Gains within a market are referred to as total welfare or economic surplus. Within total welfare, economists look at consumer surplus and producer surplus . A surplus is defined as the excess of a good or service when the quantity supplied exceeds the quantity demanded; this occurs when the price is above the equilibrium price.

Economic Surpluses

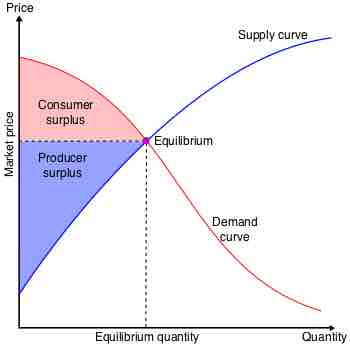

The total welfare (or economic surplus) is the sum of the consumer surplus and the producer surplus.

Consumer surplus is the monetary gain that consumers receive when they purchase a good for less than the highest price they are willing to pay. For example, a customer is willing to pay $50 for a new pair of running shoes. They are able to purchase the pair for $35 and consumer surplus is $15.

Producer surplus is the amount that producers benefit by selling a good at a market price that is higher than the least that they would be willing to sell it for. An example would be a manufacturer that makes jeans. The lowest price the producer is willing to sell a pair of jeans for is $40, but the jeans actually sell for $50. The producer surplus is $10.

In order to calculate the total welfare, the supply and demand of the good must be used to determine the economic gain. On a demand and supply curve graph, the consumer surplus is located under the demand curve and above a horizontal line that shows the actual price of a good (equilibrium price).

When the supply of a good increases, the price falls which increases consumer surplus. When the demand for a good increases, the price increases and the supply decreases resulting in producer surplus. When a good is in high demand, consumers are willing to pay more in order to obtain the good.