wikiHow is a “wiki,” similar to Wikipedia, which means that many of our articles are co-written by multiple authors. To create this article, 23 people, some anonymous, worked to edit and improve it over time.

This article has been viewed 119,995 times.

Learn more...

Do you have family and friends with the heart and the wallet to help you achieve home ownership? New home buyers are increasingly using "intra-family mortgages" of 10-100% of the purchase price to do this. But you need a plan to avoid the hassles and pitfalls of mixing money and relationships. The best way to borrow from people you know is to make the deal as formal as possible. Before you borrow any money you need to be sure that you can pay it back at the agreed terms.

Steps

Finding a Lender

-

1Approach close relatives. Borrowing money to buy a house is a major commitment, potentially involving hundreds of thousands of dollars. For this reason, it’s a good idea to start by canvassing those closest to you, who know you the best, and are able to make judgement about your reliability. Your close family will know you as well as anybody, and should understand your financial situation.

- Never be pushy, or make demands. Rather, be understanding and appreciate that a potential lender is taking a risk to help you.

- Your parents will want to support and help you as much as they can, but you will need to present a good argument and indicate the mutual benefits.

- Your parents may feel obliged to help you, but you must ask them to carefully consider whether or not they can afford it.[1]

-

2Consider friends and extended family. You may also want to consider talking to your extended family as well as some of your friends. You will have to think carefully about who may be interested in helping you, and who has the means to lend you the money. If you deal with friends, there may be a somewhat different dynamic to the relationship.

- Friends are more likely to see a loan as a mutually beneficial way for them to invest their money.

- Don’t be surprised if a distant Aunt you haven’t seen for twenty years isn’t interested in lending you money.

Advertisement -

3Explain the advantages to the lender. When you approach somebody, it is essential that you are able to fully outline the potential benefits to the lender. The main benefits to the lender are a good rate of interest and a steady income stream. With interest rates very low across the world, savers and investors are receiving little return on their money. A loan to a friend or family member could result in a better rate of return than she would get from a bank.

- A loan for a house is such a large sum of money that the loan will be repaid over a long time. The lender will thus have a regular and reliable income stream long into the future.

- Having this predictable income can be a great help for the lender.[2]

-

4Detail how the borrower will benefit. Depending on who you are talking to, and what the context is, it can help to explain how exactly the borrower will benefit. This can go beyond the fact of you being able to buy a house. Borrowing from a friend or family member may mean you are able to secure a loan at a lower rate than if you were borrowing from a bank. Perhaps this lower rate is what makes the purchase possible.

- You may also be able to pay back the loan on more flexible terms, or with an unusual repayment schedule.

- For example, you might be able to agree to pay only interest for the first year and then start paying back the loan itself in the second year.

- Don’t take any of this for granted, and make it clear that you are committed to repaying the loan according to the terms and schedule you agree.[3]

Agreeing Terms

-

1Negotiate a fair and straightforward agreement. Once you have spoken in detail to somebody who is prepared to lend you the money, you need to begin to negotiate the terms of the agreement. You should take this very seriously, and treat it the same as you would a meeting with a bank manager. Bring draft agreements and go through them line-by-line to ensure that everything is clear and agreed. Document everything throughout.[4]

- You will need to agree on the interest rate that the loan will be repaid at. Will this be fixed or variable? If it’s variable you need to have a clear understand of how often the rate can change.

- Bear in mind that the IRS requires intra-family loans to reflect the commercial market.[5]

- You will also have to agree on the repayment schedule. How will you repay the loan, and according to what schedule? Will you make monthly payments, or perhaps bi-monthly or quarterly?

-

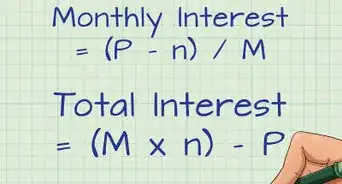

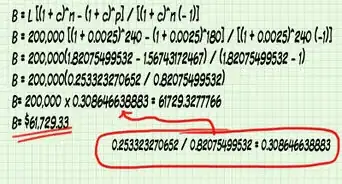

2Set up a repayment plan. Having a clear repayment plan agreed can enable you to plan ahead in order to meet the repayments. Use a loan calculator to input your loan terms and generate the list of due dates and amounts that make up your payment schedule. Borrowing from a friend or family member may make it easier to be a little flexible with repayment dates, but it is important to have a clear plan, and stick to it as much as possible.

-

3Sign a promissory note. Once you have agreed on terms, you will need to complete some paperwork to secure the legality of the agreement and protect the rights of both the lender and the borrower.[6] The first essential document is the promissory note (sometimes referred to as a mortgage note). This is a legally binding document which states that the borrower promises to repay the loan according to the agreed terms.

- The terms will include the interest rate, the payment dates and the frequency of payment.

- All of this information should be provided in the promissory note itself.

- It should also outline any penalties which may be applied if the borrower falls behind in the repayment schedule.[7]

-

4Complete a mortgage agreement or “deed of trust.” You will also need to sign and complete a mortgage agreement, or “deed of trust”, which legally secures (provides collateral for) the promissory note. This document will essentially state that if the borrower does not pay back the loan, the lender can take action to recover the value of the loan. It should state that the lender can, as a final resort, foreclose the property to pay off the loan.

- The document will outline the borrower’s responsibility to make all payments in a timely manner, as well as ensuring the property has hazard insurance.

- This document should state that the borrower is required to properly maintain the property.[8]

-

5Consider legal assistance. These are legally binding documents which deal with significant amounts of money, as well as the personal relationship of two or more people. You should get professional legal help in order to make sure all the paperwork has been completely properly. Hire an attorney to look through the documents independently and discuss all the details and potential implications with you and the lender.[9]

- It is crucial that everybody understands their legal position before the loan is made.

- The attorney will be able to advise you on any issues arising from the loan related to the taxes of the borrower and lender.

Keeping to the Agreement

-

1Repay the loan as agreed. As long as you keep up with your payment plan as spelled out in your promissory note, you are on track to successfully repaying your loan. Even if you are able to meet the payments without difficulties, you and the lender might prefer to put a buffer up so that you are not the ones handling the payments directly.

- Consider hiring a loan manager to deal with the payments and send any reminder notices, annual reports, and other documents.

- Having an outside person dealing with the everyday administration of the loan can help you have a more normal relationship with the borrower.

-

2Keep the lines of communication open. A major factor in a successful private loan is your ability to maintain clear communication and honest transparency with the lender. The lender should make herself available to talk, and hear you out if you have run into temporary financial difficulty. The borrower has a responsibility to be direct and honest with the lender from the start and throughout.

- If you are anticipating having problems making a payment, speak to the lender as soon as possible and be prepared to offer a sensible alternative.

- You might like to set up regular meetings or conversations so you can both keep track of the loan.

- This gives you a formal forum to discuss any issues and work together to find mutually beneficial solutions.[10]

-

3Be open to restructuring. If you run into financial difficulty, and are struggling to make the payments, you should be prepared to work hard to make accommodations which ensure the borrower gets repaid. Treat the loan as you would a loan from a bank, and work with the lender to come up with an alternative payment schedule.[11]

- This could mean increasing the duration of the loan from ten to fifteen years, or altering the repayment schedule so a greater proportion of the loan is paid off in later years.

- Remember that you have to make an offer that benefits the lender as well.

- If you’re asking for a significant extension to the duration of the loan, be prepared to marginally increase the rate of interest.

-

4Keep the loan separate from your relationship. A big part of treating the loan as a professional agreement is keeping it isolated from your day-to-day interactions. Try to avoid talking about the loan at family occasions or when socialising. Keep it something you discuss at specific times, and try to contain it. This will be a lot easier if all the agreements are clear, and everybody is sticking to them.[12]

Warnings

- Be aware of the annual gift tax exemption. According to the IRS, individuals may gift up to $14,000 every year to another individual without incurring gift taxes.[13] Any payments you forgive on a private loan count towards your gift amount for the year to that individual.⧼thumbs_response⧽

- Contact your accountant or tax adviser if you are concerned that through direct gifts or forgiven loan payments you may exceed your gift allowance for the year.⧼thumbs_response⧽

-Step-18.webp)

References

- ↑ https://www.moneyadviceservice.org.uk/en/articles/should-you-borrow-from-family-or-friends

- ↑ http://www.nolo.com/legal-encyclopedia/borrowing-from-family-friends-buy-29649.html

- ↑ http://www.nolo.com/legal-encyclopedia/borrowing-from-family-friends-buy-29649.html

- ↑ http://money.usnews.com/money/personal-finance/articles/2012/08/22/how-to-lend-money-to-family-and-friends

- ↑ http://money.usnews.com/money/personal-finance/articles/2012/08/22/how-to-lend-money-to-family-and-friends

- ↑ http://money.usnews.com/money/personal-finance/articles/2012/08/22/how-to-lend-money-to-family-and-friends

- ↑ http://www.nolo.com/legal-encyclopedia/borrowing-from-family-friends-buy-29649.html

- ↑ http://www.nolo.com/legal-encyclopedia/borrowing-from-family-friends-buy-29649.html

- ↑ http://www.nolo.com/legal-encyclopedia/borrowing-from-family-friends-buy-29649.html

- ↑ http://money.usnews.com/money/personal-finance/articles/2012/08/22/how-to-lend-money-to-family-and-friends

- ↑ http://learnbonds.com/13480/lending-money-to-family/

- ↑ http://www.businessinsider.com/how-to-borrow-money-from-friends-and-family-without-destroying-your-relationships-2014-3?IR=T

- ↑ http://www.forbes.com/sites/deborahljacobs/2011/08/22/6-ways-to-give-family-and-friends-financial-aid/