or partnerships (certain trusts, estates and tax-exempt corporations are permitted).

- Profits and losses must be allocated to shareholders proportionately to each one's interest in the business.

Limited Liability Company (LLC)

An LLC, like an S corporation, is a hybrid entity having certain characteristics of both a corporation and a partnership or sole proprietorship. The primary characteristic an LLC shares with a corporation is limited liability, and the primary characteristic it shares with a partnership is taxation on the ownership level. It differs from an S corporation in that there are no restrictions on the number or types of shareholders. It is actually a type of unincorporated association rather than a corporation.

Taxable Income

In the United States, taxable income for a corporation is defined as all gross income (sales plus other income minus cost of goods sold and tax exempt income) less allowable tax deductions and tax credits. This income is taxed at a specified corporate tax rate. This rate varies by jurisdiction and is generally the same for different types of income. Some systems have graduated tax rates - corporations with lower levels of income pay a lower rate of tax - or impose tax at different rates for different types of corporations.

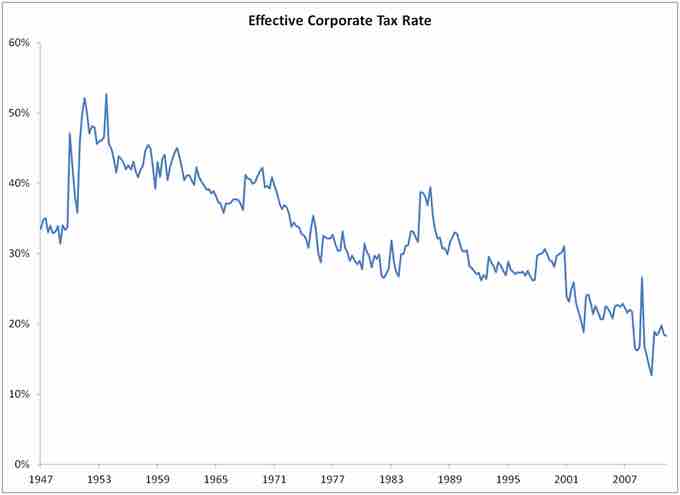

US Corporate Tax Rates

This graph shows the effect of corporate tax rates in the U.S. from 1947 through 2012.

In the US, federal rates range from 15% to 35%. States charge rates ranging from 0% to 10%, deductible in computing federal taxable income. Some cities charge rates up to 9%, also deductible in computing Federal taxable income. Corporations are also subject to property tax, payroll tax, withholding tax, excise tax, customs duties and value added tax. However, these are rarely referred to as "corporate tax."