Impact of Type of Insurance Plan on Access and Utilization of Health Care Services for Adults Aged 18-64 Years With Private Health Insurance: United States, 2007-2008

ShareCompartir

ShareCompartir

On This Page

- Key findings

- In 2007-2008, 18% of adults aged 18-64 years with private health insurance were enrolled in an HDHP, including 5% who were enrolled in a CDHP.

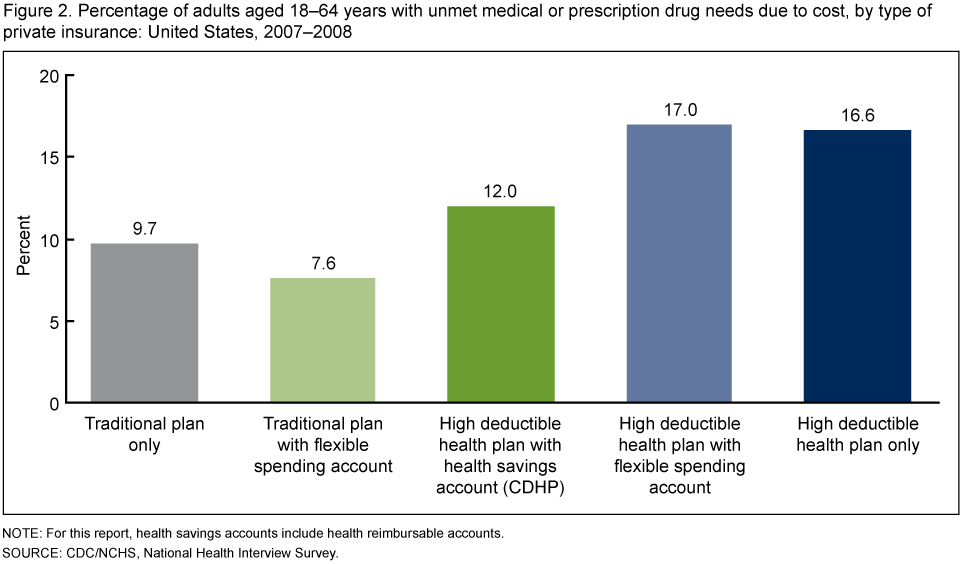

- Adults aged 18-64 years enrolled in an HDHP-only or an HDHP FSA were more likely to report unmet medical or prescription drug needs due to cost than adults enrolled in a traditional health plan with or without an FSA.

- Adults aged 18-64 years with either an FSA or an HSA were more likely to get an influenza vaccination than those without an FSA or an HSA.

- Adults aged 18-64 years with either an FSA or an HSA were more likely to have contact with an eye doctor than those without an FSA or an HSA.

- Adults aged 18-64 years with an FSA were more likely to have had contact with a medical specialist within the past year than those without an FSA.

- Summary

- Definitions

- Data source and methods

- About the author

- References

- Suggested citation

NCHS Data Brief No. 28, February 2010

PDF Version (987 KB)

by Robin A. Cohen, Ph.D.

Key findings

Data from the National Health Interview Survey

- Almost 18% of adults under age 65 with private health insurance were enrolled in some type of high deductible health plan (HDHP), including 5% who were enrolled in a consumer-directed health plan (CDHP), 2% with a flexible spending account (FSA) for medical expenses, and 12% in a HDHP-only plan.

- Approximately 17% of adults aged 18-64 years enrolled in an HDHP had unmet medical or prescription drug needs due to cost, compared with 10% among adults aged 18-64 years enrolled in a traditional health plan only (no FSA).

- Privately insured adults aged 18-64 years with an FSA or health savings account (HSA) were more likely to receive a flu shot or have contact with an eye doctor in the past 12 months than those with neither an FSA nor an HSA.

National attention to consumer-directed health care has increased following the enactment of the Medicare Prescription Drug Improvement and Modernization Act of 2003 (P.L. 108-173), which established tax-advantaged health savings accounts (HSAs) (1). Enrollment in consumer-directed health care products has increased over the past several years (2). Consumer-directed health care may enable individuals to have more control over when and how they access care, what types of care they use, and how much they spend on health care services. This report ex-amines types of private health plans and their association with utilization and access to health care services for adults aged 18-64 years in 2007-2008.

Keywords: High deductible plan, consumer-directed plan, flexible spending account, National Health Interview Survey

In 2007-2008, 18% of adults aged 18-64 years with private health insurance were enrolled in an HDHP, including 5% who were enrolled in a CDHP.

In 2007-2008, four out of five adults aged 18-64 years with private health insurance were en-rolled in a traditional health plan (Figure 1), including 68% without an FSA and 14% with an FSA (Traditional plan + FSA).

Adults aged 18-64 years enrolled in an HDHP-only or an HDHP + FSA were more likely to report unmet medical or prescription drug needs due to cost than adults enrolled in a traditional health plan with or without an FSA.

Seventeen percent of adults aged 18-64 years enrolled in an HDHP + FSA and 16.6% enrolled in an HDHP-only had an unmet medical or prescription drug need due to cost compared with 9.7% of adults aged 18-64 years enrolled in a traditional health plan without an FSA (Figure 2). Adults enrolled in a traditional plan + FSA were less likely to have unmet medical or prescription drug needs (7.6%) compared with adults enrolled in a traditional health plan only. Twelve per-cent of adults aged 18-64 years enrolled in a CDHP had an unmet medical or prescription drug need.

Adults aged 18-64 years with either an FSA or an HSA were more likely to get an influenza vaccination than those without an FSA or an HSA.

The percentage of adults aged 18-64 years with private health insurance who received an influenza vaccination in the past 12 months was highest among those enrolled in a traditional plan + FSA (37.5%), an HDHP + FSA (36.3%), or a CDHP (33.6%) (Figure 3). Adults aged 18-64 years covered by either a traditional plan only (26.7%) or an HDHP-only (25.8%) had lower rates of receiving an influenza vaccination in the past 12 months.

Adults aged 18-64 years with either an FSA or an HSA were more likely to have contact with an eye doctor than those without an FSA or an HSA.

The percentage of adults aged 18-64 years with private health insurance who had seen or talked to an eye doctor in the past 12 months was highest among those enrolled in a HDHP + FSA (52.2%), a traditional plan + FSA (48.2%), or a CDHP (45.4%) (Figure 4). Adults aged 18-64 years covered by either a traditional plan only (36.4%) or an HDHP-only (36.8%) had lower rates of having contact with an eye doctor in the past 12 months.

Adults aged 18-64 years with an FSA were more likely to have had contact with a medical specialist within the past year than those without an FSA.

The percentage of adults aged 18-64 years with private health insurance who had contact with a medical specialist in the past 12 months was highest among those who had a traditional plan + FSA (30.8%) or an HDHP + FSA (34.6%) (see Table). Adults aged 18-64 years with a tradi-tional plan only had the lowest rate of contact with a medical specialist in the past 12 months (23.9%).

The percentage of adults aged 18-64 years who had at least one contact with a dentist in the past 12 months ranged from 68.0% among those enrolled in an HDHP-only plan to 82.5% en-rolled in a traditional plan + FSA. Almost 71% of adults aged 18-64 years enrolled in a tradi-tional plan only had contact with a dentist in the past 12 months.

Most privately insured adults aged 18-64 years had a usual source of medical care. The per-centage who had a usual source of medical care ranged from 87.7% among those enrolled in an HDHP-only plan to 92.5% among those enrolled in a traditional plan + FSA.

The percentage of adults aged 18-64 years who had at least one contact with a doctor or other health care professional in the past 12 months ranged from 83.8% among those enrolled in an HDHP-only to 89.8% for those enrolled in an HDHP + FSA.

Table. Percentage (with standard errors) of privately insured adults aged 18-64 years with selected types of health care access and utilization of health services, by type of private health insurance: United States, 2007-2008

| Type of private health insurance | Has a usual source of medical care1 | At least one contact with a doctor or other health care professional in the past 12 months | At least one contact with a dentist or dental professional in the past year2 | At least one contact with a medical specialist in the past 12 months |

|---|---|---|---|---|

| Percent (standard error) | ||||

| Traditional plan3 only | 91.0 (0.33) | 85.8 (0.39) | 70.6 (0.52) | 23.9 (0.44) |

| Traditional plan3 with FSA4 | 92.5 (0.63) | 89.3 (0.75) | 82.5 (0.88) | 30.8 (1.12) |

| HDHP5 with HSA6 (CDHP)7 | 90.7 (1.38) | 86.0 (1.58) | 77.2 (2.10) | 27.3 (1.80) |

| HDHP5 with FSA4 | 92.3 (1.79) | 89.8 (2.14) | 77.3 (3.82) | 34.6 (3.61) |

| HDHP5 only | 87.7 (0.95) | 83.8 (0.98) | 68.0 (1.17) | 26.0 (1.15) |

1 Persons with a usual source of medical care have a place that they usually go to when they are sick or need advice about their health. Persons who mentioned that the hospital emergency room was their usual source of medical care were considered not to have a usual source of medical care.

2 The data in this table are based on a question in the survey that asked respondents, “About how long has it been since you last saw a dentist?” Respondents are instructed to include all types of dentists, such as orthodontists, oral surgeons, and all other dental specialists, as well as dental hygienists.

3 A traditional plan is a private health plan with an annual deductible of less than $1,100 for self-only coverage or $2,200 for family coverage for 2007 and 2008.

4 FSA is a flexible spending account for medical expenses that must be used within a specified time.

5 HDHP is a high deductible health plan. An HDHP is a private plan with an annual deductible of not less than $1,100 for self-only coverage or $2,200 for family coverage for 2007 and 2008.

6 HSA is a health savings account. For this analysis HSAs also include Health Reimbusible Accounts (HRAs). Any unspent funds in these accounts are carried over to subsequent years.

7 CDHP is a consumer directed health plan. A CDHP is a High Deductible Health Plan (HDHP) coupled with a HSA.

SOURCE: CDC/NCHS, National Health Interview Survey. Estimates are based on household interviews of a sample of the civilian noninstitutionalized population.

Summary

Although HDHPs and CDHPs still comprise a relatively small share of the private health insur-ance market, their market share has increased (2). The use of FSAs has also increased. Pri-vately insured adults aged 18-64 years with HDHPs were more likely to experience unmet medical and prescription drug needs compared with individuals enrolled in traditional health plans and CDHPs. For privately insured adults aged 18-64 years, having either an FSA or an HSA was associated with increased health care utilization for influenza vaccination, dental vis-its, and eye doctor visits, which are services typically paid out of pocket by consumers.

Definitions

Private insurance: Is indicated when respondents report that they were covered at the time of the interview by private health insurance through an employer or union, or if they purchased a policy on their own. Private health insurance includes managed care such as health maintenance organi-zations (HMOs). It does not include military health plans.

High deductible health plan (HDHP): Private health plan with an annual deductible of not less than $1,100 for self-only coverage or $2,200 for family coverage for 2007 and 2008.

Traditional plan: Private health plan with an annual deductible of less than $1,100 for self-only coverage or $2,200 for family coverage for 2007 and 2008.

Consumer-directed health plan (CDHP): Account that is offered by some employers to allow employees to set aside pre-tax dollars of their own money for their use throughout the year to reimburse themselves for their out-of-pocket expenses for health care. For this type of account, any money remaining in the account at the end of the year, following a short grace period, is lost to the employee. A person was considered to by covered by an FSA based on a “yes” response to the question “With this plan, is there a special account or fund that can be used to pay for medical expenses? The accounts are sometimes referred to as Health Savings Accounts (HSAs), Health Reimbursement Accounts (HRAs), Personal Care Accounts, Personal medical funds, or Choice funds, and are different from Flexible Spending Accounts.”

Health Savings Account (HSA): For this report, HSAs also includes HRAs.

Flexible spending account (FSA): An HDHP with a special account to pay for medical expenses; unspent funds are carried over to subsequent years. A person is considered to have a CDHP if there was a “yes” response to the following question: “Do you or anyone in your family have a Flexible Spending Account for health expenses? These accounts are offered by some employers to allow employees to set aside pre-tax dollars of their own money for their use throughout the year to reimburse themselves for their out-of-pocket expenses for health care. With this type of account, any money remaining in the account at the end of the year, following a short grace period, is lost to the employee.”

Persons who were covered by a CDHP and who also had a family member with an FSA were considered not to be covered by an FSA.

Dental contact: Dental contact is based on a question in the survey that asked respondents, “About how long has it been since you last saw a dentist?” Respondents are instructed to include all types of dentists, such as orthodontists, oral surgeons, and all other dental specialists, as well as dental hygienists.

Doctor or other health professional: Doctor refers to medical doctor (M.D.) and osteopathic physician (D.O.), including general practitioners and all types of specialists (such as internists, gynecologists, obstetricians, psychiatrists, and ophthalmologists). Other health care professional includes physician assistants, psychologists, nurses, physical therapists, chiropractors, etc.

Emergency room visit: Includes emergency room visits that resulted in a hospital admission.

Influenza vaccination: Includes both the flu shot and the nasal spray.

Doctor or other health care professional contact: This may include a contact while a person is in the hospital as well as a contact from a home visit, but not a contact made to arrange appointments.

Unmet need: A person was considered to have an unmet need if he or she delayed or did not get medical care due to cost or did not get a prescription drug due to cost in the past 12 months.

Usual source of care: Usual source of care was measured by asking the respondent, “Is there a place that you USUALLY go when you are sick or need advice about your health?” Persons who report the emergency department as their usual source of care are defined as having no usual source of care in this report.

Most access and utilization measures in this report are based on the 12 months prior to inter-view, with the exception of a usual source of care. Usual source of care is a person’s status at the time of interview. Insurance coverage is also a person’s status at the time of interview. Therefore, an individual’s insurance status may have been different at the time health services were sought or received. This analysis does not take into account single service dental plans, which may have an impact on use of dental services.

Data source and methods

Data from the 2007 and 2008 National Health Interview Survey (NHIS) were used for this analy-sis. NHIS collects information about the health and health care of the civilian noninstitutionalized population in the United States. Interviews are conducted in the respondents’ households primarily, but follow-ups in order to complete interviews may be conducted over the telephone. Questions about health insurance coverage are asked of family respondents in the family component of the survey. The questions may be viewed on the NHIS website. Most questions on access and utilization are from the sample adult component of the NHIS. However, questions on unmet medical need due to cost are from the family core component of the NHIS. Only persons aged 18-64 years with private health in-surance were included in this analysis. The questions about HDHPs, CDHPs, and FSAs were first included in the 2007 NHIS. Detailed questions about private health insurance plans are asked on a plan basis. Information is collected on up to four private health insurance plans per family. Questions about HDHPs and CDHPs were asked for each private health insurance plan. The question about FSAs was asked on a family basis and includes all persons in the family without regard to insurance status. In 2007 and 2008, 92,450 persons aged 18-64 years were included in the family core component on the NHIS and 36,147 persons aged 18-64 years were included in the sample adult component of the NHIS.

NHIS is designed to yield a nationally representative sample, and this analysis uses weights to produce national estimates. Data weighting procedures are described in more detail elsewhere (3) (NHIS Methods). Point estimates and estimates of corresponding variances for this analysis were calculated using the SUDAAN software package (4) to account for the complex sample design of the NHIS. The Taylor series linearization method was chosen for variance estimation. All estimates shown meet the National Center for Health Statistics (NCHS) standard for having a relative standard error less than or equal to 30%. Differences between percentages were evaluated using two-sided significance tests at the 0.05 level. Terms such as “similar” and “no difference” indicate that the statistics being compared were not significantly different. Lack of comment regarding the difference between any two sta-tistics does not necessarily suggest that the difference was tested and found to not be significant.

NHIS is conducted continuously throughout the year by interviewers of the U.S. Census Bureau for the Centers for Disease Control and Prevention’s NCHS. For further information about NHIS, see the NHIS website.

About the author

Robin A. Cohen is with the Centers for Disease Control and Prevention’s National Center for Health Statistics, Division of Health Interview Statistics.

References

- United States Government Accountability Office. Consumer-directed health plans: Early enrollee experiences with health savings accounts and eligible health plans. GAO-06-798. Washington. 2006.

- Martinez ME, Cohen RA. Health insurance coverage: Early release of estimates from the National Health Interview Survey, January-June 2009. Hyattsville, MD: National Center for Health Statistics. December 2009.

- Botman SL, Moore TF, Moriarity CL, Parsons VL. Design and estimation for the National Health Interview Survey, 1995-2004. National Center for Health Statistics. Vital Health Stat 2(130). 2000.

- Research Triangle Institute. SUDAAN (Release 9.1). Research Triangle Park, NC: Re-search Triangle Institute. 2004.

Suggested citation

Cohen RA. Impact of type of insurance plan on access and utilization of health care services for adults aged 18-64 years with private health insurance: United States, 2007-2008. NCHS data brief, no 28. Hyattsville, MD: National Center for Health Statistics. 2010.

Copyright information

All material appearing in this report is in the public domain and may be reproduced or copied without permission; citation as to source, however, is appreciated.

National Center for Health Statistics

Edward J. Sondik, Ph.D., Director

Jennifer H. Madans, Ph.D., Associate Director for Science

Division of Health Interview Statistics

Jane F. Gentleman, Ph.D., Director

- Page last reviewed: November 6, 2015

- Page last updated: February 10, 2010

- Content source: