This article was co-authored by Darron Kendrick, CPA, MA. Darron Kendrick is an Adjunct Professor of Accounting and Law at the University of North Georgia. He received his Masters degree in tax law from the Thomas Jefferson School of Law in 2012, and his CPA from the Alabama State Board of Public Accountancy in 1984.

This article has been viewed 195,971 times.

A subsidiary is a company that is controlled by another company that owns 50% or more of its voting stock. The controlling company, also called the parent company, is said to have a controlling interest in the subsidiary.[1] This type of parent-subsidiary relationship typically comes about as the result of acquisitions or heavy investment by a large corporation in another company. Parent companies will need to account for transactions with the subsidiary as well as prepare consolidated financial statements.

Steps

Accounting for Transactions with the Subsidiary

-

1Record the parent’s purchase of the subsidiary’s stock. To do this, debit Intercorporate Investment and credit Cash.

- For example, if the parent bought $50,000 worth of a subsidiary’s stock, it would debit Intercorporate Investment for $50,000 to reflect the new asset and credit cash for $50,000 to reflect the cash outflow.

-

2Record any dividends that the subsidiary pays the parent company. To do this, debit Cash and credit Intercorporate Investment.

- For example, say that the parent company receives $1,000 of dividends from the subsidiary. The parent company debits cash for $1,000 and credits Intercorporate Investment for $1,000 to reflect the fact that the dividend decreased the subsidiary’s retained earnings.

Advertisement -

3Record the parent’s percentage of the subsidiary’s annual profit. To do this, debit the Intercorporate Investment account and credit Investment Revenue.

- For example, assume the parent company owns 60% of the subsidiary, and the subsidiary reports a profit of $100,000. The parent company debits Intercorporate Investment for $60,000 (60% of $100,000) and credits Investment Revenue for $60,000.[2]

-

4Identify transactions that need to be adjusted in consolidated financial statements. In order to make the preparation of consolidated financial statements easier, it's best to identify transactions that will be adjusted. These include any accounts payable, accounts receivable, and sales transactions that occur between the parent company and its subsidiary.[3]

- Mark these transactions with a special reference tag in the ledger so that they can be accounted for at the end of the year.

Preparing Consolidated Financial Statements

-

1Determine if the parent needs to prepare consolidated financial statements. Consolidated financial statements are necessary if the parent exercises majority control over the subsidiary. Majority control means that parent can control what the subsidiary does.[4]

- Since, by definition, parents own more than 50% of the subsidiary’s stock, the parent usually exercises majority control.

- If the subsidiary is going through bankruptcy, a foreign country restricts remittance of profits to the parent, or the parent can’t control the subsidiary’s operations, it may not have majority control and doesn’t have to prepare consolidated financial statements.

-

2Prepare the consolidated financial statements. List the subsidiary’s balance sheet and income statement information next to the parent’s accounting data. Add each line item together to determine the consolidated balance.[5]

- For example, if the parent has $40,000 in accounts receivable and the subsidiary has $30,000 in accounts receivable, the consolidated column should indicate $70,000 of accounts receivable.

-

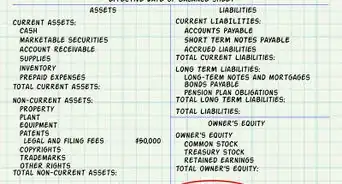

3Adjust intercorporate stock-holdings. Intercorporate stock holding issues cause an overstatement of the outstanding stock balance by reporting subsidiary stock owned by the parent as outstanding stock. This can be remedied with a debit to the subsidiary's common stock, paid-in capital in excess of par, and retained earnings accounts and a credit to the investment in stock of subsidiary account for an equal amount.[6]

- These transactions will be for the book value of the subsidiary stock and related accounts.

- For example, if the parents owns $100,000 in the subsidiary's stock and the subsidiary's retained earnings total $50,000, their common stock and paid-in capital in excess of par would be debited for a total of $100,000 (depending on how much the par value of the stock is) and their retained earnings would be debited for $50,000.

- Then, the parent company's investment in subsidiary stock account would be credited for $150,000.

-

4Adjust intercorporate sales. Intercorporate sales arise from inventory transfers that take place between the parent and the subsidiary. Keep in mind that a sale isn't considered consummated until the item sold to the subsidiary is re-sold to an independent third party. In these cases, one side may report a profit, even though no transaction has taken place. This means that several accounts will be overstated in the consolidated reports.[7]

- Identify these inventory transfers and then debit consolidated retained earnings credit consolidated ending inventory for the value of the transfers.

- For example, if $50,000 worth of product was transferred from the subsidiary to the parent, the consolidated statements would record a $50,000 debit to retained earnings and a $50,000 credit to consolidated ending inventory.

-

5Adjust intercorporate receivables and payables. Intercorporate receivables and payables arise from transactions between the parent and the subsidiary. Essentially, this appears on the consolidated statement like the consolidated company owes itself money. This issue can be fixed with debits to consolidated accounts payable and credits to consolidated accounts receivable as necessary to eliminate intercorporate transactions.[8]

- For example, if a sale is recorded from the subsidiary to the parent in the amount of $20,000 and an entry for accounts receivable is made in the subsidiary's accounts, an entry should be made crediting consolidated accounts receivable for $20,000 to eliminate this transaction.

Expert Q&A

Did you know you can get expert answers for this article?

Unlock expert answers by supporting wikiHow

-

QuestionWhy we do not add the amount of capital share and retained earnings of the subsidiary company in the amount of parent company's share capital and retained earnings while preparing a consolidation statement?

Darron Kendrick, CPA, MADarron Kendrick is an Adjunct Professor of Accounting and Law at the University of North Georgia. He received his Masters degree in tax law from the Thomas Jefferson School of Law in 2012, and his CPA from the Alabama State Board of Public Accountancy in 1984.

Darron Kendrick, CPA, MADarron Kendrick is an Adjunct Professor of Accounting and Law at the University of North Georgia. He received his Masters degree in tax law from the Thomas Jefferson School of Law in 2012, and his CPA from the Alabama State Board of Public Accountancy in 1984.

Financial AdvisorThe shares are already recorded in the investment account and the earnings of the subsidiary are already recorded in the equity of the parent. The adjustments remove the double counting of these items.

Support wikiHow by unlocking this expert answer.

-

QuestionWhat if the subsidiary is cancelled?Darron Kendrick, CPA, MADarron Kendrick is an Adjunct Professor of Accounting and Law at the University of North Georgia. He received his Masters degree in tax law from the Thomas Jefferson School of Law in 2012, and his CPA from the Alabama State Board of Public Accountancy in 1984.

Financial AdvisorThis would not matter as long as it is likely that the money for the payment of the investment is reasonably expected to take place.Support wikiHow by unlocking this expert answer.

-

QuestionHow does one treat the sale of a subsidiary in consolidated financial statements?Darron Kendrick, CPA, MADarron Kendrick is an Adjunct Professor of Accounting and Law at the University of North Georgia. He received his Masters degree in tax law from the Thomas Jefferson School of Law in 2012, and his CPA from the Alabama State Board of Public Accountancy in 1984.

Financial AdvisorThe entity sold would no longer be recorded and the gain or loss would be reported in the period sold.Support wikiHow by unlocking this expert answer.

References

- ↑ http://www.investopedia.com/terms/s/subsidiary.asp

- ↑ http://accounting.utep.edu/sglandon/c12/c12b.pdf

- ↑ https://www.ocf.berkeley.edu/~cchang/pdf%20docs/ch003.pdf

- ↑ https://www.ocf.berkeley.edu/~cchang/pdf%20docs/ch003.pdf

- ↑ http://www.cengage.com/resource_uploads/downloads/0324381980_74249.pdf

- ↑ https://www.ocf.berkeley.edu/~cchang/pdf%20docs/ch003.pdf

- ↑ https://www.ocf.berkeley.edu/~cchang/pdf%20docs/ch003.pdf

- ↑ https://www.ocf.berkeley.edu/~cchang/pdf%20docs/ch003.pdf

About This Article

If you’re a parent company that owns at least 50 percent of another company, you’ll need to know how to account for your subsidiary. To record the parent’s purchase of the subsidiary’s stock, debit Intercorporate Investment and credit Cash. You’ll also want to record any dividends that the subsidiary pays to the parent company by debiting Cash and crediting Intercorporate Investment. When you’re ready to record the parent’s percentage of the subsidiary’s annual profit, you can debit the Intercorporate Investment account and credit the Investment Revenue. As you put together your consolidated financial statements, identify any transactions that need to be adjusted, including any accounts payable, accounts receivable, and sales transactions that occur between the parent company and its subsidiary. For more tips from our Accountant co-author, including how to prepare consolidated financial statements for your subsidiary, keep reading!