This article was co-authored by Michael R. Lewis. Michael R. Lewis is a retired corporate executive, entrepreneur, and investment advisor in Texas. He has over 40 years of experience in business and finance, including as a Vice President for Blue Cross Blue Shield of Texas. He has a BBA in Industrial Management from the University of Texas at Austin.

There are 7 references cited in this article, which can be found at the bottom of the page.

This article has been viewed 58,328 times.

Lines of credit are similar to loans, but have structural components that make them more complex. Where a loan is for a set amount, a line of credit is more like a credit card: you have a credit limit, and can withdraw funds from the credit line at your need and convenience. Where loans have a set payment each month that accounts for equity and interest, a line of credit's payment is different each time. These payments are based on a percentage of the total balance, making them easy to calculate once you understand how they work.

Steps

Understanding Lines of Credit

-

1Compare lines of credit to other types of financing. Lines of credit combine elements of credit cards and traditional loans. They are like credit cards in that you can only borrow up to a certain amount and can either use the money when you need it or choose to not use the money at all. However, the line of credit may have a maintenance fee until the credit line is borrowed upon and may or may not begin to charge interest immediately. Like a loan, a line of credit requires good credit to take out. However, a line of credit has more flexibility in both repayment and usage restrictions (it can usually be used at the borrower's discretion, provided the line's conditions have not been breached by the borrower in the interim period between the initiation date and the time the line is activated).

- Loans taken from a line of credit will also often have a minimum monthly payment, like a credit card.

- Lines of credit may or may not be secured by assets (like your home). Secured lines of credit are borrowed against the value of the asset on which they are secured. This means that the lender can seize the asset if you fail to repay your line of credit.[1]

-

2Determine if a line of credit is best for you. Lines of credit are best for purposes involving the payment of variable or unknown expenses. Many people use them for covering variable monthly expenses or dealing with fixed expenses when income may be variable. Alternately, they can be used for projects or events that can be difficult to price upfront (like home improvement projects). However, lines of credit are not best for fixed, single-item purchases, like a house or a car. Using a traditional loan would be cheaper in these instances.[2]Advertisement

-

3Know the downsides of lines of credit. Lines of credit can be great for unexpected or unpredictable expenses. However, they are more expensive than traditional auto or home loans because they charge higher interest rates and a possible initiation fee. That said, their rates are usually better than credit cards and are considerably better than payday loans. In addition, the interest on lines of credit is usually not tax deductible, except for lines secured by homes.

- Lines of credit may also charge certain fees, like a withdrawal fee. Check with the lender to see if this is the case with your line of credit.

- Sometimes the interest calculations used on lines of credit can be difficult to understand. You may end up paying more in interest than you expect.[3]

- Failing to repay a line of credit may also hurt your credit and keep you from getting loans or credit lines in the future.[4]

-

4Understand the different types of lines of credit. Lines of credit can be offered to either individuals or to businesses. For individuals, the types of lines of credit include personal and home equity lines of credit (HELOCs). HELOCs are secured against the value of your home and follow a specific structure of withdrawal and payment periods. Personal lines of credit, however, may be unsecured, and only require that you have good credit and a checking account with the lender.[5]

- Personal lines of credit can also be demand loans, meaning that the bank can request full repayment of the loan balance at any time.[6]

- HELOCs follow a unique repayment structure that is not discussed here. For more on HELOCs, see how to calculate an equity line payment.

Calculating Your Minimum Monthly Payment

-

1Determine the current balance of your line of credit. This is the amount you have currently borrowed on the account, not the limit of the line. You can find this on your most recent account statement, or by calling customer service for the bank that carries your credit line. This information will also be available on the bill for your monthly payment.[7]

-

2Find the basis for the monthly minimum payment. This will almost always be expressed as a percentage of the balance of the credit line. However, it may also just be calculated from outstanding interest. This is rarely on your monthly statements, but you can find it by calling customer service or by consulting the original documentation for your line of credit.

-

3Confirm that no finance charges, fees, or withdrawals are scheduled to come out of the account before you make your next payment. If some are scheduled, add them to the balance of the line of credit before you continue with the calculation. Fees may be charged for withdrawals, so make sure these fees are not pending on your account before calculating your payment.[8]

-

4Calculate the minimum payment. Multiply the balance of your line of credit by the basis for the minimum monthly payment. The result will be your minimum payment for that month.

- For example, if you had a payment basis of 2 percent on a line with a balance of $20,000, your monthly payment would be ($20,000 times 2 percent equals) $400.

- Your minimum payment will also be listed on your monthly bill.

- You may also be required to pay off the balance of your credit line account in full once per year.[9]

-

5Consider paying more than the minimum amount. You should avoid paying just the minimum amount on your lines of credit. You can save a surprising amount of money by paying more than the minimum each month on any loan or line of credit. The extra payment is applied directly to the principal, meaning the line of credit will accumulate less interest in subsequent months.

- For large loans, such as a home equity line of credit, this can mean paying off the line years ahead of schedule.[10]

Calculating Payments Needed to Repay the Line of Credit

-

1Learn the formula. When you're repaying a line of credit, it's important to set a timeline for repayment. The following formula will help you figure out how much you will have to pay each month to repay for your credit line balance within a certain number of months or years. The formula is: . In the formula, the variables stand for the following:

- P is the monthly payment. This is the result of the equation.

- r is the monthly interest rate. This is the annual interest rate divided by 12. The interest rate is also expressed as a decimal in the equation, so 0.5% would be 0.005 (0.5/100=0.005).

- PV is the present value, or the current outstanding balance on your credit line.

- n is the number of periods. This is the number of months in which you want to pay off your credit line. So, three years would be entered as -36 (3 years * 12 months/year).

- Note that this value is input as a negative number. This does not refer to a negative number of months, but is simply a mathematical construct.[11]

-

2Determine your variables. Two of the variables, r and PV, will come from your credit line's billing statement. Keep in mind that your interest rate, r, will have to be entered as a monthly interest rate. The only variable you will have to come up with is your repayment period, n. This can be any number you choose, but keep in mind that a larger value will result in smaller payments and a smaller value will result is larger payments (but less overall interest paid).

- For example, imagine you owe $10,000 on a line of credit with an annual interest rate of 6%. You want to pay the balance off within three years. So, your inputs are $10,000 for PV, 0.005 for r (6%/12 and then divided by 100 to get decimal form), and -36 for n.

-

3Calculate payments. Input your variables into the equation and then solve using the correct order of operations. The equation, completed using the example data, looks like this:

- First, solve the addition within parentheses (1+0.005). The example is now:

- Next, solve the exponent. This is done on a calculator by first entering the lower number (1.005 in this case), pressing the exponent button (usually ), and then entering the higher number (-36 here) and pressing enter. The example is now:

- Note that the result, 0.836, is a rounded figure. If you do not round, you may get a different result.

- Solve the multiplication in the numerator (0.005($10,000)). The example is now:

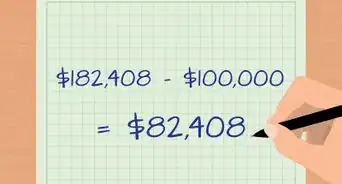

- Solve the subtraction in the denominator (1-0.836). The example is now:

- Finally, solve the division to get your answer. The answer solves to $304.87. So, your monthly payment will have to be $304.87 each month to pay off your $10,000 credit line balance in three years.

-

4Adjust payments as necessary. You can adjust the payment time to find an acceptable monthly payment or time schedule. Keep in mind, again, that a shorter repayment period will expensive as far as payments go but will be overall cheaper in interest paid (because interest has less time to accrue).

- If you have additional annual payments or monthly fees, or if your interest rate changes each year, you can use an online calculator to find your required payments.[12]

References

- ↑ http://www.consumerfinance.gov/askcfpb/901/what-personal-line-credit.html

- ↑ http://www.investopedia.com/articles/personal-finance/072913/basics-lines-credit.asp

- ↑ http://www.investopedia.com/articles/personal-finance/072913/basics-lines-credit.asp

- ↑ http://www.consumerfinance.gov/askcfpb/913/what-happens-if-i-do-not-pay-back-my-personal-line-credit.html

- ↑ http://www.consumerfinance.gov/askcfpb/901/what-personal-line-credit.html

- ↑ http://www.investopedia.com/terms/l/lineofcredit.asp

- ↑ http://www.consumerfinance.gov/askcfpb/911/how-do-i-pay-back-my-personal-line-credit.html

- ↑ http://www.consumerfinance.gov/askcfpb/901/what-personal-line-credit.html

- ↑ http://www.consumerfinance.gov/askcfpb/911/how-do-i-pay-back-my-personal-line-credit.html

About This Article