This article was co-authored by Michael R. Lewis. Michael R. Lewis is a retired corporate executive, entrepreneur, and investment advisor in Texas. He has over 40 years of experience in business and finance, including as a Vice President for Blue Cross Blue Shield of Texas. He has a BBA in Industrial Management from the University of Texas at Austin.

There are 8 references cited in this article, which can be found at the bottom of the page.

wikiHow marks an article as reader-approved once it receives enough positive feedback. In this case, 89% of readers who voted found the article helpful, earning it our reader-approved status.

This article has been viewed 54,423 times.

Living on a modest or minimal income can be tiring and stressful, but by budgeting and seeking aid when necessary, you can survive on a surprisingly small amount of money. Federal, state, and local governments also provide aid for low-income individuals and families, and by combining this help with other cost saving measures you can stretch your income and make ends meet.

Steps

Creating a Budget

-

1Analyze your spending. If you find you’re having trouble getting by on the amount of money you bring in, start by getting a sense for where that money is going. Jot down a list of your known monthly expenses, like rent, utilities, transportation, etc. Then use your three most recent months of credit card and bank statements to categorize your other spending into food, household necessities, healthcare, entertainment, or other. Figure out on average how much you spend each month in each category, and use this as a baseline.

-

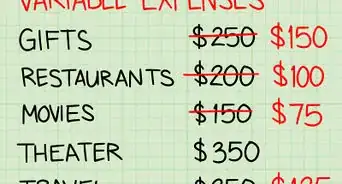

2Choose where to save. Once you’ve written down all of your expenses, you can look at the categories and decide where you can save money. Are there ways you can reduce your spending on food, entertainment, or other expenses? Are you spending more than you realized on food and clothing? Analyze each line item and be realistic about whether or not you can reduce it.Advertisement

-

3Create a budget. Using your list of historical spending and combining the areas you plan to improve, create a monthly budget that you will work off of going forward. Don’t budget for less than you can get by on — just try to eliminate anything you truly don’t need. Once you’ve decided on this budget, stick to it as closely as you can and adjust it only deliberately.

- You can write down your budget in a visible place, like on your fridge or front door, and check in once a week in how you are doing. Having a visual representation of your spending can help you keep track of it, and motivate you to meet your savings goals.

- If you prefer electronic budgeting, tools like Mint.com and other budgeting software connect to your accounts, and allow you to see your budget and spending online.

-

4Consider using cash. Financial experts often recommend that if you are on a low monthly budget, you only use cash to make purchases. This avoids the charges that come with credit cards, and ensures you know how much you are spending — using a card (even a debit card) can make it difficult to keep track of how much money you are actually spending. Think about switching to this method at least for the first few months on your new budget, to help you adjust to your new spending pattern and avoid any extra charges using a credit card might bring.

Finding ways to Save

-

1Save on rent. You can save the most by reducing expense categories that are highest, such as rent or mortgage, so ask yourself if you can spend less on your housing.

- If you’re in a housing situation where you can leave without paying a penalty, look around for lower rent.

- Really hardcore? Microhousing is the latest form of cheap living, whether by renting a micro apartment or by buying a tiny house. If you’re really embracing the simple lifestyle long-term, this may be a great saving option for you.

-

2Reduce your utility bills. Another type of monthly expense is utilities, or bills like water, sewer, electricity, cable, internet, garbage service, and natural gas. While some of these expenses are necessary, there are ways to reduce your use of utility services and save.

- Take showers instead of baths, and be brief. Also make sure your faucets are always completely turned off and you have no leaks to keep from wasting extra water.

- Always turn off the lights in rooms you are not using.

- Insulate your windows during the winter using clear plastic or bubble wrap, to stop heat from escaping into the outdoor cold. This will help reduce your electricity bill.[1]

- If you have internet service on your cell phone, consider getting rid of your cable internet, and doing your computer-based online work at a public library, where internet is free. You can check email and facebook on your phone, but may be able to save by getting rid of cable internet.

- Many cable and cell phone companies are in intense competition for business, so there are many ways to save on those bills by keeping your eyes and ears open. Pay as you go cell phones tend to be much cheaper than new ones, and by getting rid of cable and just using Netflix or HuluPlus, you can save hundreds each year.

- In some locations, energy has been deregulated, which gives consumers the opportunity to shop around for the lowest price.

-

3Save on food. Another large household expense is food. While you can’t eliminate the need to eat every day, you might be able to get more for less by reexamining how you spend money on food. Generally you will save more by eating at home instead of at restaurants, and by buying fresh food to prepare rather than pre-made meals.

- Food Studies scholar Leanne Brown's book Good and Cheap provides nutritious recipes you can make at home for $4 a day.[2] Consider using this or a similar cook book to plan low-budget meals in advance.

- Staple foods like rice, beans, and lentils are really nutritious and inexpensive. You can use these low-cost items to make the bases of your meals, and then add in fresh vegetables, spices, meat, or other items to liven up the meal. If you consistently use these staples to feed yourself, you can save tremendously on your monthly grocery bill.

- Couponing is another way to save on food or household items. You can look out for coupons for items you were already planning to buy, or you can plan your menu each week around couponed items.

- Consider buying non-perishables in bulk. Things like toothpaste, paper towels and toilet paper, trash bags, plus dry pasta, oatmeal, and dry rice and beans should be bought in bulk to save you money long-term.[3] Produce and other things that perish quickly should be purchased in smaller quantities, unless you plan to freeze them (and have room to do so).

-

4Eat out less. Every time you eat out, you pay for the food you buy, as well as the labor for the person who prepares it, all the packaging for the meal or the server, and the environment you’re eating in. Simply put, you can save money by not eating out altogether or reducing the amount you do.[4]

- You can save when you do eat out by choosing more simple meals or side dishes, eliminating alcoholic beverages from your restaurant purchases, or finding deals like happy hour.

-

5Save on transportation. Another expensive item is transportation. You can save on transportation costs by biking or walking to work as often as possible, carpooling, or using public transportation instead of driving. These small savings (which can include saving on gas, parking, and wear on your vehicle) can add up and impact your bottom line — adding some funds back for eating or utilities.

- Ask your employer if they offer or support ride-share programs.

- Many employees now work from home one or more days a week, which saves the cost and time of commuting. Consider asking your employer whether you can work from home full-time or even just occasionally, if your job allows.

-

6Buy used. Another brilliant way to save is to shop first at second hand stores. This doesn’t mean you buy everything you own at Goodwill — just make a practice of searching craigslist and the local thrift shop first before buying anything over $50. (Some examples are kitchen equipment, household furniture, clothing, or electronics.) Remember that buying used only saves if you already needed the item, but if you make a practice of buying used when you can, you will begin to reap the savings.

-

7Have fun for free. Instead of spending money on movie tickets and plays, check out the free entertainment in your area. Most towns have a public library where anyone can borrow books, audiobooks, or even movies, for free. Some cities have free movies or concerts in the park during the summer, where anyone can bring a blanket and watch.

Qualifying for Government Assistance

-

1Seek housing assistance. Rent is most people’s largest monthly expense, and depending on your income, you may qualify for housing assistance. This may come in two forms: 1) rent subsidy (where the government pays a portion of your rent), or 2) reduced rent housing. Both types of aid are based on your household income, and the number of people living in your house.[5]

- See if you qualify for federal housing assistance by using the HUD Website. [6]

- Also search for housing assistance in the state where you reside, which may also other assistance.[7]

-

2Apply for nutrition assistance. Like housing aid, the federal and most state governments also offer assistance to individuals or families with reduced incomes. Qualifying for aid is based on your household size and number of people living in the house, and the amount of assistance you qualify for can vary based on your income.

-

3Get healthcare help. A US government program is the Affordable Care program, which provides subsidized health insurance to low-income individuals or families. By enrolling for coverage, you will receive subsidized healthcare treatment, and have significantly fewer expenses should you or a family member experienced an unplanned medical event.

- You can apply for coverage during open enrollment, which starts November 1 before the year of coverage, and ends on January 31, in the year of coverage.[8] . (So for example, open enrollment for 2016 is November 1, 2015 — January 31, 2015.)

- You can also apply for healthcare assistance outside of the open enrollment period if you have life changes such as a marriage, birth of a child, loss of coverage, have a baby, or move to another area.[9]

-

4Apply for reduced utilities. Many local garbage, electric, gas, and cable services are operated by the government, and offer reduced prices for low-income individuals and families. If you qualify for any government assistance like housing or nutrition, you will likely also qualify for subsidized utilities. Check the websites of your local providers to learn about how you can save.

References

- ↑ http://energy.gov/energysaver/fall-and-winter-energy-saving-tips

- ↑ http://www.npr.org/sections/thesalt/2014/08/01/337141837/cheap-eats-cookbook-shows-how-to-eat-well-on-a-food-stamp-budget

- ↑ http://money.usnews.com/money/blogs/my-money/2014/03/18/15-items-always-worth-buying-in-bulk

- ↑ http://www.livingonadime.com/stop-eating-debt/

- ↑ http://portal.hud.gov/hudportal/HUD?src=/topics/rental_assistance

- ↑ http://portal.hud.gov/hudportal/HUD?src=/topics/rental_assistance

- ↑ http://portal.hud.gov/hudportal/HUD?src=/topics/rental_assistance/local

- ↑ http://obamacarefacts.com/obamacare-open-enrollment/

- ↑ https://www.healthcare.gov/get-coverage

About This Article