This article was co-authored by Samantha Gorelick, CFP®. Samantha Gorelick is a Lead Financial Planner at Brunch & Budget, a financial planning and coaching organization. Samantha has over 6 years of experience in the financial services industry, and has held the Certified Financial Planner™ designation since 2017. Samantha specializes in personal finance, working with clients to understand their money personality while teaching them how to build their credit, manage cash flow, and accomplish their goals.

There are 11 references cited in this article, which can be found at the bottom of the page.

wikiHow marks an article as reader-approved once it receives enough positive feedback. In this case, several readers have written to tell us that this article was helpful to them, earning it our reader-approved status.

This article has been viewed 463,015 times.

Buying a new or used car, for most people, is not a purchase made by writing a check or handing over cash for the full amount. At least part of the amount is typically financed. If you do finance a car, it's important that you understand exactly how much you'll be paying every month, otherwise you could end up going over budget.

Steps

Determining the Amount to Finance

-

1Settle on the price of the vehicle that you're buying with the dealership or seller. You might be able to pay a lower price than the sticker or asking price by negotiating with the seller. Once you settle on a price, however, that's your starting point.

- For example, suppose you negotiate a deal to purchase a new car for $19,055. You have a down payment and your old car to trade-in, and you qualify for a customer cash rebate. You plan to finance the rest of the cost with an auto loan.

-

2Calculate the amount of state sales tax and add it to the estimated purchase price. Also find out how much your state charges for tax and title fees. Add this to the cost of the car. [1]

- Some states don’t allow a deduction of sales tax on trade-ins; you must pay tax on the total cost.

- For the example, suppose your state charges 7 percent sales tax and an additional $200 for tags and title fees.

- The sales tax would be .

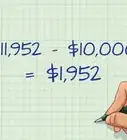

- The cost of the car would now be $20,590 .

Advertisement -

3Deduct the trade-in value from the price of the car (if applicable). It may be the case that you're trading in your old vehicle to help pay for the new one. Once you've settled on a trade-in value with the dealership, deduct that amount from the purchase price of the car.

- The dealer offers you $3,000 for your trade-in. This brings the cost of the car down to $17,590 .

-

4Add any fees that the dealer charges. Dealer fees vary depending on your state and whether you are purchasing a new or used car. Destination fees pay for the cost of delivering a new vehicle from the factory to the car dealership. Documents fees (also known as “doc” fees or conveyance fees) include loan processing fees and service and handling fees. Some states have caps on documents fees.[2] [3]

- The dealer charges you $500 in destination and vehicle preparation fees. This brings the cost of the car to $18,090 .

-

5Subtract any rebates or incentives for which you qualify. You may qualify for these discounts when purchasing a new car. Manufacturers and car dealers use them to steer customers away from the competition and ensure brand loyalty. Research available incentives and rebates ahead of time to potentially save thousands of dollars on a new car.[4]

- Typical rebates include customer cash for brand loyalty and dealer cash that may be passed along to the customer.

- Common incentives include low annual percentage rate (APR) financing for customers with excellent credit and special lease programs.

- You qualify for a brand loyalty rebate of $1,000. The cost of the car is now $17,090 .

-

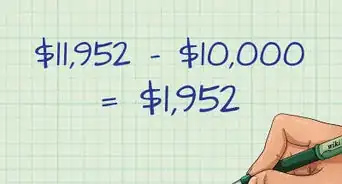

6Subtract the down payment from the loan. The down payment is the amount of cash that you're putting down to pay for the car.[5] This amount will vary from sale to sale and is based on what you can afford to pay out of pocket immediately. Deduct that amount from the amount to be financed.

- Your down payment is $2,000. This brings the total cost of the car down to $15,090 .

- The amount you need to finance, or borrow, is $15,090.

Calculating Auto Loan Payments

-

1Understand how auto loans work. Auto loans are what is known as an amortizing loan. The creditor lends you the principal amount, which is the cost of the car. You pay the creditor back plus interest. The principal and interest are paid down (or amortized) in equal payments over the life of the loan.[6]

- The monthly payments remain the same, but the interest piece of the payment decreases and the principal piece increases over the course of the loan.

-

2Learn the formula for loan amortization. The term “amortization” means paying down the loan in equal installments. The formula will tell you how much each payment will be. The information you need is the amount of the loan, the interest rate per month and the total number of months that you will make a payment.[7]

- Use the formula .

- A = the monthly payment.

- P = the principal

- r = the interest rate per month, which equals the annual interest rate divided by 12

- n = the total number of months

-

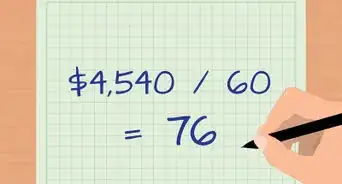

3Calculate your monthly loan payment. Using the above example, you need to borrow $15,090 to purchase the car. This is the principal. You qualify for an auto loan that lasts 4 years, or 48 months and charges 7 percent annual interest. You will repay the loan (including principal and interest) in 48 equal payments (once per month).

- Calculate the interest rate per month. The annual interest rate is 7 percent. Divide this by 12 to get the monthly interest rate. The monthly interest rate is 0.583 percent

- .

- .

- Your monthly payment will be $361.07

Using Microsoft Excel to Calculate Auto Loan Payments

-

1

-

2Get the correct information. You'll not only need your loan information, but you'll also need to modify them slightly to get the correct value.

- Multiply the length of the loan in years by 12. You want to calculate monthly payments, not annual payments, so you'll need the total number of months throughout the life of the loan. For example, if the loan is for four years, then the number of months is 4 * 12, or 48.

- Since you want to pay off the loan completely, the future value of the loan will be 0. This means that you won't owe any more money at the end of the payment stream.

-

3Create headers for your Microsoft Excel spreadsheet. Launch Excel and type these words on the first 4 rows in column A:

- Rate

- Number of Payments

- Present Value

- Future Value

-

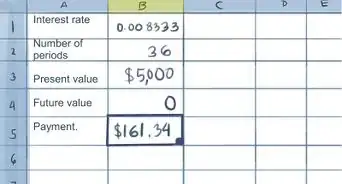

4Enter the values that you'll use to calculate your payments. Plug the following numbers in column B next to the descriptions:

- 7.00%

- 48

- 15,090

- 0

-

5Use the Microsoft Excel function to calculate the payment. Input the formula “=PMT(B1/12,B2,B3,B4)” in a cell below the numbers.

- Type “=PMT(“ and click on the cell with 7.00% so “B1” appears after the left parentheses.

- Type “/12,” (including the comma). Remember, you're dividing by 12 because you're calculating the interest rate on a monthly basis and the interest rate you were given is on an annual basis.

- Click on the cell with 48 to see “B2” appear.

- Type a comma after “B2” and click on the cell with 15,090 to see “B3” appear.

- Type a comma after “B3” and click on the cell with 0 to see “B4” appear.

- Type a right parenthesis at the end to complete the formula.

-

6Perform the calculation. Press the “Enter” key and the formula will be replaced with the monthly payment of $361.35.

-

7Alter the payment. Change any of the variables, such as the finance amount or number of months, to see how the monthly payment changes.

-

8Calculate the loan payment without Excel. If you want to double-check Excel's math or you don't have access to Excel, you can get your loan payment by using one of the many loan payment calculators that are online.[10]

Expert Q&A

Did you know you can get expert answers for this article?

Unlock expert answers by supporting wikiHow

-

QuestionIs there anything I can do to lower my auto loan payments?

Samantha Gorelick, CFP®Samantha Gorelick is a Lead Financial Planner at Brunch & Budget, a financial planning and coaching organization. Samantha has over 6 years of experience in the financial services industry, and has held the Certified Financial Planner™ designation since 2017. Samantha specializes in personal finance, working with clients to understand their money personality while teaching them how to build their credit, manage cash flow, and accomplish their goals.

Samantha Gorelick, CFP®Samantha Gorelick is a Lead Financial Planner at Brunch & Budget, a financial planning and coaching organization. Samantha has over 6 years of experience in the financial services industry, and has held the Certified Financial Planner™ designation since 2017. Samantha specializes in personal finance, working with clients to understand their money personality while teaching them how to build their credit, manage cash flow, and accomplish their goals.

Financial PlannerYou can lower some of the other costs associated with your car, like your car insurance. For instance, you can take a defensive driving class, or you can increase your deductible to lower your monthly payments.

Support wikiHow by unlocking this expert answer.

References

- ↑ http://www.salestaxinstitute.com/resources/rates

- ↑ https://www.cars.com/articles/2014/06/everything-you-ever-wanted-to-know-about-a-dealer-doc-fee/

- ↑ https://help.edmunds.com/hc/en-us/articles/206102367-Destination-Charges

- ↑ http://www.edmunds.com/car-buying/how-to-use-new-car-incentives-and-rebates.html

- ↑ http://www.investopedia.com/terms/d/down_payment.asp

- ↑ http://www.accountingcoach.com/blog/what-does-it-mean-to-amortize-a-loan

- ↑ http://www.vertex42.com/ExcelArticles/amortization-calculation.html

- ↑ https://support.office.com/en-us/article/Financial-functions-reference-5658d81e-6035-4f24-89c1-fbf124c2b1d8

- ↑ https://support.office.com/en-us/article/PMT-function-0214da64-9a63-4996-bc20-214433fa6441

- ↑ http://www.bankrate.com/calculators/mortgages/loan-calculator.aspx

- ↑ Samantha Gorelick, CFP®. Financial Planner. Expert Interview. 6 May 2020.

About This Article

To calculate auto loan payments, start by finding the monthly interest rate by dividing the annual interest rate by 12. Then, find the principal, which is how much you need to borrow to purchase the car. Next, determine how many months you'll be paying the loan off for. Once you have all of this information, plug it into the formula for loan amortization and solve to find the monthly payment. To learn how to calculate auto loan payments using Excel, scroll down!