This article was co-authored by John Gillingham, CPA, MA. John Gillingham is a Certified Public Accountant, the Owner of Gillingham CPA, PC, and the Founder of Accounting Play, Apps to teach Business & Accounting. John, who is based in San Francisco, California, has over 14 years of accounting experience and specializes in assisting consultants, bootstrapped startups, pre-series A ventures, and stock option compensated employees. He received his MA in Accountancy from the California State University - Sacramento in 2011.

There are 11 references cited in this article, which can be found at the bottom of the page.

wikiHow marks an article as reader-approved once it receives enough positive feedback. In this case, 100% of readers who voted found the article helpful, earning it our reader-approved status.

This article has been viewed 48,139 times.

Bookkeeping is the act of recording your daily business transactions.[1] You’ll need to record the money going out as well as the money coming in. Because documentation is key, you’ll need to get organized. Hold onto receipts, bills, and cancelled checks. Pay particular attention to your petty cash and remember to reconcile your accounts at least once a month.

Steps

Setting Up Your Accounts Payable

-

1Save proof of business expenses. Accounts payable is the amount of money you owe other people for business expenses. If you buy inventory or supplies, then you’ll need to collect proof of the expense. You’ll also need this information later at tax time. Save the following:[2]

- bills

- receipts

- bank statements

- credit card statements

- proof of payment

- any other documentary evidence

-

2Set up a spreadsheet or ledger. You’ll need create an electronic spreadsheet or ledger on a piece of paper. If you don’t want to do this yourself, there is bookkeeping software you can purchase that will make bookkeeping easy.

- Think about moving to an automated system when you’re receiving more than two bills a day or your expenses are increasing rapidly.

Advertisement -

3Create columns for necessary information. You’ll include the following information on your spreadsheet or ledger, so create a column for each:

- supplier’s name

- account number

- type of expense (e.g., office supplies, professional services, etc.)

- date you received the invoice

- amount you owe

-

4Post information daily. It’s important not to overlook accounts payable and forget to include them on your spreadsheet. Get in the habit of posting information daily.

- If you have few expenses, then you might want to post only weekly or monthly, but it’s key that you remember to develop a routine.

-

5Pay your bills in a timely fashion. Remember to pay bills frequently—on a weekly basis is ideal. Don’t wait until the due date. Instead, give yourself a few days in advance of the deadline.

- Paying bills early is a good way to maintain effective relations with your vendors.

- However, if you’ve been hired by a business to work as a bookkeeper, then paying on time is a necessity for maintaining your job.

Setting Up Your Accounts Receivable

-

1Create an invoice template. You want your invoice to be clear so that clients will pay as quickly as possible. Include the following information on your invoice:[3]

- your business contact information

- your business logo (if applicable)

- clear payment terms, such as “payment is due in 30 days of invoice date”

- detail about the specifics of your service

- hours worked

- the name a check should be made out to (particularly important if you operate under a fictitious business name)

-

2Save proof of payment and other documents. Just as you document your expenses, also document your accounts receivable. Hold onto the following, and create electronic copies if possible:[4]

- invoices

- cancelled checks

- other proof of payment

-

3Create a spreadsheet or ledger. You need something to enter your accounts receivable information onto. Choose a spreadsheet or a ledger book. Also consider using software. You can use the same software for accounts receivable that you use for accounts payable.

- If you are receiving 5-10 invoices a week, you should consider automating the system.[5]

-

4Insert columns for accounts receivable information. Set up columns for the following information on your spreadsheet or ledger:[6]

- customer name

- invoice date

- invoice number

- amount owed

- due date

- amount past due

- date payment was received

-

5Post information to your ledgers regularly. Get in the habit of staying on top of the amounts your customers owe you. You should post accounts receivable regularly, which will depend on the size of your business. The key is to get in a consistent habit so that you don’t forget.

- If you’re receiving multiple invoices a day, then posting daily is a good idea.[7]

- However, if you have only a few big invoices a month, then you might want to post monthly or weekly.

- Nevertheless, if you’re posting accounts payable daily, you should get in the habit of reviewing accounts receivable at the same time.

-

6Follow up on late payments. A bookkeeper also needs to track down customers who haven’t paid in a timely fashion.<> You’ll need to send appropriate letters telling the client their bill is due.

- If you find clients aren’t paying the business, you might want to talk with the owner about giving customers more options for making payment. For example, the business could accept credit cards.

Documenting Petty Cash

-

1Establish the starting balance. You can quickly lose track of where your petty cash has gone if you don’t keep accurate records. Accordingly, start with an initial balance. Make it small enough that your employees won’t feel tempted to steal from it but large enough that it can cover reasonable expenses.[8]

- Most small businesses can get by with $50-200 in petty cash.

-

2Require receipts. Keep careful records of what petty cash is spent on. Require your employees to provide receipts of all purchases made using petty cash.[9] Have a folder where you store receipts, and get in the habit of organizing receipts on a weekly basis.

-

3Create a log. You should also keep a log along with your receipts.[10] You need the log because not every purchase will have a receipt. On the log, record the amount taken from petty cash and what is was spent on. Enter the information immediately.

- For example, if you took $20 out to buy new pens for the office, you should enter the information as soon as you remove the money from the petty cash box. If you have money left over, then record that you are returning money to the petty cash box.

-

4Replenish by writing a check to yourself. This is a good way to document cash transfers. You can keep a copy of the cancelled check that shows which account you transferred money from. Don’t just take cash from your own wallet and dump it in the petty cash box.

-

5Enter petty cash information accurately on your balance sheet. Consider petty cash to be an asset on your financial statements.[11] Don’t neglect to accurately record it. Although the amounts may seem small, they can add up quickly for a small business.

Reconciling Your Accounts

-

1Keep ledgers for all financial accounts. You may have several business bank accounts. For example, small businesses usually have a checking account to pay bills and a savings account to save up money to pay self-employment tax.[12] You should also create a ledger or spreadsheet for each of your major accounts.

- Keeping this ledger will allow you to monitor the current state of your business. You won’t have to wait for the monthly bank statement to see if your business is insolvent or thriving.

-

2Reconcile your books. You need to make sure that your monthly recording of expenses is the same that shows up on your bank records. This means analyzing your bank statement and your accounts to make sure the same transactions appear on each.

- Reconciliation is a good way to catch mistakes—yours or the bank’s. If the bank makes a mistake, you can contact them. Share whatever documentation you have (receipts, cancelled checks).

- You can also catch fraudulent activity with reconciliation. For example, an employee might have withdrawn money from the checking account without telling you.

- Perform reconciliation monthly.[13] If you wait too long, it will be harder to reconcile. Also, you won’t catch fraudulent transactions in a timely manner.

-

3Meet with the accountant. You may need to meet with the company’s accountant once a month to go over the books. The accountant can identify any recordings that are unclear or inaccurate, and you can talk about them.

Expert Q&A

-

QuestionHow do I keep books for a small business?

John Gillingham, CPA, MAJohn Gillingham is a Certified Public Accountant, the Owner of Gillingham CPA, PC, and the Founder of Accounting Play, Apps to teach Business & Accounting. John, who is based in San Francisco, California, has over 14 years of accounting experience and specializes in assisting consultants, bootstrapped startups, pre-series A ventures, and stock option compensated employees. He received his MA in Accountancy from the California State University - Sacramento in 2011.

John Gillingham, CPA, MAJohn Gillingham is a Certified Public Accountant, the Owner of Gillingham CPA, PC, and the Founder of Accounting Play, Apps to teach Business & Accounting. John, who is based in San Francisco, California, has over 14 years of accounting experience and specializes in assisting consultants, bootstrapped startups, pre-series A ventures, and stock option compensated employees. He received his MA in Accountancy from the California State University - Sacramento in 2011.

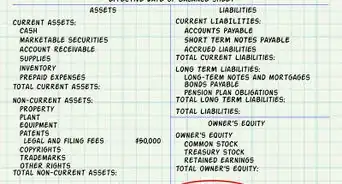

Certified Public AccountantWhen you're preparing the accounting for a small business, use the balance sheet as a check to help with the accuracy of the books. For example, when you look at the balance sheet, you should get an idea of the company's profits and losses, as well as the ending loan balances and how much the owner has invested in the business versus how much they've taken out.

References

- ↑ https://www.abetterlemonadestand.com/small-business-accounting/

- ↑ https://www.abetterlemonadestand.com/small-business-accounting/

- ↑ https://www.sba.gov/blogs/bookkeeping-basics-part-2-how-set-and-manage-accounts-receivable

- ↑ https://www.abetterlemonadestand.com/small-business-accounting/

- ↑ https://www.sba.gov/blogs/bookkeeping-basics-part-2-how-set-and-manage-accounts-receivable

- ↑ https://www.smartsheet.com/top-excel-accounting-templates

- ↑ http://www.nolo.com/legal-encyclopedia/bookkeeping-accounting-basics-29653.html

- ↑ http://quickbooks.intuit.com/r/accounting-money/dos-and-donts-for-petty-cash/

- ↑ http://quickbooks.intuit.com/r/accounting-money/dos-and-donts-for-petty-cash/

- ↑ http://quickbooks.intuit.com/r/accounting-money/dos-and-donts-for-petty-cash/

- ↑ http://quickbooks.intuit.com/r/accounting-money/dos-and-donts-for-petty-cash/

- ↑ https://www.abetterlemonadestand.com/small-business-accounting/

- ↑ http://fitsmallbusiness.com/bank-reconciliation-quickbooks-online/#

- ↑ https://www.abetterlemonadestand.com/small-business-accounting/

- ↑ https://www.entrepreneur.com/article/219917

About This Article

To do bookkeeping for a small business, start by creating a spreadsheet for accounts payables with columns for information like the supplier’s name, type of expense, and the amount you owe. Then, post your information and update your spreadsheet at least once a week so you can stay on top of your bills. You’ll also need to create an invoice template with clear terms, such as "payment is due in 30 days of invoice date," so you can ask clients for payment. Once a customer pays, file a copy of the invoice with the cancelled check or other proof of payment. To learn more, including how to document your petty cash and reconcile your accounts, read on!