This article was written by Jennifer Mueller, JD. Jennifer Mueller is an in-house legal expert at wikiHow. Jennifer reviews, fact-checks, and evaluates wikiHow's legal content to ensure thoroughness and accuracy. She received her JD from Indiana University Maurer School of Law in 2006.

There are 7 references cited in this article, which can be found at the bottom of the page.

This article has been viewed 70,792 times.

When you sign a car loan, your lender retains a security interest in your car. This means if you don't make the payments in time, the lender can repossess your car and sell it to pay back the loan. If your car has been repossessed, you typically can get it back by paying off the loan in full. However, if you can't afford to do that, you may be able to get the loan reinstated. Since not all states require lenders to reinstate car loans after repossession, you typically must negotiate with your lender – but you must act fast, because you lose the right to do anything after your car is sold.[1]

Steps

Negotiating with Your Lender

-

1Check your loan agreement. Your loan agreement may contain a clause allowing for reinstatement, or provide other information regarding the procedure after repossession.[2] [3]

- Even if reinstatement isn't built into your law, some states such as California provide you with the right to reinstate your car loan if your car is repossessed.

- You can find a list of automobile repossession laws in every state at http://www.creditinfocenter.com/legal/auto-repossession-laws.shtml, along with links to each state's law.

-

2Contact your lender. Unless your lender has a dedicated line for repossessions, you typically can call the lender's general customer service number.[4] [5]

- If you've previously dealt with a certain individual, you may want to speak with him or her first. Having an existing relationship with the representative may help your case.

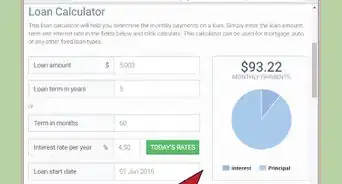

- Ask your lender for a reinstatement quote. Your lender will send you a written notice with the reinstatement quote and the amount of money you must pay to bring your loan current.

- If you live in a state that provides you with the right to reinstatement, you're on better footing – even if reinstatement is not included in your loan agreement. Make sure you read up on your state's law and understand your rights before you call.

- Keep in mind that even in states with laws that give you the right to reinstate your loan, you have an extremely short period of time – typically 15 days – after your car has been repossessed to request reinstatement.[6]

Advertisement -

3Consider consulting an attorney. If the lender is unwilling to negotiate with you, an experienced consumer rights or debt attorney may be able to help you work with the lender to get your car back.[7]

- To find an attorney, look for a consumer debt or credit attorney who is licensed to practice in your area. Many local bar associations have searchable directories on their websites.

- Bar associations also often have attorney referral programs, where you describe your situation and are matched with attorneys who are best able to help you.

- Many attorneys are willing to provide a free consultation, so you don't have anything to lose in at least talking to someone, even if you ultimately decide you cannot afford an attorney.

- However, keep in mind that an attorney's fees may be outweighed by the fees you would pay to the lender and the repossession lot to get your car back.

- In some instances, an attorney may be able to get late fees dropped, get the repossession fees dropped, or work with the lender to adjust your interest rate or refinance your car on terms that are more affordable to you.

-

4Offer alternatives. If you don't have enough money to cover the back payments, you may be able to arrange for a partial reinstatement or a new payment plan.[8]

- When you receive a reinstatement quote, it typically is only good for a couple of weeks. Check the notice for the deadline.

- If you are unable to pay the amount required to bring the loan current, ask about a partial reinstatement. This will enable you to get your car back without paying everything you owe.

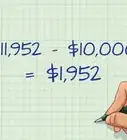

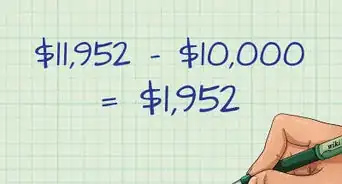

- For example, suppose you haven't made your $200 car payment in three months, so you owe your lender $600. You are able to pay $300 of that. Your reinstatement quote requires monthly payments of $225. If you can pay $275 for six months, you can offer to spread out the back payments and pay them along with your regular loan payment.

- As much as you want to get your car back, make sure you're not getting in over your head. Don't offer a monthly amount that you doubt you'll be able to pay on a regular basis.

- Keep in mind that even if your state gives you the right to reinstate your car loan, you may lose that right if your car is repossessed a second time.[9]

-

5Make payment arrangements. Unless your lender has agreed to an alternate arrangement, you typically must pay all of the overdue payments upfront along with fees to have your loan reinstated.[10] [11]

- Your reinstatement quote should include the amount of money you must pay your lender to bring your car loan current. There may be late fees and penalties included in this amount.

- If you've negotiated an alternative deal with your lender, you may want to ask for another written statement of the amount now due to reinstate your loan.

- Make sure you have in writing the amount you have to pay before you send payment to your lender.

- Take a hard look at your budget, and make your monthly car payment a priority. After your car has been repossessed once, you may have less leeway if you miss a payment again.

- In some cases the repossession fees will be included in the payment you make to your lender. If they aren't, you can expect to pay these fees at the lot when you pick up your car.

-

6Consider using a credit counseling service. If you are significantly behind on other bills, or are having difficulty budgeting monthly payments, a licensed credit counselor can assist you in making your bills more manageable.[12] [13]

- The U.S. Trustee Program has a searchable list of approved credit counseling agencies available at http://www.justice.gov/ust/list-credit-counseling-agencies-approved-pursuant-11-usc-111. If you decide to use a credit counseling service, choose one from this list to avoid being charged excessive fees.

- The credit counseling service will send you free information regarding the process so you can determine if it would benefit you.

- A credit counselor will look at your entire financial situation and help you work with your creditors to create a debt management program that fits in your budget and will help get you out of debt.

-

7Sign any documents. If your reinstatement comes with different terms than applied to the original loan, you may have to sign a new loan agreement.

- Read your loan agreement carefully before you sign it, and make sure you understand the amount of your payments each month and how many months are left on your loan.

- Also make sure you understand the interest rate being charged and what will happen if you get the loan refinanced or pay it off early.

- If you can afford to do so, you may want to set up automatic payments with your lender. The amount of your car loan will be withdrawn from your bank account each month on the due date.

Getting Your Car Back

-

1Find out where your car is located. The address where your car is being kept typically will be on the repossession notice you received.[14]

- If you haven't received a repossession notice yet, you can probably find out the location of your car by calling your lender.

-

2Gather documents. You will need to bring identification documents such as a driver's license, as well as documents that prove you are allowed to take back the car.

- Make sure you have your original retail installment sales contract as well as your new reinstatement contract and copies of all communication between you and the lender.

- If you receive any written notices assuring you of your right to reclaim your car, bring copies of those as well. You also should bring proof of your payment.

- You typically will need to bring your driver's license and proof of insurance before the lot custodian will allow you to drive your car off the property.

- Keep the name and direct phone number of the person you worked with to have your loan reinstated. If you have any trouble getting your car back, you will need to call that person and have them talk to the lot attendant.

-

3Ask about repossession fees. Because auction lots can charge holding and repossession fees that may add up to several hundred dollars, you should call the lot before you go and find out how much you'll be charged.[15]

- Find out what methods of payment are acceptable. Keep in mind many of these lots will want a money order or cashier's check and won't accept a credit card.

- In addition to towing, the lot where your car is being kept will charge a holding fee for each day it sits on the lot before it is sold. If the car had been sold, these fees typically would have been passed on to the individual who bought the car at auction.

- In some cases you can get the repossession fees waived. You might want to consider talking to a bankruptcy or consumer rights lawyer about your options – especially if the fees on top of the amount you already paid the lender will put you in a bind.

- When you call the lot, ask what documents will be necessary for you to reclaim your car. Make sure you have everything listed so you won't run into any problems.

- Write down exactly what you need when you speak to the lot attendant, and repeat the list back to confirm it. Also get the name of the person with whom you spoke.

-

4Arrange to pick up your car. You'll typically want to get a friend to drive you to the lot so you can complete any necessary paperwork and retrieve your car.[16]

- Keep in mind that it may take up to a week for your car to be ready for you. This doesn't necessarily mean that you're going to have problems getting your car back, but keep in touch with your lender and with the lot until the car is back in your possession. Don't just wait for a call.

- Once you're at the lot, be ready to call your lender if the lot attendant refuses to give you your car back.

- When you get your car, check for any personal items you may have kept in the car before you drive off the lot. You have a right to these items, and if they've been removed from the car the lot custodian or your lender should be able to tell you how you can retrieve them.

References

- ↑ http://www.nolo.com/legal-encyclopedia/car-repossession-redemption-v-reinstatement.html

- ↑ http://www.nolo.com/legal-encyclopedia/car-repossession-redemption-v-reinstatement.html

- ↑ http://www.bblocklaw.com/denial-of-the-right-to-reinstate/

- ↑ http://www.nolo.com/legal-encyclopedia/car-repossession-redemption-v-reinstatement.html

- ↑ http://www.bblocklaw.com/denial-of-the-right-to-reinstate/

- ↑ http://www.nolo.com/legal-encyclopedia/the-bank-repossessed-car-how-much-time-i-back.html

- ↑ http://www.bblocklaw.com/denial-of-the-right-to-reinstate/

- ↑ http://www.nolo.com/legal-encyclopedia/car-repossession-redemption-v-reinstatement.html

- ↑ http://www.bblocklaw.com/denial-of-the-right-to-reinstate/

- ↑ http://www.nolo.com/legal-encyclopedia/car-repossession-redemption-v-reinstatement.html

- ↑ https://www.consumer.ftc.gov/articles/0144-vehicle-repossession

- ↑ https://www.consumer.ftc.gov/articles/0150-coping-debt

- ↑ https://www.consumer.ftc.gov/articles/0153-choosing-credit-counselor

- ↑ http://www.nolo.com/legal-encyclopedia/required-notices-car-repossessions.html

- ↑ https://www.consumer.ftc.gov/articles/0144-vehicle-repossession

- ↑ https://www.consumer.ftc.gov/articles/0144-vehicle-repossession

About This Article

If your car’s been repossessed by your lender, you may be able to get your loan reinstated. Check your loan agreement to see if there’s a clause about reinstatement. Some states mandate loan companies to offer reinstatement, but this is usually within a brief period like 15 days. Contact your lender and ask for a quote to reinstate your loan. You may have to pay a fee, lump sum, or cover all of your missed payments. If you can’t afford your back payments, ask them about a partial reinstatement so you can get your car back without paying everything. Just make sure you can afford the repayments so your car doesn’t get repossessed again. For more tips from our Legal co-author, including how to get help from an attorney when your car’s repossessed, read on.