Latin American debt crisis

The Latin American debt crisis (Spanish: Crisis de la deuda latinoamericana; Portuguese: Crise da dívida latino-americana) was a financial crisis that originated in the early 1980s (and for some countries starting in the 1970s), often known as La Década Perdida (The Lost Decade), when Latin American countries reached a point where their foreign debt exceeded their earning power, and they could not repay it.

Origins

In the 1960s and 1970s, many Latin American countries, notably Brazil, Argentina, and Mexico, borrowed huge sums of money from international creditors for industrialization, especially infrastructure programs.[1][2] These countries had soaring economies at the time, so the creditors were happy to provide loans. Initially, developing countries typically garnered loans through public routes like the World Bank. After 1973, private banks had an influx of funds from oil-rich countries which believed that sovereign debt was a safe investment.[3] Mexico borrowed against future oil revenues with the debt valued in US dollars, so that when the price of oil collapsed, so did the Mexican economy.

Between 1975 and 1982, Latin American debt to commercial banks increased at a cumulative annual rate of 20.4 percent. This heightened borrowing led Latin America to quadruple its external debt from US$75 billion in 1975 to more than $315 billion in 1983, or 50 percent of the region's gross domestic product (GDP). Debt service (interest payments and the repayment of principal) grew even faster as global interest rates surged, reaching $66 billion in 1982, up from $12 billion in 1975.[4]

History

When the world economy went into recession in the 1970s and 1980s, and oil prices skyrocketed, it created a breaking point for most countries in the region. Developing countries found themselves in a desperate liquidity crunch. Petroleum-exporting countries, flush with cash after the oil price increases of 1973–1980, invested their money with international banks, which "recycled" a major portion of the capital as syndicated loans to Latin American governments.[5][1] The sharp increase in oil prices caused many countries to search out more loans to cover the high prices, and even some oil-producing countries took on substantial debt for economic development, hoping that high prices would persist and allow them to repay their debt.[3]

As interest rates increased in the United States of America and in Europe in 1979, debt payments also increased, making it harder for borrowing countries to pay back their debts.[7] Deterioration in the exchange rate with the US dollar meant that Latin American governments ended up owing tremendous quantities of their national currencies, as well as losing purchasing power.[8] The contraction of world trade in 1981 caused the prices of primary resources (Latin America's largest export) to fall.[8]

While the dangerous accumulation of foreign debt occurred over a number of years, the debt crisis began when the international capital markets became aware that Latin America would not be able to repay its loans.[9] This occurred in August 1982 when Mexico's Finance Minister, Jesús Silva-Herzog, declared that Mexico would no longer be able to service its debt.[10] Mexico stated that it could not meet its payment due dates, and announced unilaterally a moratorium of 90 days; it also requested a renegotiation of payment periods and new loans in order to fulfill its prior obligations.[8]

In the wake of Mexico's sovereign default, most commercial banks reduced significantly or halted new lending to Latin America. As much of Latin America's loans were short-term, a crisis ensued when their refinancing was refused. Billions of dollars of loans, which previously would have been refinanced, were now due immediately.

The banks had to somehow restructure the debts to avoid financial panic; this usually involved new loans with very strict conditions, as well as the requirement that the debtor countries accept the intervention of the International Monetary Fund (IMF).[8] There were several stages of strategies to slow and end the crisis. The IMF moved to restructure the payments and reduce government spending in debtor countries.[11] Later it and the World Bank encouraged open markets.[12][13] Finally, the US and the IMF pushed for debt relief, recognizing that countries could not fully repay the large sums they owed.[14]

However, some unorthodox economists like Stephen Kanitz attribute the debt crisis not to the high level of indebtedness nor to the disorganization of the continent's economy. They say that the cause of the crisis was leverage limits such as US government banking regulations which forbid its banks from lending over ten times the amount of their capital, a regulation that, when the inflation eroded their lending limits, forced them to cut the access of underdeveloped countries to international savings.[15]

Effects

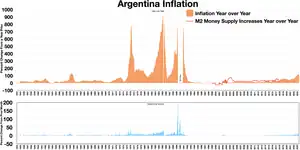

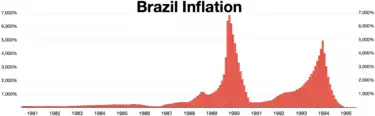

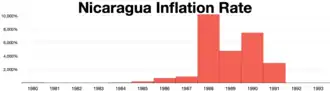

The debt crisis of 1982 was the most serious of Latin America's history. Incomes and imports dropped; economic growth stagnated; unemployment rose to high levels; and inflation reduced the buying power of the middle classes.[8] In fact, in the ten years after 1980, real wages in urban areas actually dropped between 20 and 40 percent.[12] Additionally, investment that might have been used to address social issues and poverty was instead being used to pay the debt.[3] Losses to bankers in the United States were catastrophic, perhaps more than the banking industry's entire collective profits since the nation's founding in the late 1700s.[16]

In response to the crisis, most nations abandoned their import substitution industrialization (ISI) models of economy and adopted an export-oriented industrialization strategy, usually the neoliberal strategy encouraged by the IMF, although there were exceptions such as Chile and Costa Rica, which adopted reformist strategies. A massive process of capital outflow, particularly to the United States, served to depreciate the exchange rates, thereby raising the real interest rate. Real GDP growth rate for the region was only 2.3 percent between 1980 and 1985, but in per capita terms Latin America experienced negative growth of almost 9 percent. Between 1982 and 1985, Latin America paid back US$108 billion.[8]

International Monetary Fund

Before the crisis, Latin American countries such as Brazil and Mexico borrowed money to enhance economic stability and reduce the poverty rate. However, as their inability to pay back their foreign debts became apparent, loans ceased, stopping the flow of resources previously available for the innovations and improvements of the previous few years. This rendered several half-finished projects useless, contributing to infrastructure problems in the affected countries.[17]

During the international recession of the 1970s, many major countries attempted to slow down and stop inflation in their countries by raising the interest rates of the money that they loaned, causing Latin America's already enormous debt to increase further. Between the years of 1970 to 1980, Latin America's debt levels increased by more than one thousand percent.[17]

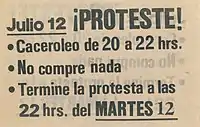

The crisis caused per capita income to drop and also increased poverty as the gap between the wealthy and poor increased dramatically. Due to plummeting employment rates, children and young adults were forced into the drug trade, prostitution and terrorism.[18] Low employment also worsened many problems like crime and generally reduced quality of life in the affected countries. Frantically trying to solve these problems, debtor countries felt constant pressure to repay their debts, increasing the difficulty of rebuilding ruined economies.

Latin American countries, unable to pay their debts, turned to the IMF (International Monetary Fund), which provided money for loans and unpaid debts. In return, the IMF forced Latin America to make reforms that would favor free-market capitalism, further aggravating inequalities and poverty conditions.[19] The IMF also forced Latin America to implement austerity plans and programs that lowered total spending in an effort to recover from the debt crisis. This reduction in government spending further deteriorated social fractures in the economy and halted industrialisation efforts.

Latin America's growth rate and living standards fell dramatically due to government austerity plans that restricted further spending, creating popular rage towards the IMF, a symbol of "outsider" power over Latin America.[20] Government leaders and officials were ridiculed and some even discharged due to involvement and defending of the IMF. In the late 1980s, Brazilian officials planned a debt negotiation meeting where they decided to "never again sign agreements with the IMF".[21] The result of IMF intervention caused greater financial deepening (Financialization) and dependence on the developed world capital flows, as well as increased exposure to international volatility.[22] The application of structural adjustment programs entailed high social costs in terms of rising unemployment and underemployment, falling real wages and incomes, and increased poverty.

2015 levels of external debt

The following is a list of external debt for Latin America based on a 2015 report by The World Factbook.[23]

| Rank | Country – Entity | External Debt (million US$) | Date of information |

|---|---|---|---|

| 24 | Brazil | 535,400 | 31 Dec 2014 est. |

| 26 | Mexico | 438,400 | 31 Dec 2014 est |

| 42 | Chile | 140,000 | 31 Dec 2014 est. |

| 45 | Argentina | 115,700 | 31 Dec 2014 est. |

| 51 | Colombia | 84,000 | 31 Dec 2014 est. |

| 52 | Venezuela | 69,660 | 31 Dec 2014 est. |

| 60 | Peru | 56,470 | 31 Dec 2014 est. |

| 79 | Cuba | 25,230 | 31 Dec 2014 est. |

| 83 | Ecuador | 21,740 | 31 Dec 2014 est. |

| 84 | Dominican Republic | 19,720 | 31 Dec 2014 est. |

| 86 | Costa Rica | 18,370 | 31 Dec 2014 est. |

| 88 | Uruguay | 17,540 | 31 Dec 2014 est. |

| 93 | Guatemala | 15,940 | 31 Dec 2014 est. |

| 94 | Panama | 15,470 | 31 Dec 2014 est. |

| 95 | El Salvador | 15,460 | 31 Dec 2014 est. |

| 103 | Nicaragua | 10,250 | 31 Dec 2014 est. |

| 106 | Paraguay | 8,759 | 31 Dec 2014 est. |

| 108 | Bolivia | 8,073 | 31 Dec 2014 est. |

| 117 | Honduras | 7,111 | 31 Dec 2014 est. |

See also

References

- "Global Waves of Debt: Causes and Consequences". World Bank. Retrieved 13 May 2022.

- Diaz-Alejandro, Carlos F. (1 June 1984). "Latin American Debt: I Don't Think We are in Kansas Anymore". Brookings. Retrieved 13 May 2022.

- Ferraro, Vincent (1994). World Security: Challenges for a New Century. New York: St. Martin's Press.

- Institute of Latin American Studies, The Debt Crisis in Latin America, p. 69

- Gadanecz, Blaise (6 December 2004). "The syndicated loan market: structure, development and implications".

{{cite journal}}: Cite journal requires|journal=(help) - "Will the FED Strangle Latin America Again?".

- Schaeffer, Robert. Understanding Globalization, p. 96

- García Bernal, Manuela Cristina (1991). "Iberoamérica: Evolución de una Economía Dependiente". In Luís Navarro García (Coord.), Historia de las Américas, vol. IV, pp. 565–619. Madrid/Sevilla: Alhambra Longman/Universidad de Sevilla. ISBN 978-84-205-2155-8

- Cline, William R. (February 1995). International Debt Reexamined. Peterson Institute for International Economics. ISBN 978-0-88132-083-1.

- Pastor, Robert A. Latin American Debt Crisis: Adjusting for the Past or Planning for the Future, p. 9

- Sachs, J. D. (1989). "New Approaches To The Latin American Debt Crisis".

{{cite journal}}: Cite journal requires|journal=(help) - Felix, David (Fall 1990). "Latin America's Debt Crisis". World Policy Journal. 7 (4): 733–71.

- Devlin, Robert; Ricardo French-Davis (July–September 1995). "The great Latin American debt crisis: a decade of asymmetric adjustment". Revista de Economía Política. 15 (3).

- Krugman, Paul (2007). International Economics: Theory and Policy. Pearson Education.

- Kanitz, Stephen. "Brazil: The Emerging Boom 1993–2005 Chapter 2". brazil.melhores.com.br. Archived from the original on 5 August 2017. Retrieved 22 February 2009.

- Nassim Nicholas Taleb (2007). The Black Swan: The Impact of the Highly Improbable. Random House.

- "Encyclopædia Britannica Online School Edition". Encyclopædia Britannica. Retrieved 21 May 2012.

- Ruggiero, Gregory. "Latin American Debt Crisis: What Were Its Causes And Is It Over?". AngelFire. Retrieved 15 May 2012.

- Ghosh, Jayati. The Economic and Social Effects of Financial Liberalization: A Primer for Developing Countries. Working Paper. United Nations, Department of Economics and Social Affairs, 2005.

- "Latin American debt crisis". ABC-CLIO. Retrieved 22 May 2012.

- Pastor, Manuel Jr. (1989). "Latin America, the Debt Crisis, and the International Monetary Fund". Latin American Perspectives. JSTOR. 16 (1): 79–110. doi:10.1177/0094582X8901600105. JSTOR 2633823. S2CID 144458701.

- Palma, Gabriel. The Three Routes to Financial Crises: The Need for Capital Controls. SCEPA Working Paper. Schwartz Center for Economic Policy Analysis (SCEPA), The New School, 2000.

- The World Factbook, 2015

Further reading

- Signoriello, Vincent J. (1991), Commercial Loan Practices and Operations, Chapter 8 Servicing Foreign Debt, Latin American Debt Crisis, Performing a Vital Service, ISBN 978-1-55520-134-0.

- Signoriello, Vincent J. (1985, Jan–Feb) International Correspondent Banker Magazine, London, England, Performing a Vital Service, The Future for Debt Rescheduling, pp. 44–45.

- Sunkel, Osvald and Stephany Griffith-Jones (1986), Debt and Development Crises in Latin America: The End of an Illusion, Oxford University Press.

- Pastor, Manuel (1993). "15: Managing the Latin American Debt Crisis: The International Monetary Fund and Beyond". In Gerald A. Epstein; Julie Graham; Jessica Gordon Nembhard (eds.). Creating a new world economy: forces of change & plans for action. Temple University Press. ISBN 978-1-56639-054-5.