wikiHow is a “wiki,” similar to Wikipedia, which means that many of our articles are co-written by multiple authors. To create this article, 14 people, some anonymous, worked to edit and improve it over time.

There are 7 references cited in this article, which can be found at the bottom of the page.

This article has been viewed 977,436 times.

Learn more...

If you'd like to authorize someone else to handle money in your bank account, most banks give several options. You have the option to give the person financial power of attorney and specify which transactions they're allowed to make. Alternatively, you can change your account to give someone else access. Each bank has its own requirements and special forms you'll need to fill out, so it's a good idea to contact your bank directly to find out what method is best for your situation.

Steps

Granting Financial Power of Attorney

-

1Look into granting financial power of attorney for limited transactions. Most banks won't allow someone not listed on your account to make transactions in your name unless you have given explicit permission. In legal terms, this means granting the person financial power of attorney (FPOA) by signing a legal document stating what transactions the person is allowed to make. By giving someone FPOA, you can authorize them to make withdrawals, write checks for you, and take other actions in your absence.[1]

- A limited FPOA puts a limit on what the person can do with your account. You can authorize them to make a few specific transactions if that's all you want them to do.

- If you want the person to have longer-term access to your account, you can grant a durable FPOA. This enables the person to make decisions for you and handle your finances in the event that you become incapacitated.

-

2Contact your bank for a power of attorney form. Most major banks have a specific power of attorney form (sometimes called a third party authorization form) for you to fill out with the details of your situation.[2] You'll provide information on to whom you're granting power of attorney, which transactions you want the person to be able to take, and for how long they're authorized to have access to your account.

- Either visit your bank in person to speak to an agent, or visit your bank's website to obtain a power of attorney form online.

- Fill out and submit the form according to your bank's instructions.

Advertisement -

3Create your own power of attorney form. If your bank doesn't have a specific power of attorney form, you can create your own listing exactly what transactions the person is allowed to make. In order for the document to be legally valid, you will need to follow your state's laws in order to draw it up using the correct language. Execute (sign) the power of attorney form with the person to whom you're giving FPOA.[3]

- You may want to have a lawyer help you draw up the form to make sure it's legally sound.

- The execution of the document must also be done according to your state's laws. Some states require that you have a witness, and others require that you have the document notarized.

-

4Present the document to your bank. Once you have your forms filled out and signed according to the requirements of your state laws, visit your bank and meet with an agent to submit the form and make your intentions clear. Once the form is put on file, the other party will now be authorized to make the transactions you laid out.

Adjusting Your Account

-

1Consider opening a convenience account. About half the states in the US provide the option of opening convenience accounts. The other person would have access to the account, but would only be authorized to use it on your behalf. In other words, the person could use it to pay your bills, but they couldn't withdraw cash to use for their own purposes.[4]

- This is not an option in every state. See if your state's laws permit convenience accounts.

- Contact your bank to find out whether a convenience account will meet your needs.

-

2Look into adding someone as a co-owner. Every bank gives you the option of adding a co-owner to the account to create a joint account. This person would have the exact same ability to make transactions as you do. Go online or talk to a bank representative in person to add another person to your account.[5]

- In order to add a co-owner, you'll need to fill out forms that are signed by both parties.

- Once the forms are completed and submitted, the other person will be granted full access to the account.

-

3Use caution when allowing someone else full access to your account. Opening a convenience account or a joint account are both risky options. Adding a co-owner gives that person free reign to use your account in whatever way they please. Even if you just open a convenience account, you have to trust the person to use your money wisely. In either situation, be sure you have full trust in the person who has access to your account.[6]

- You may want to meet with a lawyer to discuss which option is best for your situation. The lawyer may advise you against getting a joint account, and instead recommend getting a durable FPOA. It's a good idea to think it through with an expert before making a decision.

- This is especially true if you're considering adding your children to your bank account so they can take care of your bills. Unanticipated problems could arise at a later time, so make sure your finances are well protected.[7]

Self-Authorizing Someone to Use Your Account

-

1Authorize someone to make a deposit. If all you want to do is allow someone to deposit money in your account, some banks allow people to do this without special authorization. Depending on what bank you use, you may not need to write an official letter or fill out any forms. Contact your bank for more information on its policies regarding third party deposits.[8]

-

2Authorize someone to make a withdrawal. Giving someone your bank card or account information is a way to self-authorize them to make a withdrawal. However, banks advise against doing this, since you won't have control over how much the person withdraws from your account. Some banks have explicit policies in place to prevent non-account holders from making transactions, so using FPOA or listing the person as a co-signer may be a better bet.

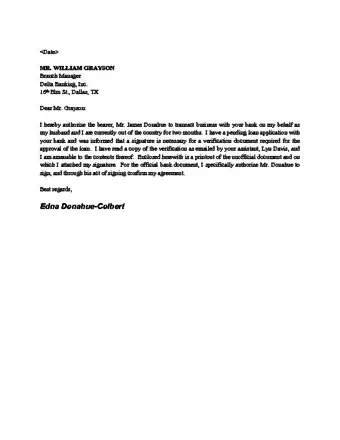

Sample Bank Letter

Community Q&A

-

QuestionHow do I write a bank authorization letter to close my account?

Community AnswerThat's not what a bank authorization letter is for. If you want to close your account, just call or visit your bank and ask to have your account closed.

Community AnswerThat's not what a bank authorization letter is for. If you want to close your account, just call or visit your bank and ask to have your account closed. -

QuestionI already have a joint account at my bank now. I want to add one account holder. What can I do?

Community AnswerGo to the bank with the person you want added to the account and have him/her bring two pieces of identification to show the bank. They will add the name to the account without having to change the checks if you wish.

Community AnswerGo to the bank with the person you want added to the account and have him/her bring two pieces of identification to show the bank. They will add the name to the account without having to change the checks if you wish. -

QuestionHow do I remove an old account from a new account to claim the pending funds?Community AnswerContact your bank for specific advice.

References

- ↑ https://www.legalzoom.com/articles/financial-power-of-attorney-how-it-works

- ↑ https://estate.findlaw.com/planning-an-estate/durable-financial-power-of-attorney.html

- ↑ https://info.legalzoom.com/grant-power-attorney-20090.html

- ↑ http://www.nolo.com/legal-encyclopedia/convenience-accounts-powers-attorney.html

- ↑ https://www.nerdwallet.com/blog/banking/joint-checking-account/

- ↑ http://www.nolo.com/legal-encyclopedia/convenience-accounts-powers-attorney.html

- ↑ https://generationslawgroup.com/should-i-add-my-adult-child-to-my-bank-account

- ↑ https://www.bankrate.com/banking/checking/cant-deposit-cash-into-someone-elses-account-these-are-your-options/

About This Article

To write a bank authorization letter, call or visit your bank to obtain a power of attorney form or third party authorization form. If you want someone to have limited access to your account, get a limited financial power of attorney form so you can specify what the other person will have access to. To grant someone more permanent access to your account, choose a durable financial power of attorney form instead. Once you have filled out the form, present it to your bank to get the authorization finalized. To learn how to add a second person onto your account, read on!