This article was co-authored by Samantha Gorelick, CFP®. Samantha Gorelick is a Lead Financial Planner at Brunch & Budget, a financial planning and coaching organization. Samantha has over 6 years of experience in the financial services industry, and has held the Certified Financial Planner™ designation since 2017. Samantha specializes in personal finance, working with clients to understand their money personality while teaching them how to build their credit, manage cash flow, and accomplish their goals.

There are 8 references cited in this article, which can be found at the bottom of the page.

This article has been viewed 25,795 times.

Learning how to manage personal finances is vital, but financial literacy is rarely taught in schools. Whether your child or student is in elementary school or in their late teens, teaching them about finances can set them up for success later in life. Start by teaching them about budgeting and managing expenses. Explain how credit works, why it’s important, and how to use credit cards responsibly. Stress the importance of saving, and introduce the basic ways to invest money. Since money management can be abstract and complex, use apps and other resources to simulate concrete real-world scenarios.

Steps

Introducing Budget Management

-

1Explain how to accurately estimate income and expenses. Make a spreadsheet or write a sample monthly budget with a pen and paper. List total income, and break expenses up into categories, such as car payments, insurance, a cell phone bill, and entertainment.[1]

- Mention that income and expenses can fluctuate month to month, so tracking them over time is important.

-

2Make the sample budget relevant for your student or child. For instance, include your teenager’s actual income and spending from last month. List after-tax income from their part-time job and add up their car insurance, cell phone bill, clothes, haircut, and money spent going out with friends.[2]

- Start with these basic examples, then introduce a more complex sample budget that includes rent, utilities, and groceries.

- For younger students, use simple values, such as a $10 weekly allowance and candy, toys, and other small expenses.

Advertisement -

3Explain the difference between a need and a want. Tell your learner that housing, utilities, and other core bills are spending priorities. If money’s tight, paying rent or car insurance is more important than going out to eat or buying a new cell phone.[3]

- Subtract their expenses from income, and discuss how balancing needs and wants impacts their budget. Ask them to identify needs that take priority and wants that can be cut to save money.

-

4Show them how to make bill payments. Mention that the most common ways to pay bills are via check or debit. Show them a physical check and explain how to fill in the date, payee, payment amount, and signature fields. Then go to an online bill payment portal and explain how to fill in debit card billing information.[4]

-

5Introduce the importance of saving money. While saving money is a distinct topic with its own lesson plan, you’ll need to mention it when you explain budgeting. Let them know that saving 10 to 20 percent of their income is crucial, and they’ll need to save more of their income as they get older.[5]

- Include specific reasons to save, such as for an emergency, a down payment on a home, and retirement.

- You can also teach them to create different savings to help them save for multiple goals. Show them that they can even physically put money into separate jars or envelopes to keep track of how much they've saved.[6]

-

6Use budgeting resources to simulate real-world scenarios. After covering the basics, have your learner create and manage hypothetical budgets using smartphone apps. Personal finance simulators can provide accessible, concrete examples and reinforce budget management skills.[7]

- For example, use the Budget Challenge app, which is free for iOS and Android devices: https://www.budgetchallenge.com.

Explaining Credit and Debt

-

1Define credit and its broad impacts on life. Explain that credit is when a lender gives you money and expects you to pay it back by a due date or with interest, which is an added percentage. Tell them that if they don’t repay a line of credit, they’ll have a harder time getting leases, mortgages, cars, jobs, and other life essentials.[8]

- Understanding credit is an important first step towards financial literacy. If the person already has some debt, you can also help them come up with a basic payment plan for handling that debt.[9]

-

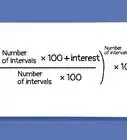

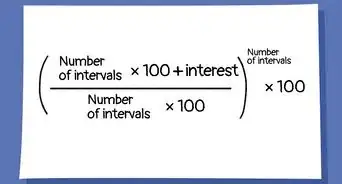

2Describe how interest works. Explain that they won’t have to pay interest if they pay off a credit card balance by its due date. Mention that the better credit you have, the lower your interest rate will be on credit cards, mortgages, and car loans. Explain that interest on a loan can capitalize if it’s not paid, which is when it becomes part of the principle, or original loan amount.[10]

- Compare a credit balance with library books to help them understand. If they return the book they borrowed, they won’t have to pay extra. If they keep the book past its due date, they’ll have to pay extra, or interest.[11]

-

3Explain how credit scores are calculated. Tell your student that it takes time to earn a good credit score. Explain that the score is based on payment history, amounts owed, length of credit history, new credit and recently opened accounts, and types of credit in use. Stress that a low number will negatively impact their ability to get loans, leases, jobs, and other necessities.[12]

-

4Stress the importance of using a credit card responsibly. Let them know that having a credit card is an important part of building credit, but they must use it responsibly. Tell them they can’t use the card to make a purchase they can’t afford. Remind them of the library book analogy to stress the importance of paying of a balance by the due date.[13]

- Mention that if they don’t pay off a balance and credit card debt piles up, their credit score will take a major hit.

Spelling out Savings and Investments

-

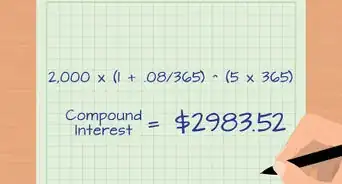

1Discuss the importance of saving and growing money. Remind them of the reasons that they need to save, from emergencies to retirement. Explain that money can grow when invested properly. Mention that, while there are risks, if they invest $10,000, they can earn tens of thousands of dollars over the course of 20 years.[14]

-

2Describe how checking and savings accounts work. Explain that a checking account is primarily used for making payments and a savings account is for holding money. Mention that bank accounts earn interest, and a savings account earns more interest and should be left alone.[15]

- Teach them to automatically put away a little money each time they receive any. For instance, if they're working, they might put $25 out of each paycheck into a savings account.[16]

-

3Explain the various types of investments. Tell your learner that, as they get older, they should think about investing money in the stock market. Let them know that there are risks, but investments are a good way to grow money for retirement. Explain that there are a variety of ways to invest money, and go over the basic types of investments.[17]

- Stocks are when you purchase a small amount of ownership in a company. If the company performs well, your investment becomes more valuable.

- Mutual funds and exchange-traded funds (ETFs) are pools of money from lots of investors that are used to purchase a diverse range of investments. Since they hold dozens or hundreds of securities, or investments, they’re less risky than purchasing stock in a single company.

- Bonds are when you lend money to a government or a business for a specific length of time at a fixed interest rate. While they’re lower risk, bond earnings are lower-yield investments.

-

4Discuss risk and diversification. After introducing basic types of investments, tell your learner that each has a degree of risk. If they invest in 1 company that goes under, their investment will lose value. In order to lower their risk, they need to diversify, or invest in many companies and other investment categories (such as natural resources or real estate).[18]

-

5Use stock market games to simulate investing. After introducing the basics, have your student play investment simulation games. Smartphone apps can help make complex, abstract aspects of investing more concrete and accessible.[19]

- Wall Street Survivor is a helpful free resource: http://www.wallstreetsurvivor.com.

Expert Q&A

-

QuestionHow can I start saving money from nothing?

Samantha Gorelick, CFP®Samantha Gorelick is a Lead Financial Planner at Brunch & Budget, a financial planning and coaching organization. Samantha has over 6 years of experience in the financial services industry, and has held the Certified Financial Planner™ designation since 2017. Samantha specializes in personal finance, working with clients to understand their money personality while teaching them how to build their credit, manage cash flow, and accomplish their goals.

Samantha Gorelick, CFP®Samantha Gorelick is a Lead Financial Planner at Brunch & Budget, a financial planning and coaching organization. Samantha has over 6 years of experience in the financial services industry, and has held the Certified Financial Planner™ designation since 2017. Samantha specializes in personal finance, working with clients to understand their money personality while teaching them how to build their credit, manage cash flow, and accomplish their goals.

Financial PlannerPut aside money from every paycheck as soon as you receive it. Start with a small, manageable amount, like $25. -

QuestionWhat are the first things I should teach someone about managing money?Samantha Gorelick, CFP®Samantha Gorelick is a Lead Financial Planner at Brunch & Budget, a financial planning and coaching organization. Samantha has over 6 years of experience in the financial services industry, and has held the Certified Financial Planner™ designation since 2017. Samantha specializes in personal finance, working with clients to understand their money personality while teaching them how to build their credit, manage cash flow, and accomplish their goals.

Financial PlannerI would start with explaining how credit works. If they have any debt, take a look at that and come up with a payment plan for it. I would also teach them how to build a cash savings and emergency fund, as well as how to create different saving pots for different goals.

References

- ↑ https://www.investopedia.com/university/teaching-financial-literacy-teens/teaching-financial-literacy-teens-budgeting.asp

- ↑ https://www.investopedia.com/university/teaching-financial-literacy-teens/teaching-financial-literacy-teens-budgeting.asp

- ↑ https://www.theguardian.com/education/teacher-blog/2013/mar/04/financial-education-teaching-resources

- ↑ http://www.tdbank.com/wowzone/lessons/Gr2-3Lesson3.pdf

- ↑ https://www.investopedia.com/university/teaching-financial-literacy-teens/teaching-financial-literacy-teens-budgeting.asp

- ↑ Samantha Gorelick, CFP®. Financial Planner. Expert Interview. 6 May 2020.

- ↑ https://www.usnews.com/education/blogs/high-school-notes/2014/03/03/3-ways-to-engage-high-schoolers-in-personal-finance

- ↑ https://www.investopedia.com/university/teaching-financial-literacy-teens/teaching-financial-literacy-teens-credit-and-debt.asp

- ↑ Samantha Gorelick, CFP®. Financial Planner. Expert Interview. 6 May 2020.

- ↑ https://www.investopedia.com/university/teaching-financial-literacy-teens/teaching-financial-literacy-teens-credit-and-debt.asp

- ↑ http://www.tdbank.com/wowzone/lessons/Gr4-5Lesson3.pdf

- ↑ https://www.investopedia.com/university/teaching-financial-literacy-teens/teaching-financial-literacy-teens-credit-and-debt.asp

- ↑ https://www.investopedia.com/university/teaching-financial-literacy-teens/teaching-financial-literacy-teens-credit-and-debt.asp

- ↑ https://www.investopedia.com/university/teaching-financial-literacy-teens/teaching-financial-literacy-teens-investing.asp

- ↑ http://www.tdbank.com/wowzone/lessons/Gr2-3Lesson3.pdf

- ↑ Samantha Gorelick, CFP®. Financial Planner. Expert Interview. 6 May 2020.

- ↑ https://www.investopedia.com/university/teaching-financial-literacy-teens/teaching-financial-literacy-teens-investing.asp

- ↑ https://www.investopedia.com/university/teaching-financial-literacy-teens/teaching-financial-literacy-teens-investing.asp

- ↑ https://www.investopedia.com/university/teaching-financial-literacy-teens/teaching-financial-literacy-teens-investing.asp

About This Article