Great Depression

Between 1929 and 1939[1] was a period of great economic depression worldwide that became evident after a major fall in stock prices in the United States.[2] The economic contagion began around September and led to the Wall Street stock market crash of October 24 (Black Thursday). The economic shock impacted most countries across the world to varying degrees. It was the longest, deepest, and most widespread depression of the 20th century.[3]

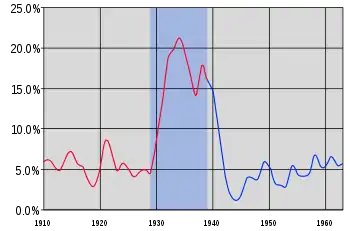

Between 1929 and 1932, worldwide gross domestic product (GDP) fell by an estimated 15%. By comparison, worldwide GDP fell by less than 1% from 2008 to 2009 during the Great Recession.[4] Some economies started to recover by the mid-1930s. However, in many countries, the negative effects of the Great Depression lasted until the beginning of World War II.[5] Devastating effects were seen in both rich and poor countries with falling personal income, prices, tax revenues, and profits. International trade fell by more than 50%, unemployment in the U.S. rose to 23% and in some countries rose as high as 33%.[6]

Cities around the world were hit hard, especially those dependent on heavy industry. Construction was virtually halted in many countries. Farming communities and rural areas suffered as crop prices fell by about 60%.[7][8][9] Faced with plummeting demand and few job alternatives, areas dependent on primary sector industries suffered the most.[10]

Economic historians usually consider the catalyst of the Great Depression to be the sudden devastating collapse of U.S. stock market prices, starting on October 24, 1929. However, some dispute this conclusion, seeing the stock crash less as a cause of the Depression and more as a symptom of the rising nervousness of investors partly due to gradual price declines caused by falling sales of consumer goods (as a result of overproduction because of new production techniques, falling exports and income inequality, among other factors) that had already been underway as part of a gradual Depression.[6][11]

Overview

After the Wall Street Crash of 1929, where the Dow Jones Industrial Average dropped from 381 to 198 over the course of two months, optimism persisted for some time. The stock market rose in early 1930, with the Dow returning to 294 (pre-depression levels) in April 1930, before steadily declining for years, to a low of 41 in 1932.[12]

At the beginning, governments and businesses spent more in the first half of 1930 than in the corresponding period of the previous year. On the other hand, consumers, many of whom suffered severe losses in the stock market the previous year, cut expenditures by 10%. In addition, beginning in the mid-1930s, a severe drought ravaged the agricultural heartland of the U.S.[13]

Interest rates dropped to low levels by mid-1930, but expected deflation and the continuing reluctance of people to borrow meant that consumer spending and investment remained low.[14] By May 1930, automobile sales declined to below the levels of 1928. Prices, in general, began to decline, although wages held steady in 1930. Then a deflationary spiral started in 1931. Farmers faced a worse outlook; declining crop prices and a Great Plains drought crippled their economic outlook. At its peak, the Great Depression saw nearly 10% of all Great Plains farms change hands despite federal assistance.[15]

The decline in the U.S. economy was the factor that pulled down most other countries at first; then, internal weaknesses or strengths in each country made conditions worse or better. Frantic attempts by individual countries to shore up their economies through protectionist policies – such as the 1930 U.S. Smoot–Hawley Tariff Act and retaliatory tariffs in other countries – exacerbated the collapse in global trade, contributing to the depression.[16] By 1933, the economic decline pushed world trade to one third of its level compared to four years earlier.[17]

Economic indicators

| United States | United Kingdom | France | Germany | |

|---|---|---|---|---|

| Industrial production | −46% | −23% | −24% | −41% |

| Wholesale prices | −32% | −33% | −34% | −29% |

| Foreign trade | −70% | −60% | −54% | −61% |

| Unemployment | +607% | +129% | +214% | +232% |

Course

Origins

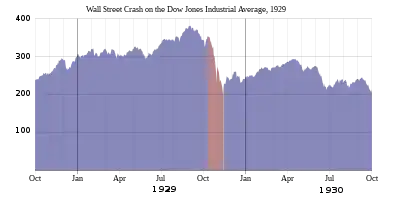

Because the Great Depression began in the United States and then spread around the world, the origins of the Great Depression are examined in the context of the United States economy. In the aftermath of World War I, the Roaring Twenties had brought considerable wealth to the United States and Western Europe.[19] 1929 dawned with considerable economic progress in the American economy. A small stock crash occurred on March 25, 1929, but the crash was stabilized. Despite signs of economic trouble, the market continued to improve through September. Stock prices began to slump in September, and were volatile at the end of September.[20] A large sell-off of stocks began in mid-October. Finally, on October 24, Black Thursday, the American stock market crashed 11% at the opening bell. Actions to stabilize the market failed, and on October 28, Black Monday, the market crashed another 12%. The panic peaked the next day on Black Tuesday, when the market saw another 11% drop.[21][22] Thousands of investors were ruined, and billions of dollars had been lost; many stocks could not be sold at any price.[22] The market recovered 12% on Wednesday, but the damage had been done. Though the market recovered from November 14, until April 17, 1930, the market entered a prolonged slump. From April 17, 1930, until July 8, 1932, the market lost 89% of its value.[23]

Despite the crash, the worst of the crisis did not reverberate around the world until after 1929. The crisis hit panic levels again in December 1930, with a bank run on the Bank of United States (privately run, no relation to the government). Unable to pay out to all of its creditors, the bank failed.[24][25] Among the 608 American banks that closed in November and December 1930, the Bank of United States accounted for a third of the total $550 million deposits lost and, with its closure, bank failures reached a critical mass.[26]

The Smoot-Hawley act and the breakdown of international trade

The Smoot–Hawley Tariff Act was passed in the United States on June 17, 1930, having been proposed the year prior. Ostensibly aimed at protecting the American economy as the Depression began to take root, it backfired enormously and may have even caused the Depression. The consensus view among economists and economic historians (including Keynesians, Monetarists and Austrian economists) is that the passage of the Smoot-Hawley Tariff exacerbated the Great Depression,[27] although there is disagreement as to how much. In the popular view, the Smoot-Hawley Tariff was a leading cause of the depression.[28][29] In a 1995 survey of American economic historians, two-thirds agreed that the Smoot–Hawley Tariff Act at least worsened the Great Depression.[30] According to the U.S. Senate website the Smoot–Hawley Tariff Act is among the most catastrophic acts in congressional history.[31]

Many economists have argued that the sharp decline in international trade after 1930 helped to worsen the depression, especially for countries significantly dependent on foreign trade. Most historians and economists blame the Act for worsening the depression by seriously reducing international trade and causing retaliatory tariffs in other countries. While foreign trade was a small part of overall economic activity in the U.S. and was concentrated in a few businesses like farming, it was a much larger factor in many other countries.[32] The average ad valorem (value based) rate of duties on dutiable imports for 1921–1925 was 25.9% but under the new tariff it jumped to 50% during 1931–1935. In dollar terms, American exports declined over the next four years from about $5.2 billion in 1929 to $1.7 billion in 1933; so, not only did the physical volume of exports fall, but also the prices fell by about 1⁄3 as written. Hardest hit were farm commodities such as wheat, cotton, tobacco, and lumber.

Governments around the world took various steps into spending less money on foreign goods such as: "imposing tariffs, import quotas, and exchange controls". These restrictions triggered much tension among countries that had large amounts of bilateral trade, causing major export-import reductions during the depression. Not all governments enforced the same measures of protectionism. Some countries raised tariffs drastically and enforced severe restrictions on foreign exchange transactions, while other countries reduced "trade and exchange restrictions only marginally":[33]

- "Countries that remained on the gold standard, keeping currencies fixed, were more likely to restrict foreign trade." These countries "resorted to protectionist policies to strengthen the balance of payments and limit gold losses." They hoped that these restrictions and depletions would hold the economic decline.[33]

- Countries that abandoned the gold standard, allowed their currencies to depreciate which caused their balance of payments to strengthen. It also freed up monetary policy so that central banks could lower interest rates and act as lenders of last resort. They possessed the best policy instruments to fight the Depression and did not need protectionism.[33]

- "The length and depth of a country's economic downturn and the timing and vigor of its recovery are related to how long it remained on the gold standard. Countries abandoning the gold standard relatively early experienced relatively mild recessions and early recoveries. In contrast, countries remaining on the gold standard experienced prolonged slumps."[33]

The gold standard and the spreading of global depression

The gold standard was the primary transmission mechanism of the Great Depression. Even countries that did not face bank failures and a monetary contraction first hand were forced to join the deflationary policy since higher interest rates in countries that performed a deflationary policy led to a gold outflow in countries with lower interest rates. Under the gold standard's price–specie flow mechanism, countries that lost gold but nevertheless wanted to maintain the gold standard had to permit their money supply to decrease and the domestic price level to decline (deflation).[34][35]

There is also consensus that protectionist policies, and primarily the passage of the Smoot–Hawley Tariff Act, helped to exacerbate, or even cause the Great Depression.[30]

Gold standard

Some economic studies have indicated that just as the downturn was spread worldwide by the rigidities of the gold standard, it was suspending gold convertibility (or devaluing the currency in gold terms) that did the most to make recovery possible.[37]

Every major currency left the gold standard during the Great Depression. The UK was the first to do so. Facing speculative attacks on the pound and depleting gold reserves, in September 1931 the Bank of England ceased exchanging pound notes for gold and the pound was floated on foreign exchange markets.

Japan and the Scandinavian countries joined the United Kingdom in leaving the gold standard in 1931. Other countries, such as Italy and the United States, remained on the gold standard into 1932 or 1933, while a few countries in the so-called "gold bloc", led by France and including Poland, Belgium and Switzerland, stayed on the standard until 1935–36.

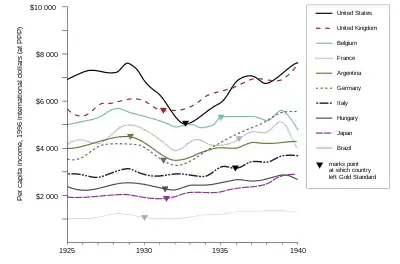

According to later analysis, the earliness with which a country left the gold standard reliably predicted its economic recovery. For example, The UK and Scandinavia, which left the gold standard in 1931, recovered much earlier than France and Belgium, which remained on gold much longer. Countries such as China, which had a silver standard, almost avoided the depression entirely. The connection between leaving the gold standard as a strong predictor of that country's severity of its depression and the length of time of its recovery has been shown to be consistent for dozens of countries, including developing countries. This partly explains why the experience and length of the depression differed between regions and states around the world.[38]

German banking crisis of 1931 and British crisis

The financial crisis escalated out of control in mid-1931, starting with the collapse of the Credit Anstalt in Vienna in May.[39][40] This put heavy pressure on Germany, which was already in political turmoil. With the rise in violence of Nazi and communist movements, as well as investor nervousness at harsh government financial policies,[41] investors withdrew their short-term money from Germany as confidence spiraled downward. The Reichsbank lost 150 million marks in the first week of June, 540 million in the second, and 150 million in two days, June 19–20. Collapse was at hand. U.S. President Herbert Hoover called for a moratorium on Payment of war reparations. This angered Paris, which depended on a steady flow of German payments, but it slowed the crisis down, and the moratorium was agreed to in July 1931. An International conference in London later in July produced no agreements but on August 19 a standstill agreement froze Germany's foreign liabilities for six months. Germany received emergency funding from private banks in New York as well as the Bank of International Settlements and the Bank of England. The funding only slowed the process. Industrial failures began in Germany, a major bank closed in July and a two-day holiday for all German banks was declared. Business failures were more frequent in July, and spread to Romania and Hungary. The crisis continued to get worse in Germany, bringing political upheaval that finally led to the coming to power of Hitler's Nazi regime in January 1933.[42]

The world financial crisis now began to overwhelm Britain; investors around the world started withdrawing their gold from London at the rate of £2.5 million per day.[43] Credits of £25 million each from the Bank of France and the Federal Reserve Bank of New York and an issue of £15 million fiduciary note slowed, but did not reverse the British crisis. The financial crisis now caused a major political crisis in Britain in August 1931. With deficits mounting, the bankers demanded a balanced budget; the divided cabinet of Prime Minister Ramsay MacDonald's Labour government agreed; it proposed to raise taxes, cut spending, and most controversially, to cut unemployment benefits 20%. The attack on welfare was unacceptable to the Labour movement. MacDonald wanted to resign, but King George V insisted he remain and form an all-party coalition "National Government". The Conservative and Liberals parties signed on, along with a small cadre of Labour, but the vast majority of Labour leaders denounced MacDonald as a traitor for leading the new government. Britain went off the gold standard, and suffered relatively less than other major countries in the Great Depression. In the 1931 British election, the Labour Party was virtually destroyed, leaving MacDonald as Prime Minister for a largely Conservative coalition.[44][45]

Turning point and recovery

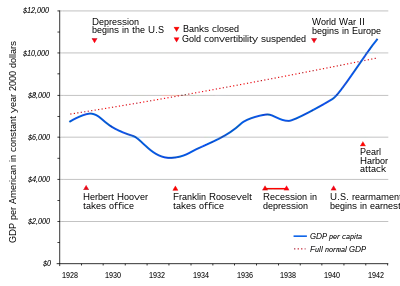

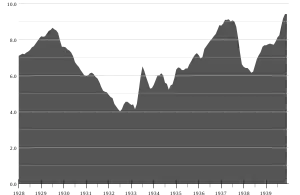

In most countries of the world, recovery from the Great Depression began in 1933.[11] In the U.S., recovery began in early 1933,[11] but the U.S. did not return to 1929 GNP for over a decade and still had an unemployment rate of about 15% in 1940, albeit down from the high of 25% in 1933.

There is no consensus among economists regarding the motive force for the U.S. economic expansion that continued through most of the Roosevelt years (and the 1937 recession that interrupted it). The common view among most economists is that Roosevelt's New Deal policies either caused or accelerated the recovery, although his policies were never aggressive enough to bring the economy completely out of recession. Some economists have also called attention to the positive effects from expectations of reflation and rising nominal interest rates that Roosevelt's words and actions portended.[47][48] It was the rollback of those same reflationary policies that led to the interruption of a recession beginning in late 1937.[49][50] One contributing policy that reversed reflation was the Banking Act of 1935, which effectively raised reserve requirements, causing a monetary contraction that helped to thwart the recovery.[51] GDP returned to its upward trend in 1938.[46] A revisionist view among some economists holds that the New Deal prolonged the Great Depression.[52] John Maynard Keynes did not think that the New Deal under Roosevelt ended the Great Depression: "It is, it seems, politically impossible for a capitalistic democracy to organize expenditure on the scale necessary to make the grand experiments which would prove my case—except in war conditions."[53]

According to Christina Romer, the money supply growth caused by huge international gold inflows was a crucial source of the recovery of the United States economy, and that the economy showed little sign of self-correction. The gold inflows were partly due to devaluation of the U.S. dollar and partly due to deterioration of the political situation in Europe.[54] In their book, A Monetary History of the United States, Milton Friedman and Anna J. Schwartz also attributed the recovery to monetary factors, and contended that it was much slowed by poor management of money by the Federal Reserve System. Former (2006–2014) Chairman of the Federal Reserve Ben Bernanke agreed that monetary factors played important roles both in the worldwide economic decline and eventual recovery.[55] Bernanke also saw a strong role for institutional factors, particularly the rebuilding and restructuring of the financial system,[56] and pointed out that the Depression should be examined in an international perspective.[57]

Role of women and household economics

Women's primary role was as housewives; without a steady flow of family income, their work became much harder in dealing with food and clothing and medical care. Birthrates fell everywhere, as children were postponed until families could financially support them. The average birthrate for 14 major countries fell 12% from 19.3 births per thousand population in 1930, to 17.0 in 1935.[58] In Canada, half of Roman Catholic women defied Church teachings and used contraception to postpone births.[59]

Among the few women in the labor force, layoffs were less common in the white-collar jobs and they were typically found in light manufacturing work. However, there was a widespread demand to limit families to one paid job, so that wives might lose employment if their husband was employed.[60][61][62] Across Britain, there was a tendency for married women to join the labor force, competing for part-time jobs especially.[63][64]

In France, very slow population growth, especially in comparison to Germany continued to be a serious issue in the 1930s. Support for increasing welfare programs during the depression included a focus on women in the family. The Conseil Supérieur de la Natalité campaigned for provisions enacted in the Code de la Famille (1939) that increased state assistance to families with children and required employers to protect the jobs of fathers, even if they were immigrants.[65]

In rural and small-town areas, women expanded their operation of vegetable gardens to include as much food production as possible. In the United States, agricultural organizations sponsored programs to teach housewives how to optimize their gardens and to raise poultry for meat and eggs.[66] Rural women made feed sack dresses and other items for themselves and their families and homes from feed sacks.[67] In American cities, African American women quiltmakers enlarged their activities, promoted collaboration, and trained neophytes. Quilts were created for practical use from various inexpensive materials and increased social interaction for women and promoted camaraderie and personal fulfillment.[68]

Oral history provides evidence for how housewives in a modern industrial city handled shortages of money and resources. Often they updated strategies their mothers used when they were growing up in poor families. Cheap foods were used, such as soups, beans and noodles. They purchased the cheapest cuts of meat—sometimes even horse meat—and recycled the Sunday roast into sandwiches and soups. They sewed and patched clothing, traded with their neighbors for outgrown items, and made do with colder homes. New furniture and appliances were postponed until better days. Many women also worked outside the home, or took boarders, did laundry for trade or cash, and did sewing for neighbors in exchange for something they could offer. Extended families used mutual aid—extra food, spare rooms, repair-work, cash loans—to help cousins and in-laws.[69]

In Japan, official government policy was deflationary and the opposite of Keynesian spending. Consequently, the government launched a campaign across the country to induce households to reduce their consumption, focusing attention on spending by housewives.[70]

In Germany, the government tried to reshape private household consumption under the Four-Year Plan of 1936 to achieve German economic self-sufficiency. The Nazi women's organizations, other propaganda agencies and the authorities all attempted to shape such consumption as economic self-sufficiency was needed to prepare for and to sustain the coming war. The organizations, propaganda agencies and authorities employed slogans that called up traditional values of thrift and healthy living. However, these efforts were only partly successful in changing the behavior of housewives.[71]

World War II and recovery

The common view among economic historians is that the Great Depression ended with the advent of World War II. Many economists believe that government spending on the war caused or at least accelerated recovery from the Great Depression, though some consider that it did not play a very large role in the recovery, though it did help in reducing unemployment.[11][72][73][74]

The rearmament policies leading up to World War II helped stimulate the economies of Europe in 1937–1939. By 1937, unemployment in Britain had fallen to 1.5 million. The mobilization of manpower following the outbreak of war in 1939 ended unemployment.[75]

When the United States entered the war in 1941, it finally eliminated the last effects from the Great Depression and brought the U.S. unemployment rate down below 10%.[76] In the U.S., massive war spending doubled economic growth rates, either masking the effects of the Depression or essentially ending the Depression. Businessmen ignored the mounting national debt and heavy new taxes, redoubling their efforts for greater output to take advantage of generous government contracts.[77]

Causes

The two classic competing economic theories of the Great Depression are the Keynesian (demand-driven) and the Monetarist explanation.[78] There are also various heterodox theories that downplay or reject the explanations of the Keynesians and monetarists. The consensus among demand-driven theories is that a large-scale loss of confidence led to a sudden reduction in consumption and investment spending. Once panic and deflation set in, many people believed they could avoid further losses by keeping clear of the markets. Holding money became profitable as prices dropped lower and a given amount of money bought ever more goods, exacerbating the drop in demand.[79] Monetarists believe that the Great Depression started as an ordinary recession, but the shrinking of the money supply greatly exacerbated the economic situation, causing a recession to descend into the Great Depression.[80]

Economists and economic historians are almost evenly split as to whether the traditional monetary explanation that monetary forces were the primary cause of the Great Depression is right, or the traditional Keynesian explanation that a fall in autonomous spending, particularly investment, is the primary explanation for the onset of the Great Depression.[81] Today there is also significant academic support for the debt deflation theory and the expectations hypothesis that — building on the monetary explanation of Milton Friedman and Anna Schwartz — add non-monetary explanations.[82][83]

There is a consensus that the Federal Reserve System should have cut short the process of monetary deflation and banking collapse, by expanding the money supply and acting as lender of last resort. If they had done this, the economic downturn would have been far less severe and much shorter.[84]

Mainstream explanations

Modern mainstream economists see the reasons in

- A money supply reduction (Monetarists) and therefore a banking crisis, reduction of credit, and bankruptcies.

- Insufficient demand from the private sector and insufficient fiscal spending (Keynesians).

- Passage of the Smoot–Hawley Tariff Act exacerbated what otherwise might have been a more "standard" recession (Both Monetarists and Keynesians).[30]

Insufficient spending, the money supply reduction, and debt on margin led to falling prices and further bankruptcies (Irving Fisher's debt deflation).

Monetarist view

The monetarist explanation was given by American economists Milton Friedman and Anna J. Schwartz.[85] They argued that the Great Depression was caused by the banking crisis that caused one-third of all banks to vanish, a reduction of bank shareholder wealth and more importantly monetary contraction of 35%, which they called "The Great Contraction". This caused a price drop of 33% (deflation).[86] By not lowering interest rates, by not increasing the monetary base and by not injecting liquidity into the banking system to prevent it from crumbling, the Federal Reserve passively watched the transformation of a normal recession into the Great Depression. Friedman and Schwartz argued that the downward turn in the economy, starting with the stock market crash, would merely have been an ordinary recession if the Federal Reserve had taken aggressive action.[87][88] This view was endorsed in 2002 by Federal Reserve Governor Ben Bernanke in a speech honoring Friedman and Schwartz with this statement:

Let me end my talk by abusing slightly my status as an official representative of the Federal Reserve. I would like to say to Milton and Anna: Regarding the Great Depression, you're right. We did it. We're very sorry. But thanks to you, we won't do it again.

The Federal Reserve allowed some large public bank failures – particularly that of the New York Bank of United States – which produced panic and widespread runs on local banks, and the Federal Reserve sat idly by while banks collapsed. Friedman and Schwartz argued that, if the Fed had provided emergency lending to these key banks, or simply bought government bonds on the open market to provide liquidity and increase the quantity of money after the key banks fell, all the rest of the banks would not have fallen after the large ones did, and the money supply would not have fallen as far and as fast as it did.[91]

With significantly less money to go around, businesses could not get new loans and could not even get their old loans renewed, forcing many to stop investing. This interpretation blames the Federal Reserve for inaction, especially the New York branch.[92]

One reason why the Federal Reserve did not act to limit the decline of the money supply was the gold standard. At that time, the amount of credit the Federal Reserve could issue was limited by the Federal Reserve Act, which required 40% gold backing of Federal Reserve Notes issued. By the late 1920s, the Federal Reserve had almost hit the limit of allowable credit that could be backed by the gold in its possession. This credit was in the form of Federal Reserve demand notes.[93] A "promise of gold" is not as good as "gold in the hand", particularly when they only had enough gold to cover 40% of the Federal Reserve Notes outstanding. During the bank panics, a portion of those demand notes was redeemed for Federal Reserve gold. Since the Federal Reserve had hit its limit on allowable credit, any reduction in gold in its vaults had to be accompanied by a greater reduction in credit. On April 5, 1933, President Roosevelt signed Executive Order 6102 making the private ownership of gold certificates, coins and bullion illegal, reducing the pressure on Federal Reserve gold.[93]

Keynesian view

British economist John Maynard Keynes argued in The General Theory of Employment, Interest and Money that lower aggregate expenditures in the economy contributed to a massive decline in income and to employment that was well below the average. In such a situation, the economy reached equilibrium at low levels of economic activity and high unemployment.

Keynes's basic idea was simple: to keep people fully employed, governments have to run deficits when the economy is slowing, as the private sector would not invest enough to keep production at the normal level and bring the economy out of recession. Keynesian economists called on governments during times of economic crisis to pick up the slack by increasing government spending or cutting taxes.

As the Depression wore on, Franklin D. Roosevelt tried public works, farm subsidies, and other devices to restart the U.S. economy, but never completely gave up trying to balance the budget. According to the Keynesians, this improved the economy, but Roosevelt never spent enough to bring the economy out of recession until the start of World War II.[94]

Debt deflation

Irving Fisher argued that the predominant factor leading to the Great Depression was a vicious circle of deflation and growing over-indebtedness.[95] He outlined nine factors interacting with one another under conditions of debt and deflation to create the mechanics of boom to bust. The chain of events proceeded as follows:

- Debt liquidation and distress selling

- Contraction of the money supply as bank loans are paid off

- A fall in the level of asset prices

- A still greater fall in the net worth of businesses, precipitating bankruptcies

- A fall in profits

- A reduction in output, in trade and in employment

- Pessimism and loss of confidence

- Hoarding of money

- A fall in nominal interest rates and a rise in deflation adjusted interest rates[95]

During the Crash of 1929 preceding the Great Depression, margin requirements were only 10%.[96] Brokerage firms, in other words, would lend $9 for every $1 an investor had deposited. When the market fell, brokers called in these loans, which could not be paid back.[97] Banks began to fail as debtors defaulted on debt and depositors attempted to withdraw their deposits en masse, triggering multiple bank runs. Government guarantees and Federal Reserve banking regulations to prevent such panics were ineffective or not used. Bank failures led to the loss of billions of dollars in assets.[97]

Outstanding debts became heavier, because prices and incomes fell by 20–50% but the debts remained at the same dollar amount. After the panic of 1929 and during the first 10 months of 1930, 744 U.S. banks failed. (In all, 9,000 banks failed during the 1930s.) By April 1933, around $7 billion in deposits had been frozen in failed banks or those left unlicensed after the March Bank Holiday.[98] Bank failures snowballed as desperate bankers called in loans that borrowers did not have time or money to repay. With future profits looking poor, capital investment and construction slowed or completely ceased. In the face of bad loans and worsening future prospects, the surviving banks became even more conservative in their lending.[97] Banks built up their capital reserves and made fewer loans, which intensified deflationary pressures. A vicious cycle developed and the downward spiral accelerated.

The liquidation of debt could not keep up with the fall of prices that it caused. The mass effect of the stampede to liquidate increased the value of each dollar owed, relative to the value of declining asset holdings. The very effort of individuals to lessen their burden of debt effectively increased it. Paradoxically, the more the debtors paid, the more they owed.[95] This self-aggravating process turned a 1930 recession into a 1933 great depression.

Fisher's debt-deflation theory initially lacked mainstream influence because of the counter-argument that debt-deflation represented no more than a redistribution from one group (debtors) to another (creditors). Pure re-distributions should have no significant macroeconomic effects.

Building on both the monetary hypothesis of Milton Friedman and Anna Schwartz and the debt deflation hypothesis of Irving Fisher, Ben Bernanke developed an alternative way in which the financial crisis affected output. He builds on Fisher's argument that dramatic declines in the price level and nominal incomes lead to increasing real debt burdens, which in turn leads to debtor insolvency and consequently lowers aggregate demand; a further price level decline would then result in a debt deflationary spiral. According to Bernanke, a small decline in the price level simply reallocates wealth from debtors to creditors without doing damage to the economy. But when the deflation is severe, falling asset prices along with debtor bankruptcies lead to a decline in the nominal value of assets on bank balance sheets. Banks will react by tightening their credit conditions, which in turn leads to a credit crunch that seriously harms the economy. A credit crunch lowers investment and consumption, which results in declining aggregate demand and additionally contributes to the deflationary spiral.[99][100][101]

Expectations hypothesis

Since economic mainstream turned to the new neoclassical synthesis, expectations are a central element of macroeconomic models. According to Peter Temin, Barry Wigmore, Gauti B. Eggertsson and Christina Romer, the key to recovery and to ending the Great Depression was brought about by a successful management of public expectations. The thesis is based on the observation that after years of deflation and a very severe recession important economic indicators turned positive in March 1933 when Franklin D. Roosevelt took office. Consumer prices turned from deflation to a mild inflation, industrial production bottomed out in March 1933, and investment doubled in 1933 with a turnaround in March 1933. There were no monetary forces to explain that turnaround. Money supply was still falling and short-term interest rates remained close to zero. Before March 1933, people expected further deflation and a recession so that even interest rates at zero did not stimulate investment. But when Roosevelt announced major regime changes, people began to expect inflation and an economic expansion. With these positive expectations, interest rates at zero began to stimulate investment just as they were expected to do. Roosevelt's fiscal and monetary policy regime change helped make his policy objectives credible. The expectation of higher future income and higher future inflation stimulated demand and investment. The analysis suggests that the elimination of the policy dogmas of the gold standard, a balanced budget in times of crisis and small government led endogenously to a large shift in expectation that accounts for about 70–80% of the recovery of output and prices from 1933 to 1937. If the regime change had not happened and the Hoover policy had continued, the economy would have continued its free fall in 1933, and output would have been 30% lower in 1937 than in 1933.[102][103][104]

The recession of 1937–1938, which slowed down economic recovery from the Great Depression, is explained by fears of the population that the moderate tightening of the monetary and fiscal policy in 1937 were first steps to a restoration of the pre-1933 policy regime.[105]

Common position

There is common consensus among economists today that the government and the central bank should work to keep the interconnected macroeconomic aggregates of gross domestic product and money supply on a stable growth path. When threatened by expectations of a depression, central banks should expand liquidity in the banking system and the government should cut taxes and accelerate spending in order to prevent a collapse in money supply and aggregate demand.[106]

At the beginning of the Great Depression, most economists believed in Say's law and the equilibrating powers of the market, and failed to understand the severity of the Depression. Outright leave-it-alone liquidationism was a common position, and was universally held by Austrian School economists.[107] The liquidationist position held that a depression worked to liquidate failed businesses and investments that had been made obsolete by technological development – releasing factors of production (capital and labor) to be redeployed in other more productive sectors of the dynamic economy. They argued that even if self-adjustment of the economy caused mass bankruptcies, it was still the best course.[107]

Economists like Barry Eichengreen and J. Bradford DeLong note that President Herbert Hoover tried to keep the federal budget balanced until 1932, when he lost confidence in his Secretary of the Treasury Andrew Mellon and replaced him.[107][108][109] An increasingly common view among economic historians is that the adherence of many Federal Reserve policymakers to the liquidationist position led to disastrous consequences.[108] Unlike what liquidationists expected, a large proportion of the capital stock was not redeployed but vanished during the first years of the Great Depression. According to a study by Olivier Blanchard and Lawrence Summers, the recession caused a drop of net capital accumulation to pre-1924 levels by 1933.[110] Milton Friedman called leave-it-alone liquidationism "dangerous nonsense".[106] He wrote:

I think the Austrian business-cycle theory has done the world a great deal of harm. If you go back to the 1930s, which is a key point, here you had the Austrians sitting in London, Hayek and Lionel Robbins, and saying you just have to let the bottom drop out of the world. You've just got to let it cure itself. You can't do anything about it. You will only make it worse. ... I think by encouraging that kind of do-nothing policy both in Britain and in the United States, they did harm.[108]

Austrian School

Two prominent theorists in the Austrian School on the Great Depression include Austrian economist Friedrich Hayek and American economist Murray Rothbard, who wrote America's Great Depression (1963). In their view, much like the monetarists, the Federal Reserve (created in 1913) shoulders much of the blame; however, unlike the Monetarists, they argue that the key cause of the Depression was the expansion of the money supply in the 1920s which led to an unsustainable credit-driven boom.[111]

In the Austrian view, it was this inflation of the money supply that led to an unsustainable boom in both asset prices (stocks and bonds) and capital goods. Therefore, by the time the Federal Reserve tightened in 1928 it was far too late to prevent an economic contraction.[111] In February 1929 Hayek published a paper predicting the Federal Reserve's actions would lead to a crisis starting in the stock and credit markets.[112]

According to Rothbard, the government support for failed enterprises and efforts to keep wages above their market values actually prolonged the Depression.[113] Unlike Rothbard, after 1970 Hayek believed that the Federal Reserve had further contributed to the problems of the Depression by permitting the money supply to shrink during the earliest years of the Depression.[114] However, during the Depression (in 1932[115] and in 1934)[115] Hayek had criticized both the Federal Reserve and the Bank of England for not taking a more contractionary stance.[115]

Hans Sennholz argued that most boom and busts that plagued the American economy, such as those in 1819–20, 1839–1843, 1857–1860, 1873–1878, 1893–1897, and 1920–21, were generated by government creating a boom through easy money and credit, which was soon followed by the inevitable bust.[116]

Ludwig von Mises wrote in the 1930s: "Credit expansion cannot increase the supply of real goods. It merely brings about a rearrangement. It diverts capital investment away from the course prescribed by the state of economic wealth and market conditions. It causes production to pursue paths which it would not follow unless the economy were to acquire an increase in material goods. As a result, the upswing lacks a solid base. It is not real prosperity. It is illusory prosperity. It did not develop from an increase in economic wealth, i.e. the accumulation of savings made available for productive investment. Rather, it arose because the credit expansion created the illusion of such an increase. Sooner or later, it must become apparent that this economic situation is built on sand."[117][118]

Marxist

Marxists generally argue that the Great Depression was the result of the inherent instability of the capitalist mode of production.[119] According to Forbes, "The idea that capitalism caused the Great Depression was widely held among intellectuals and the general public for many decades."[120]

Inequality

Two economists of the 1920s, Waddill Catchings and William Trufant Foster, popularized a theory that influenced many policy makers, including Herbert Hoover, Henry A. Wallace, Paul Douglas, and Marriner Eccles. It held the economy produced more than it consumed, because the consumers did not have enough income. Thus the unequal distribution of wealth throughout the 1920s caused the Great Depression.[121][122]

According to this view, the root cause of the Great Depression was a global over-investment in heavy industry capacity compared to wages and earnings from independent businesses, such as farms. The proposed solution was for the government to pump money into the consumers' pockets. That is, it must redistribute purchasing power, maintaining the industrial base, and re-inflating prices and wages to force as much of the inflationary increase in purchasing power into consumer spending. The economy was overbuilt, and new factories were not needed. Foster and Catchings recommended[123] federal and state governments to start large construction projects, a program followed by Hoover and Roosevelt.

Productivity shock

It cannot be emphasized too strongly that the [productivity, output, and employment] trends we are describing are long-time trends and were thoroughly evident before 1929. These trends are in nowise the result of the present depression, nor are they the result of the World War. On the contrary, the present depression is a collapse resulting from these long-term trends.

— M. King Hubbert[124]

The first three decades of the 20th century saw economic output surge with electrification, mass production, and motorized farm machinery, and because of the rapid growth in productivity there was a lot of excess production capacity and the work week was being reduced. The dramatic rise in productivity of major industries in the U.S. and the effects of productivity on output, wages and the workweek are discussed by Spurgeon Bell in his book Productivity, Wages, and National Income (1940).[125]

Socio-economic effects

The majority of countries set up relief programs and most underwent some sort of political upheaval, pushing them to the right. Many of the countries in Europe and Latin America that were democracies saw them overthrown by some form of dictatorship or authoritarian rule, most famously in Germany in 1933. The Dominion of Newfoundland gave up democracy voluntarily.

Australia

Australia's dependence on agricultural and industrial exports meant it was one of the hardest-hit developed countries.[126] Falling export demand and commodity prices placed massive downward pressures on wages. Unemployment reached a record high of 29% in 1932,[127] with incidents of civil unrest becoming common.[128] After 1932, an increase in wool and meat prices led to a gradual recovery.[129]

Canada

Harshly affected by both the global economic downturn and the Dust Bowl, Canadian industrial production had by 1932 fallen to only 58% of its 1929 figure, the second-lowest level in the world after the United States, and well behind countries such as Britain, which fell to only 83% of the 1929 level. Total national income fell to 56% of the 1929 level, again worse than any country apart from the United States. Unemployment reached 27% at the depth of the Depression in 1933.[130]

Chile

The League of Nations labeled Chile the country hardest hit by the Great Depression because 80% of government revenue came from exports of copper and nitrates, which were in low demand. Chile initially felt the impact of the Great Depression in 1930, when GDP dropped 14%, mining income declined 27%, and export earnings fell 28%. By 1932, GDP had shrunk to less than half of what it had been in 1929, exacting a terrible toll in unemployment and business failures.

Influenced profoundly by the Great Depression, many government leaders promoted the development of local industry in an effort to insulate the economy from future external shocks. After six years of government austerity measures, which succeeded in reestablishing Chile's creditworthiness, Chileans elected to office during the 1938–58 period a succession of center and left-of-center governments interested in promoting economic growth through government intervention.

Prompted in part by the devastating 1939 Chillán earthquake, the Popular Front government of Pedro Aguirre Cerda created the Production Development Corporation (Corporación de Fomento de la Producción, CORFO) to encourage with subsidies and direct investments an ambitious program of import substitution industrialization. Consequently, as in other Latin American countries, protectionism became an entrenched aspect of the Chilean economy.

China

China was largely unaffected by the Depression, mainly by having stuck to the Silver standard. However, the U.S. silver purchase act of 1934 created an intolerable demand on China's silver coins, and so, in the end, the silver standard was officially abandoned in 1935 in favor of the four Chinese national banks' "legal note" issues. China and the British colony of Hong Kong, which followed suit in this regard in September 1935, would be the last to abandon the silver standard. In addition, the Nationalist Government also acted energetically to modernize the legal and penal systems, stabilize prices, amortize debts, reform the banking and currency systems, build railroads and highways, improve public health facilities, legislate against traffic in narcotics and augment industrial and agricultural production. On November 3, 1935, the government instituted the fiat currency (fapi) reform, immediately stabilizing prices and also raising revenues for the government.

European African colonies

The sharp fall in commodity prices, and the steep decline in exports, hurt the economies of the European colonies in Africa and Asia.[131][132] The agricultural sector was especially hard hit. For example, sisal had recently become a major export crop in Kenya and Tanganyika. During the depression, it suffered severely from low prices and marketing problems that affected all colonial commodities in Africa. Sisal producers established centralized controls for the export of their fibre.[133] There was widespread unemployment and hardship among peasants, labourers, colonial auxiliaries, and artisans.[134] The budgets of colonial governments were cut, which forced the reduction in ongoing infrastructure projects, such as the building and upgrading of roads, ports and communications.[135] The budget cuts delayed the schedule for creating systems of higher education.[136]

The depression severely hurt the export-based Belgian Congo economy because of the drop in international demand for raw materials and for agricultural products. For example, the price of peanuts fell from 125 to 25 centimes. In some areas, as in the Katanga mining region, employment declined by 70%. In the country as a whole, the wage labour force decreased by 72.000 and many men returned to their villages. In Leopoldville, the population decreased by 33%, because of this labour migration.[137]

Political protests were not common. However, there was a growing demand that the paternalistic claims be honored by colonial governments to respond vigorously. The theme was that economic reforms were more urgently needed than political reforms.[138] French West Africa launched an extensive program of educational reform in which "rural schools" designed to modernize agriculture would stem the flow of under-employed farm workers to cites where unemployment was high. Students were trained in traditional arts, crafts, and farming techniques and were then expected to return to their own villages and towns.[139]

France

The crisis affected France a bit later than other countries, hitting hard around 1931.[140] While the 1920s grew at the very strong rate of 4.43% per year, the 1930s rate fell to only 0.63%.[141]

The depression was relatively mild: unemployment peaked under 5%, the fall in production was at most 20% below the 1929 output; there was no banking crisis.[142]

However, the depression had drastic effects on the local economy, and partly explains the February 6, 1934 riots and even more the formation of the Popular Front, led by SFIO socialist leader Léon Blum, which won the elections in 1936. Ultra-nationalist groups also saw increased popularity, although democracy prevailed into World War II.

France's relatively high degree of self-sufficiency meant the damage was considerably less than in neighbouring states like Germany.

Germany

The Great Depression hit Germany hard. The impact of the Wall Street Crash forced American banks to end the new loans that had been funding the repayments under the Dawes Plan and the Young Plan. The financial crisis escalated out of control in mid-1931, starting with the collapse of the Credit Anstalt in Vienna in May.[40] This put heavy pressure on Germany, which was already in political turmoil with the rise in violence of national socialist and communist movements, as well as with investor nervousness at harsh government financial policies,[41] investors withdrew their short-term money from Germany as confidence spiraled downward. The Reichsbank lost 150 million marks in the first week of June, 540 million in the second, and 150 million in two days, June 19–20. Collapse was at hand. U.S. President Herbert Hoover called for a moratorium on payment of war reparations. This angered Paris, which depended on a steady flow of German payments, but it slowed the crisis down, and the moratorium was agreed to in July 1931. An international conference in London later in July produced no agreements but on August 19 a standstill agreement froze Germany's foreign liabilities for six months. Germany received emergency funding from private banks in New York as well as the Bank of International Settlements and the Bank of England. The funding only slowed the process. Industrial failures began in Germany, a major bank closed in July and a two-day holiday for all German banks was declared. Business failures became more frequent in July, and spread to Romania and Hungary.[42]

In 1932, 90% of German reparation payments were cancelled (in the 1950s, Germany repaid all its missed reparations debts). Widespread unemployment reached 25% as every sector was hurt. The government did not increase government spending to deal with Germany's growing crisis, as they were afraid that a high-spending policy could lead to a return of the hyperinflation that had affected Germany in 1923. Germany's Weimar Republic was hit hard by the depression, as American loans to help rebuild the German economy now stopped.[143] The unemployment rate reached nearly 30% in 1932.[144]

The German political landscape was dramatically altered, leading to Adolf Hitler's rise to power. The Nazi Party rose from being peripheral to winning 18.3% of the vote in the September 1930 election and the Communist Party also made gains, while moderate forces like the Social Democratic Party, the Democratic Party and the People's Party lost seats. The next two years were marked by increased street violence between Nazis and Communists, while governments under President Paul von Hindenburg increasingly relied on rule by decree, bypassing the Reichstag.[145] Hitler ran for the Presidency in 1932, and while he lost to the incumbent Hindenburg in the election, it marked a point during which both Nazi Party and the Communist parties rose in the years following the crash to altogether possess a Reichstag majority following the general election in July 1932.[144][146] Although the Nazis lost seats in November 1932 election, they remained the largest party, and Hitler was appointed as Chancellor the following January. The government formation deal was designed to give Hitler's conservative coalition partners many checks on his power, but over the next few months, the Nazis manoeuvred to consolidate a single-party dictatorship.[147]

Hitler followed an autarky economic policy, creating a network of client states and economic allies in central Europe and Latin America. By cutting wages and taking control of labor unions, plus public works spending, unemployment fell significantly by 1935. Large-scale military spending played a major role in the recovery.[148] The policies had the effect of driving up the cost of food imports and depleting foreign currency reserves, leaving to economic impasse by 1936. Nazi Germany faced a choice of either reversing course or pressing ahead with rearmament and autarky. Hitler chose the latter route, which according to Ian Kershaw "could only be partially accomplished without territorial expansion" and therefore war.[149][150]

Greece

The reverberations of the Great Depression hit Greece in 1932. The Bank of Greece tried to adopt deflationary policies to stave off the crises that were going on in other countries, but these largely failed. For a brief period, the drachma was pegged to the U.S. dollar, but this was unsustainable given the country's large trade deficit and the only long-term effects of this were Greece's foreign exchange reserves being almost totally wiped out in 1932. Remittances from abroad declined sharply and the value of the drachma began to plummet from 77 drachmas to the dollar in March 1931 to 111 drachmas to the dollar in April 1931. This was especially harmful to Greece as the country relied on imports from the UK, France, and the Middle East for many necessities. Greece went off the gold standard in April 1932 and declared a moratorium on all interest payments. The country also adopted protectionist policies such as import quotas, which several European countries did during the period.

Protectionist policies coupled with a weak drachma, stifling imports, allowed the Greek industry to expand during the Great Depression. In 1939, the Greek industrial output was 179% that of 1928. These industries were for the most part "built on sand" as one report of the Bank of Greece put it, as without massive protection they would not have been able to survive. Despite the global depression, Greece managed to suffer comparatively little, averaging an average growth rate of 3.5% from 1932 to 1939. The dictatorial regime of Ioannis Metaxas took over the Greek government in 1936, and economic growth was strong in the years leading up to the Second World War.

Iceland

Icelandic post-World War I prosperity came to an end with the outbreak of the Great Depression. The Depression hit Iceland hard as the value of exports plummeted. The total value of Icelandic exports fell from 74 million kronur in 1929 to 48 million in 1932, and was not to rise again to the pre-1930 level until after 1939.[151] Government interference in the economy increased: "Imports were regulated, trade with foreign currency was monopolized by state-owned banks, and loan capital was largely distributed by state-regulated funds".[151] Due to the outbreak of the Spanish Civil War, which cut Iceland's exports of saltfish by half, the Depression lasted in Iceland until the outbreak of World War II (when prices for fish exports soared).[151]

India

How much India was affected has been hotly debated. Historians have argued that the Great Depression slowed long-term industrial development.[152] Apart from two sectors—jute and coal—the economy was little affected. However, there were major negative impacts on the jute industry, as world demand fell and prices plunged.[153] Otherwise, conditions were fairly stable. Local markets in agriculture and small-scale industry showed modest gains.[154]

Ireland

Frank Barry and Mary E. Daly have argued that:

- Ireland was a largely agrarian economy, trading almost exclusively with the UK, at the time of the Great Depression. Beef and dairy products comprised the bulk of exports, and Ireland fared well relative to many other commodity producers, particularly in the early years of the depression.[155][156][157][158]

Italy

The Great Depression hit Italy very hard.[159] As industries came close to failure they were bought out by the banks in a largely illusionary bail-out—the assets used to fund the purchases were largely worthless. This led to a financial crisis peaking in 1932 and major government intervention. The Industrial Reconstruction Institute (IRI) was formed in January 1933 and took control of the bank-owned companies, suddenly giving Italy the largest state-owned industrial sector in Europe (excluding the USSR). IRI did rather well with its new responsibilities—restructuring, modernising and rationalising as much as it could. It was a significant factor in post-1945 development. But it took the Italian economy until 1935 to recover the manufacturing levels of 1930—a position that was only 60% better than that of 1913.[160][161]

Japan

The Great Depression did not strongly affect Japan. The Japanese economy shrank by 8% during 1929–31. Japan's Finance Minister Takahashi Korekiyo was the first to implement what have come to be identified as Keynesian economic policies: first, by large fiscal stimulus involving deficit spending; and second, by devaluing the currency. Takahashi used the Bank of Japan to sterilize the deficit spending and minimize resulting inflationary pressures. Econometric studies have identified the fiscal stimulus as especially effective.[162]

The devaluation of the currency had an immediate effect. Japanese textiles began to displace British textiles in export markets. The deficit spending proved to be most profound and went into the purchase of munitions for the armed forces. By 1933, Japan was already out of the depression. By 1934, Takahashi realized that the economy was in danger of overheating, and to avoid inflation, moved to reduce the deficit spending that went towards armaments and munitions.

This resulted in a strong and swift negative reaction from nationalists, especially those in the army, culminating in his assassination in the course of the February 26 Incident. This had a chilling effect on all civilian bureaucrats in the Japanese government. From 1934, the military's dominance of the government continued to grow. Instead of reducing deficit spending, the government introduced price controls and rationing schemes that reduced, but did not eliminate inflation, which remained a problem until the end of World War II.

The deficit spending had a transformative effect on Japan. Japan's industrial production doubled during the 1930s. Further, in 1929 the list of the largest firms in Japan was dominated by light industries, especially textile companies (many of Japan's automakers, such as Toyota, have their roots in the textile industry). By 1940 light industry had been displaced by heavy industry as the largest firms inside the Japanese economy.[163]

Latin America

Because of high levels of U.S. investment in Latin American economies, they were severely damaged by the Depression. Within the region, Chile, Bolivia and Peru were particularly badly affected.[164]

Before the 1929 crisis, links between the world economy and Latin American economies had been established through American and British investment in Latin American exports to the world. As a result, Latin Americans export industries felt the depression quickly. World prices for commodities such as wheat, coffee and copper plunged. Exports from all of Latin America to the U.S. fell in value from $1.2 billion in 1929 to $335 million in 1933, rising to $660 million in 1940.

But on the other hand, the depression led the area governments to develop new local industries and expand consumption and production. Following the example of the New Deal, governments in the area approved regulations and created or improved welfare institutions that helped millions of new industrial workers to achieve a better standard of living.

Middle East and North Africa

The Great Depression had severe impacts across the Middle East and North Africa, including economic decline which led to social unrest.[165]

Netherlands

From roughly 1931 to 1937, the Netherlands suffered a deep and exceptionally long depression. This depression was partly caused by the after-effects of the American stock-market crash of 1929, and partly by internal factors in the Netherlands. Government policy, especially the very late dropping of the Gold Standard, played a role in prolonging the depression. The Great Depression in the Netherlands led to some political instability and riots, and can be linked to the rise of the Dutch fascist political party NSB. The depression in the Netherlands eased off somewhat at the end of 1936, when the government finally dropped the Gold Standard, but real economic stability did not return until after World War II.[166]

New Zealand

New Zealand was especially vulnerable to worldwide depression, as it relied almost entirely on agricultural exports to the United Kingdom for its economy. The drop in exports led to a lack of disposable income from the farmers, who were the mainstay of the local economy. Jobs disappeared and wages plummeted, leaving people desperate and charities unable to cope. Work relief schemes were the only government support available to the unemployed, the rate of which by the early 1930s was officially around 15%, but unofficially nearly twice that level (official figures excluded Māori and women). In 1932, riots occurred among the unemployed in three of the country's main cities (Auckland, Dunedin, and Wellington). Many were arrested or injured through the tough official handling of these riots by police and volunteer "special constables".[167]

Poland

Poland was affected by the Great Depression longer and stronger than other countries due to inadequate economic response of the government and the pre-existing economic circumstances of the country. At that time, Poland was under the authoritarian rule of Sanacja, whose leader, Józef Piłsudski, was opposed to leaving the gold standard until his death in 1935. As a result, Poland was unable to perform a more active monetary and budget policy. Additionally, Poland was a relatively young country that emerged merely 10 years earlier after being partitioned between German, Russian and the Austro-Hungarian Empires for over a century. Prior to independence, the Russian part exported 91% of its exports to Russia proper, while the German part exported 68% to Germany proper. After independence, these markets were largely lost, as Russia transformed into USSR that was mostly a closed economy, and Germany was in a tariff war with Poland throughout the 1920s.[168]

Industrial production fell significantly: in 1932 hard coal production was down 27% compared to 1928, steel production was down 61%, and iron ore production noted a 89% decrease.[169] On the other hand, electrotechnical, leather, and paper industries noted marginal increases in production output. Overall, industrial production decreased by 41%.[170] A distinct feature of the Great Depression in Poland was the de-concentration of industry, as larger conglomerates were less flexible and paid their workers more than smaller ones.

Unemployment rate rose significantly (up to 43%) while nominal wages fell by 51% in 1933 and 56% in 1934, relative to 1928. However, real wages fell less due to the government's policy of decreasing cost of living, particularly food expenditures (food prices were down by 65% in 1935 compared to 1928 price levels). Material conditions deprivation led to strikes, some of them violent or violently pacified - like in Sanok (March of the Hungry in Sanok March 6, 1930), Lesko county (Lesko uprising June 21 – July 9, 1932) and Zawiercie (Bloody Friday (1930) April 18, 1930).

To adopt to the crisis, Polish government employed deflation methods such as high interest rates, credit limits and budget austerity to keep a fixed exchange rate with currencies tied to the gold standard. Only in late 1932 the government created a plan to fight the economic crisis.[171] Part of the plan was mass public works scheme, employing up to 100,000 people in 1935.[169] After Piłsudski's death, in 1936 the gold standard regime was relaxed, and launching the development of the Central Industrial Region kicked off the economy, to over 10% annual growth rate in the 1936-1938 period.

Portugal

Already under the rule of a dictatorial junta, the Ditadura Nacional, Portugal suffered no turbulent political effects of the Depression, although António de Oliveira Salazar, already appointed Minister of Finance in 1928 greatly expanded his powers and in 1932 rose to Prime Minister of Portugal to found the Estado Novo, an authoritarian corporatist dictatorship. With the budget balanced in 1929, the effects of the depression were relaxed through harsh measures towards budget balance and autarky, causing social discontent but stability and, eventually, an impressive economic growth.[172]

Puerto Rico

In the years immediately preceding the depression, negative developments in the island and world economies perpetuated an unsustainable cycle of subsistence for many Puerto Rican workers. The 1920s brought a dramatic drop in Puerto Rico's two primary exports, raw sugar and coffee, due to a devastating hurricane in 1928 and the plummeting demand from global markets in the latter half of the decade. 1930 unemployment on the island was roughly 36% and by 1933 Puerto Rico's per capita income dropped 30% (by comparison, unemployment in the United States in 1930 was approximately 8% reaching a height of 25% in 1933).[173][174] To provide relief and economic reform, the United States government and Puerto Rican politicians such as Carlos Chardon and Luis Muñoz Marín created and administered first the Puerto Rico Emergency Relief Administration (PRERA) 1933 and then in 1935, the Puerto Rico Reconstruction Administration (PRRA).[175]

South Africa

As world trade slumped, demand for South African agricultural and mineral exports fell drastically. The Carnegie Commission on Poor Whites had concluded in 1931 that nearly one-third of Afrikaners lived as paupers. The social discomfort caused by the depression was a contributing factor in the 1933 split between the "gesuiwerde" (purified) and "smelter" (fusionist) factions within the National Party and the National Party's subsequent fusion with the South African Party.[178][179] Unemployment programs were begun that focused primarily on the white population.[180]

Soviet Union

The Soviet Union was the world's only socialist state with very little international trade. Its economy was not tied to the rest of the world and was mostly unaffected by the Great Depression.[181]

At the time of the Depression, the Soviet economy was growing steadily, fuelled by intensive investment in heavy industry. The apparent economic success of the Soviet Union at a time when the capitalist world was in crisis led many Western intellectuals to view the Soviet system favorably. Jennifer Burns wrote:

As the Great Depression ground on and unemployment soared, intellectuals began unfavorably comparing their faltering capitalist economy to Russian Communism [...] More than ten years after the Revolution, Communism was finally reaching full flower, according to New York Times reporter Walter Duranty, a Stalin fan who vigorously debunked accounts of the Ukraine famine, a man-made disaster that would leave millions dead.[182]

Due to having very little international trade and its policy of isolation, they did not receive the benefits of international trade once the depression ran its course, and were still effectively poorer than most developed countries at their worst sufferings in the crisis.

The Great Depression caused mass immigration to the Soviet Union, mostly from Finland and Germany. Soviet Russia was at first happy to help these immigrants settle, because they believed they were victims of capitalism who had come to help the Soviet cause. However, when the Soviet Union entered the war in 1941, most of these Germans and Finns were arrested and sent to Siberia, while their Russian-born children were placed in orphanages. Their fate remains unknown.[183]

Spain

Spain had a relatively isolated economy, with high protective tariffs and was not one of the main countries affected by the Depression. The banking system held up well, as did agriculture.[184]

By far the most serious negative impact came after 1936 from the heavy destruction of infrastructure and manpower by the civil war, 1936–39. Many talented workers were forced into permanent exile. By staying neutral in the Second World War, and selling to both sides, the economy avoided further disasters.[185]

Sweden

By the 1930s, Sweden had what America's Life magazine called in 1938 the "world's highest standard of living". Sweden was also the first country worldwide to recover completely from the Great Depression. Taking place amid a short-lived government and a less-than-a-decade old Swedish democracy, events such as those surrounding Ivar Kreuger (who eventually committed suicide) remain infamous in Swedish history. The Social Democrats under Per Albin Hansson formed their first long-lived government in 1932 based on strong interventionist and welfare state policies, monopolizing the office of Prime Minister until 1976 with the sole and short-lived exception of Axel Pehrsson-Bramstorp's "summer cabinet" in 1936. During forty years of hegemony, it was the most successful political party in the history of Western liberal democracy.[186]

Thailand

In Thailand, then known as the Kingdom of Siam, the Great Depression contributed to the end of the absolute monarchy of King Rama VII in the Siamese revolution of 1932.

United Kingdom

The World Depression broke at a time when the United Kingdom had still not fully recovered from the effects of the First World War more than a decade earlier. The country was driven off the gold standard in 1931.

The world financial crisis began to overwhelm Britain in 1931; investors around the world started withdrawing their gold from London at the rate of £2.5 million per day.[43] Credits of £25 million each from the Bank of France and the Federal Reserve Bank of New York and an issue of £15 million fiduciary note slowed, but did not reverse the British crisis. The financial crisis now caused a major political crisis in Britain in August 1931. With deficits mounting, the bankers demanded a balanced budget; the divided cabinet of Prime Minister Ramsay MacDonald's Labour government agreed; it proposed to raise taxes, cut spending and most controversially, to cut unemployment benefits by 20%. The attack on welfare was totally unacceptable to the Labour movement. MacDonald wanted to resign, but King George V insisted he remain and form an all-party coalition "National Government". The Conservative and Liberals parties signed on, along with a small cadre of Labour, but the vast majority of Labour leaders denounced MacDonald as a traitor for leading the new government. Britain went off the gold standard, and suffered relatively less than other major countries in the Great Depression. In the 1931 British election, the Labour Party was virtually destroyed, leaving MacDonald as Prime Minister for a largely Conservative coalition.[187][45]

The effects on the northern industrial areas of Britain were immediate and devastating, as demand for traditional industrial products collapsed. By the end of 1930 unemployment had more than doubled from 1 million to 2.5 million (20% of the insured workforce), and exports had fallen in value by 50%. In 1933, 30% of Glaswegians were unemployed due to the severe decline in heavy industry. In some towns and cities in the north east, unemployment reached as high as 70% as shipbuilding fell by 90%.[188] The National Hunger March of September–October 1932 was the largest[189] of a series of hunger marches in Britain in the 1920s and 1930s. About 200,000 unemployed men were sent to the work camps, which continued in operation until 1939.[190]

In the less industrial Midlands and Southern England, the effects were short-lived and the later 1930s were a prosperous time. Growth in modern manufacture of electrical goods and a boom in the motor car industry was helped by a growing southern population and an expanding middle class. Agriculture also saw a boom during this period.[191]

United States

Hoover's first measures to combat the depression were based on encouraging businesses not to reduce their workforce or cut wages but businesses had little choice: wages were reduced, workers were laid off, and investments postponed.[192][193]

In June 1930, Congress approved the Smoot–Hawley Tariff Act which raised tariffs on thousands of imported items. The intent of the Act was to encourage the purchase of American-made products by increasing the cost of imported goods, while raising revenue for the federal government and protecting farmers. Most countries that traded with the U.S. increased tariffs on American-made goods in retaliation, reducing international trade, and worsening the Depression.[194]

In 1931, Hoover urged bankers to set up the National Credit Corporation[195] so that big banks could help failing banks survive. But bankers were reluctant to invest in failing banks, and the National Credit Corporation did almost nothing to address the problem.[196]

By 1932, unemployment had reached 23.6%, peaking in early 1933 at 25%.[198] Those releasing from prison during this period had an especially difficult time finding employment given the stigma of their criminal records, which often led to recidivism out of economic desperation.[199] Drought persisted in the agricultural heartland, businesses and families defaulted on record numbers of loans, and more than 5,000 banks had failed.[200] Hundreds of thousands of Americans found themselves homeless, and began congregating in shanty towns – dubbed "Hoovervilles" – that began to appear across the country.[201] In response, President Hoover and Congress approved the Federal Home Loan Bank Act, to spur new home construction, and reduce foreclosures. The final attempt of the Hoover Administration to stimulate the economy was the passage of the Emergency Relief and Construction Act (ERA) which included funds for public works programs such as dams and the creation of the Reconstruction Finance Corporation (RFC) in 1932. The Reconstruction Finance Corporation was a Federal agency with the authority to lend up to $2 billion to rescue banks and restore confidence in financial institutions. But $2 billion was not enough to save all the banks, and bank runs and bank failures continued.[192] Quarter by quarter the economy went downhill, as prices, profits and employment fell, leading to the political realignment in 1932 that brought to power Franklin Delano Roosevelt. It is important to note, however, that after volunteerism failed, Hoover developed ideas that laid the framework for parts of the New Deal.

Shortly after President Franklin Delano Roosevelt was inaugurated in 1933, drought and erosion combined to cause the Dust Bowl, shifting hundreds of thousands of displaced persons off their farms in the Midwest. From his inauguration onward, Roosevelt argued that restructuring of the economy would be needed to prevent another depression or avoid prolonging the current one. New Deal programs sought to stimulate demand and provide work and relief for the impoverished through increased government spending and the institution of financial reforms.

During a "bank holiday" that lasted five days, the Emergency Banking Act was signed into law. It provided for a system of reopening sound banks under Treasury supervision, with federal loans available if needed. The Securities Act of 1933 comprehensively regulated the securities industry. This was followed by the Securities Exchange Act of 1934 which created the Securities and Exchange Commission. Although amended, key provisions of both Acts are still in force. Federal insurance of bank deposits was provided by the FDIC, and the Glass–Steagall Act.

The Agricultural Adjustment Act provided incentives to cut farm production in order to raise farming prices. The National Recovery Administration (NRA) made a number of sweeping changes to the American economy. It forced businesses to work with government to set price codes through the NRA to fight deflationary "cut-throat competition" by the setting of minimum prices and wages, labor standards, and competitive conditions in all industries. It encouraged unions that would raise wages, to increase the purchasing power of the working class. The NRA was deemed unconstitutional by the Supreme Court of the United States in 1935.

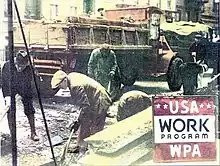

These reforms, together with several other relief and recovery measures, are called the First New Deal. Economic stimulus was attempted through a new alphabet soup of agencies set up in 1933 and 1934 and previously extant agencies such as the Reconstruction Finance Corporation. By 1935, the "Second New Deal" added Social Security (which was later considerably extended through the Fair Deal), a jobs program for the unemployed (the Works Progress Administration, WPA) and, through the National Labor Relations Board, a strong stimulus to the growth of labor unions. In 1929, federal expenditures constituted only 3% of the GDP. The national debt as a proportion of GNP rose under Hoover from 20% to 40%. Roosevelt kept it at 40% until the war began, when it soared to 128%.