Time to Maturity

"Time to maturity" refers to the length of time that can elapse before the par value (face value) for a bond must be returned to a bondholder. This time may be as short as a few months, or longer than 50 years. Once this time has been reached, the bondholder should receive the par value for their particular bond.

The issuer of a bond has to repay the nominal amount for that bond on the maturity date. After this date, as long as all due payments have been made, the issuer will have no further obligations to the bondholders. The length of time until a bond's matures is referred to as its term, tenor, or maturity. These dates can technically be any length of time, but debt securities with a term of less than one year are generally not designated as bonds. Instead, they are designated as money market instruments .

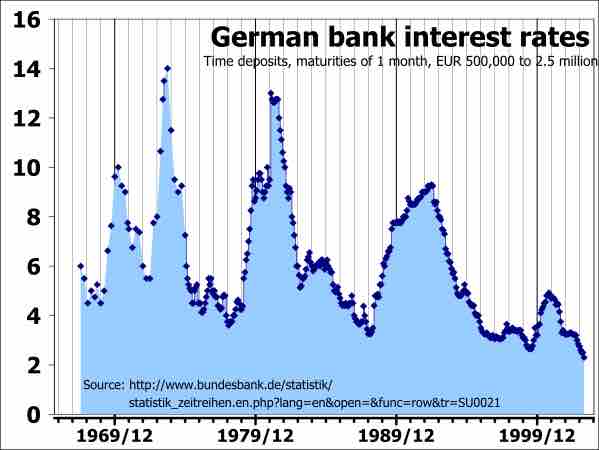

Money market interest rates

Interest rates of one-month maturity of German banks from 1967 to 2003

Most bonds have a term of up to 30 years. That being said, bonds have been issued with terms of 50 years or more, and historically, issues have arisen where bonds completely lack maturity dates (irredeemables). In the market for United States Treasury securities, there are three categories of bond maturities:

- Short term (bills): maturities between one to five years (Instruments that mature in less than one year are considered Money Market Instruments. )

- Medium term (notes): maturities between six to twelve years

- Long term (bonds): maturities greater than twelve years

Because bonds with long maturities necessarily have long durations, the bond prices in these situations are more sensitive to interest rate changes. In other words, the price risk of such bonds is higher. The fair price of a "straight bond," a bond with no embedded options, is usually determined by discounting its expected cash flows at the appropriate discount rate. Although this present value relationship reflects the theoretical approach to determining the value of a bond, in practice, the price is (usually) determined with reference to other, more liquid instruments.

In general, coupon and par value being equal, a bond with a short time to maturity will trade at a higher value than one with a longer time to maturity. This is because the par value is discounted at a higher rate further into the future.

Finally, it is important to recognize that future interest rates are uncertain, and that the discount rate is not adequately represented by a single fixed number (this would be the case if an option was written on the bond in question) stochastic calculus may be employed. Where the market price of a bond is less than its face value (par value), the bond is selling at a discount. Conversely, if the market price of bond is greater than its face value, the bond is selling at a premium.