Economic growth is the increase in the amount of the goods and services produced by an economy over time. It is conventionally measured as a percentage change in the Gross Domestic Product (GDP) or Gross National Product (GNP). These two measures, which are calculated slightly differently, total the amounts paid for the goods and services that a country produced. As an example of measuring economic growth, a country that creates 9,000,000 in goods and services in 2010 and then creates 9,090,000 in 2011 has a nominal economic growth rate of 1% for 2011.

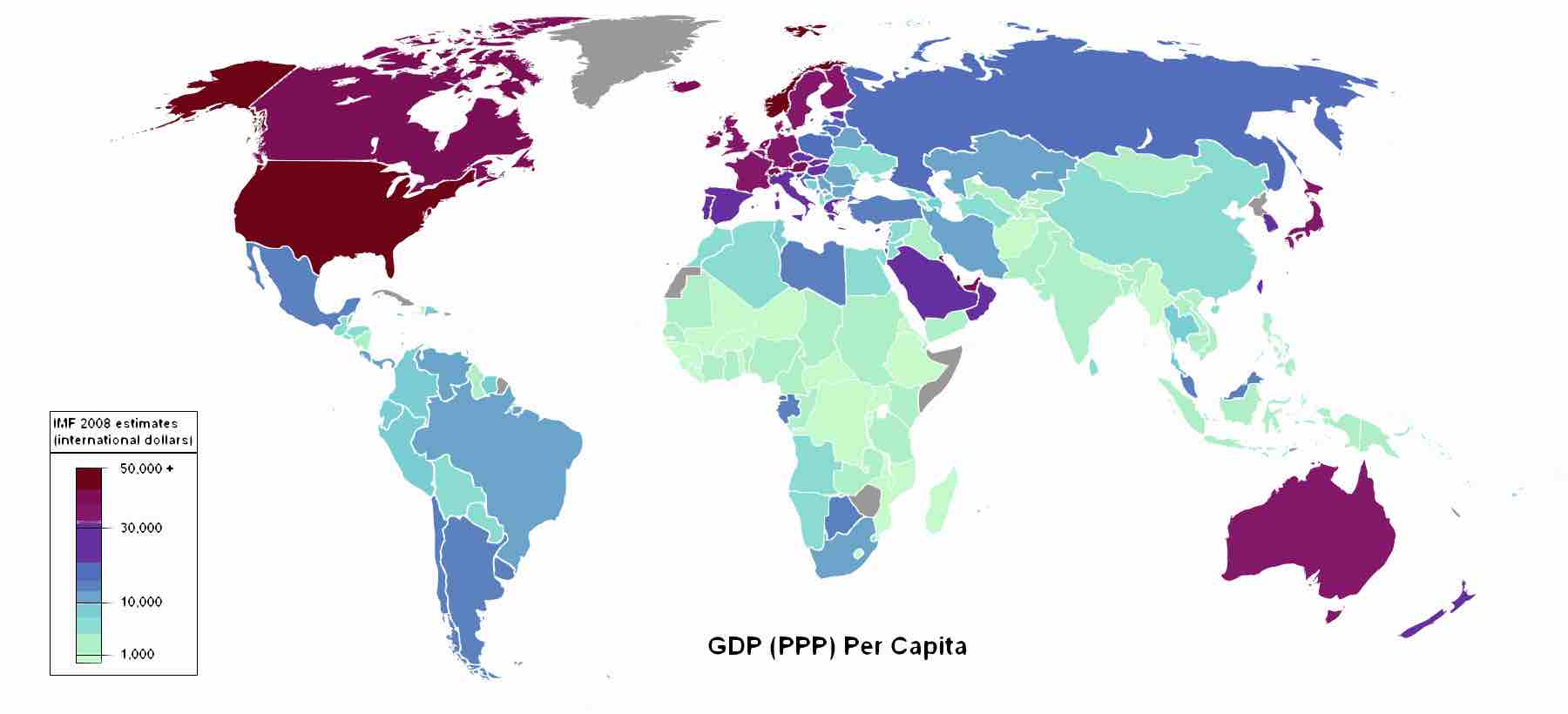

Map of GDP Per Capita (2008)

The GDP of economies across the globe.

In order to compare per capita economic growth among countries, the total sales of the countries to be compared may be quoted in a single currency. This requires converting the value of currencies of various countries into a selected currency, for example U.S. dollars. One way to do this conversion is to rely on exchange rates among the currencies, for example, how many Mexican pesos buy a single U.S. dollar? Another approach is to use the purchasing power parity method. This method is based on how much consumers must pay for the same "basket of goods" in each country.

Inflation or deflation can make it difficult to measure economic growth. If GDP, for example, goes up in a country by 1% in a year, was this due solely to rising prices (inflation) or because more goods and services were produced and saved? To express real growth rather than changes in prices for the same goods, statistics on economic growth are often adjusted for inflation or deflation.

For example, a table may show changes in GDP in the period 1990 to 2000, as expressed in 1990 U.S. dollars. This means that the single currency being used is the U.S. dollar, with the purchasing power it had in the U.S. in 1990. The table might mention whether the figures are "inflation-adjusted" or real. If no adjustments were made for inflation, the table might make no mention of inflation-adjustment or might mention that the prices are nominal.

A way of classifying the economic growth of countries is to divide them into three groups: (a) industrialized, (b) developing, and (c) less-developed nations. The industrialized nations are generally considered to be the United States, Japan, Canada, Russia, Australia and most of Western Europe. The economies of these nations are characterized by private enterprise and a consumer orientation. They have high literacy, modem technology, and higher per capita incomes. Developing nations are those that are making the transition from economies based on agricultural and raw materials production to industrial economies. Many Latin American nations fit into this category, and they exhibit rising levels of education, technology, and per capita incomes. Finally, there are many less-developed nations in today's world. These nations have low standards of living, low literacy rates, and very limited technology.

Usually, the most significant marketing opportunities exist among the industrialized nations, as they have higher levels of income, one of the necessary ingredients for the formation of markets. However, most industrialized nations also have stable population bases, and market saturation for many products already exists.

The developing nations, on the other hand, have growing population bases, and although they currently import limited goods and services, there exists a long-run potential for growth in these nations. Dependent societies seek products that satisfy basic needs like food, clothing, housing, medical care, and education. Marketers in such nations must be educators, emphasizing information in their market programs. As the degree of economic development increases, so does the sophistication of the marketing effort focused on the countries.