This article was co-authored by Jill Newman, CPA. Jill Newman is a Certified Public Accountant (CPA) in Ohio with over 20 years of accounting experience. She has experience working as an accountant in public accounting firms, nonprofits, and educational institutions, and has also honed her communication skills via an MA in English, writing jobs, and as a teacher. She received her CPA from the Accountancy Board of Ohio in 1994 and has a BS in Business Administration/Accounting.

There are 7 references cited in this article, which can be found at the bottom of the page.

This article has been viewed 623,823 times.

Not all loans are created equal. Understanding how to calculate a monthly payment, as well as the amount of interest you'll pay over the life of the loan, are very helpful in choosing the perfect loan for you. Understanding exactly how the money adds up can requires you to work with a complex formula, but you can also calculate interest more simply using Excel.

Steps

Quickly Comprehending Your Loan

-

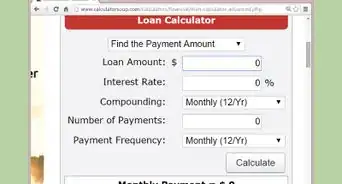

1Input your loan information into an online calculator to quickly determine your interest payments. Calculating interest payments is not a simple equation. Luckily, a quick search for "interest payment calculator" makes it easy to find your payment amounts as long as you know what to input into the calculator:

- Principal: The amount of your loan. If you loan is $5,000, the principal is $5,000.

- Interest: In simple terms, the percentage of money you're being charged to have the loan. It is either given as a percentage (such as 4%) or a decimal (.04).

- Term: Usually in months, this is how long you have to pay the loan off. For mortgages it is often calculated in years. Make sure to find out if there are any penalties for paying off the loan earlier than the stated term.

- Payment Option: Almost always a "fixed-term loan." However this can be different for specialty loans. Ask if the interest and payment schedule is fixed before getting a loan if you are unsure.[1]

-

2Find out your interest rate before getting a loan. The interest rate is the cost you pay for borrowing money. It is the rate of interest that you will pay on the principal for the life of the loan. You want it to be as low as possible, as even .5% of a difference can mean a huge sum of money.[2] If you would prefer lower payments, you may pay a higher interest rate and more total interest over the loan, but less each month. Someone with less savings on hand or whose income is bonus or commission-based would likely prefer this option. However, want to stay below 10% interest whenever possible. The common rates for different loans are:

- Auto: 4-7% [3]

- Home: 3-6%

- Personal Loans: 5-9%

- Credit Cards: 18-22% This is why you should avoid large purchases you can't repay quickly on credit cards.

- Payday Loans: 350-500% These loans are very dangerous if you can't pay them off within 1-2 weeks.[4] These loans are regulated by the state, which means that some of them have caps on the interest they can charge while others do not have a limit.

Advertisement -

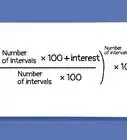

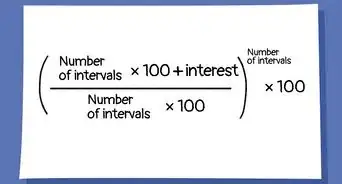

3Ask about accrual rates to determine when you get charged interest. In technical terms, the accrual rate tells you how often lender calculates the interest you owe. The more frequently you're charged the more you owe, since you have less time to pay off and the bill and prevent higher interest.[5] Look, for example, at a $100,000 loan with 4% interest, compounded three different ways:

- Yearly: $110,412.17

- Monthly: $110,512.24

- Daily: $110,521.28

-

4Use longer term loans to pay less each month, but more overall. The term is the period of time that you have to repay the loan.[6] Again, this will vary from one loan to the next, and you'll need to choose a loan with a term that meets your needs. If you are unsure about taking a shorter term loan with higher payments, then you can also always take out a longer term loan and pay a little more on the principal each month to cut back on the interest. A longer term will typically result in more interest paid over the life the loan, but smaller monthly payments.[7] For example, say you have a $20,000 auto loan with 5% interest. Total payment would be:

- 24 Month Term: You pay $1,058.27 in total interest, but only $877.43 each month.

- 30 Month Term: You pay $1,317.63 in total interest, but only $710.59 each month.

- 36 Month Term: You pay $1,579.02 in total interest, but only $599.42 each month.[8]

Calculating your Payment by Hand

-

1Learn the formula for complex interest payments. Despite all of the online calculators available for calculating payments and interest, understanding how interest and payments are calculated is essential for making an informed decision on your loans. Calculating your payments and interest requires the use of a mathematical formula, which is as follows: [9]

- The "i" represents interest rate, and the "n" represents the number of payments.

- Like most equations in finance, the formula for determining your payment is much more intimidating than the math itself. Once you understand how to set up the numbers, calculating your monthly payment is as easy as pie.

-

2Adjust for frequency of payments. Before you plug numbers into the equation, you must adjust your interest payment “i” for how often you are paying.

- For example, imagine you took out a loan at 4.5 percent, and the loan required you to make payments on a monthly basis.

- Since your payments are monthly, you will need to divide the interest rate by 12. 4.5 percent (.045) divided by 12 equals 0.00375. Plug this number in for "i."[10]

-

3Adjust for number of payments. To determine what to plug in for "n," your next step is to determine the total number of payments you'll be making over the term of the loan.

- Imagine that your monthly payments are on a loan with a 30 year term. To find the number of payments, simply multiply 30 by 12. You'll be making 360 payments.[11]

-

4Calculate your monthly payment. To figure your monthly payment on this loan, it is now just a matter of plugging the numbers into the formula. This might look intimidating, but if you go step by step, you'll soon have your interest payment. Below are the steps of the calculation, done one by one.

- Continuing with the example above, imagine you have borrowed $100,000. Your equation will look like this:

- $506.69. This will be your monthly payment.

-

5Calculate your total interest. Now that you have the monthly payment, you can determine how much interest you will pay over the life of the loan. Multiply the number of payments over the life of the loan by your monthly payment. Then subtract the principal amount you borrowed.[12]

- Using the example above, you'd multiply $506.69 by 360 and get $182,408. This is the total amount you'll pay over the loan's term.

- Subtract $100,000 and you end up with $82,408. That is the total amount of interest you'd pay on this loan.

Calculating your Interest with Excel

-

1Write down the principal, term ,and interest from your loan in one column. Fill separate boxes with the amount of the loan, the length you have to pay, and the interest, and Excel can calculate your monthly payments for you. For the remainder of the section, you can use the following example loan:

- You take out a $100,000 home loan. You have 30 years to pay it off at 4.5% annual interest rate.

-

2Write the principal in as a negative number. You need to tell Excel that you're paying a debt. To do so, write the principal with a negative number, without the $ sign.

- -100,000 = Principal

-

3Determine the number of payments you're making. You can leave it in years, if you want, but your answer would spit out yearly interest payments, not monthly. Since most loans are paid monthly, simply multiple the number of years by 12 to get your total number of payments. Write this down in another box.

- -100,000 = Principal

- 360 = Number of Payments

-

4Convert your interest rate to fit the number of payments. In this example, your interest rate is annual, meaning it is calculated at the end of the year. However, you're paying monthly, meaning you need to know what your monthly interest rate is. Since 4.5% is for 12-months of interest, simply divide by 12 to get one month's worth of interest. Be sure to convert the percentage to a decimal when you're done.

- -100,000 = Principal

- 360 = Number of Payments

- = Monthly interest.

-

5Use the =PMT function to determine interest payments. Excel already knows the equation for calculating monthly payments, with interest. You just have to give it the information it needs to make the calculation. Click on an empty box, then locate the function bar. It is located right above the spreadsheet and labeled "fx." Click inside of it and write "=PMT("

- Do not include the quotation marks.

- If you're Excel savvy, you can set up Excel to accept the payment values for you.

-

6Enter the inputs in the correct order. Place the values needed to calculate the payment in the parenthesis, separated by commas. In this case, you'll enter (Interest rate,number of periods,principal ,0).

- Using the example above, the full entry should read: "=PMT(0.00375,360,-100000,0)"

- The last number is a zero. The zero indicates you will have a balance of $0 at the end of your 360 payments.

- Make sure you remember to close the parenthesis off.

-

7Press enter to get your monthly payment. If you've entered the function correctly, you should see your total monthly payment in =PMT cell of the spreadsheet.

- In this case, you'll see the number $506.69. That will be your monthly payment.

- If you see "#NUM!" or some other output that doesn't make sense to you in cell, you've entered something incorrectly. Double check the text in the function bar and try again.

-

8Figure out the total payment amount by multiplying by your number of payments. To figure out the total amount you will pay over the life of your loan, all you have to do is multiply the payment amount by the total number of payments.

- In the example, you'd multiply $506.69 by 360 to get $182,408. This is the total amount you'll pay over the loan's term.

-

9Figure out how much you pay in interest by subtracting the principal from your total. If you want to know how much interest you'll pay over the term of the loan, this is just a matter of subtraction. Subtract the principal from the total amount you'll pay.

- In the example you'd subtract $100,000 from $182,408. You end up with $82,408. This is your total interest paid.

Expert Q&A

Did you know you can get expert answers for this article?

Unlock expert answers by supporting wikiHow

-

QuestionHow do I calculate a loan if the interest rate changes after six months?

Jill Newman, CPAJill Newman is a Certified Public Accountant (CPA) in Ohio with over 20 years of accounting experience. She has experience working as an accountant in public accounting firms, nonprofits, and educational institutions, and has also honed her communication skills via an MA in English, writing jobs, and as a teacher. She received her CPA from the Accountancy Board of Ohio in 1994 and has a BS in Business Administration/Accounting.

Jill Newman, CPAJill Newman is a Certified Public Accountant (CPA) in Ohio with over 20 years of accounting experience. She has experience working as an accountant in public accounting firms, nonprofits, and educational institutions, and has also honed her communication skills via an MA in English, writing jobs, and as a teacher. She received her CPA from the Accountancy Board of Ohio in 1994 and has a BS in Business Administration/Accounting.

Financial AdvisorCalculate the first six months of interest at that rate and add it to the principal. Then, continue your calculation using this amount with the adjusted rate of interest.

Support wikiHow by unlocking this expert answer.

-

QuestionHow do I calculate my interest payments monthly when I miss payments?Jill Newman, CPAJill Newman is a Certified Public Accountant (CPA) in Ohio with over 20 years of accounting experience. She has experience working as an accountant in public accounting firms, nonprofits, and educational institutions, and has also honed her communication skills via an MA in English, writing jobs, and as a teacher. She received her CPA from the Accountancy Board of Ohio in 1994 and has a BS in Business Administration/Accounting.

Financial AdvisorTypically when you miss a payment the monthly payment amount does not change, but you will be charged a late fee which could be a fixed amount or an amount per day until the payment is made. However, if you do need to calculate the interest on missed payments, you would add the principal amount from the payments you missed and then use that amount in your calculation with the monthly interest rate. A loan amortization schedule will show you exact breakdown of principal to interest for each payment.Support wikiHow by unlocking this expert answer.

-

QuestionHow do I calculate interest payments?

Michael R. LewisMichael R. Lewis is a retired corporate executive, entrepreneur, and investment advisor in Texas. He has over 40 years of experience in business and finance, including as a Vice President for Blue Cross Blue Shield of Texas. He has a BBA in Industrial Management from the University of Texas at Austin.

Michael R. LewisMichael R. Lewis is a retired corporate executive, entrepreneur, and investment advisor in Texas. He has over 40 years of experience in business and finance, including as a Vice President for Blue Cross Blue Shield of Texas. He has a BBA in Industrial Management from the University of Texas at Austin.

Business AdvisorAn interest payment is based upon the annual interest rate and the principal amount outstanding for the period. Presuming that you are making interest payments only on a term loan, divide the interest rate stated in the loan documents by the number of payments made in a year. Multiply the result times the principal outstanding. For example, if you have a $10,000 loan at 10% interest, your annual interest payments would total $1,000. If you make quarterly payments, you would pay $250 each quarter.Support wikiHow by unlocking this expert answer.

Reusable Spreadsheet to Calculate Interest Payments

The following table details how to use Excel, Google Docs, or similar spreadsheet programs to calculate simply interest payments on anything. Simply fill it in with your own numbers. Note that, where it says , you must fill this part in the upper bar of the spreadsheet labeled "Fx." The numbers (A2, C1, etc.) correspond to the boxes as they are labeled in Excel and Google Docs.

| A | B | C | D | |

|---|---|---|---|---|

| 1 | [Principal] | [Number of Payments] | [Interest] | [Interest per Month] |

| 2 | Negative Loan Amount (-100000) | Total number of payments, in months. (360) | Your interest rate, as a decimal. (.05) | Your monthly interest rate (divide yearly interest by 12) |

| 3 | Monthly Payment | FX=PMT(D2,B2,A2,0). NOTE: The final digit is the number zero. | ||

| 4 | Total Money Owed | FX=PRODUCT(D3,B2) | ||

| 5 | Amount Paid in Interest | FX=SUM(D4,A2) |

Warnings

- There are often times when the lowest rate advertised is not the lowest cost loan. When you understand how to the pieces to pricing these deals work, you can quickly understand the true “cost” of the debt versus the incremental price your paying for some of the features.⧼thumbs_response⧽

References

- ↑ http://www.interest.com/home-equity/calculators/monthly-payment-calculator/

- ↑ http://www.investopedia.com/terms/i/interestrate.asp

- ↑ http://www.bankrate.com/finance/auto/current-interest-rates.aspx

- ↑ http://econlib.org/library/Enc/InterestRates.html

- ↑ http://www.investopedia.com/terms/a/accrual-rate.asp

- ↑ http://www.investopedia.com/terms/t/term.asp

- ↑ http://econlib.org/library/Enc/InterestRates.html

- ↑ http://www.interest.com/home-equity/calculators/monthly-payment-calculator/

- ↑ http://www.fonerbooks.com/interest.htm

About This Article

information. The online calculator will ask for the principal, or the initial amount of your loan, as well as the interest and the term, or how long you have to pay the loan off. If you have any payment options, like a fixed-term loan, you will need to input this as well. To learn the formula for calculating interest payments online, keep reading.