Working Capital = current assets - current liabilities.

Working capital (WC) can be controlled by changing the levels of current assets and/or current liabilities through a number of mechanisms.

Working capital (WC) is a measurement of a company's operating liquidity.

Working capital needs will vary depending on the type of the business and its operational requirements.

Recognize the broader objectives of working capital, and the way in which organizations can consider a long-term perspective when viewing the utilization of working capital.

Decisions relating to working capital are usually short-term, since it is the difference between current assets and current liabilities.

A firm will use a combination of policies for managing working capital, focusing on cash flow, liquidity, profitability, and capital return.

Management of working capital requires evaluating factors affecting cash flows -- including the evaluation of appropriate interest rates.

The main considerations of working capital management decisions are (1) cash flow/ liquidity and (2) profitability/return on capital.

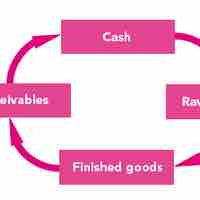

Management uses policies and techniques for the management of working capital such as cash, inventory, debtors and short term financing.

The main accounts which affect the value of working capital are accounts receivable, inventory, and accounts payable.