This article was co-authored by Andrew Lokenauth. Andrew Lokenauth is a Finance Executive who has over 15 years of experience working on Wall St. and in Tech & Start-ups. Andrew helps management teams translate their financials into actionable business decisions. He has held positions at Goldman Sachs, Citi, and JPMorgan Asset Management. He is the founder of Fluent in Finance, a firm that provides resources to help others learn to build wealth, understand the importance of investing, create a healthy budget, strategize debt pay-off, develop a retirement roadmap, and create a personalized investing plan. His insights have been quoted in Forbes, TIME, Business Insider, Nasdaq, Yahoo Finance, BankRate, and U.S. News. Andrew has a Bachelor of Business Administration Degree (BBA), Accounting and Finance from Pace University.

There are 7 references cited in this article, which can be found at the bottom of the page.

This article has been viewed 122,730 times.

Bonds are a type of debt instrument used by corporations and governments to raise capital. Bonds are sold to investors, who are essentially lending money to the issuer in exchange for interest payments (called "coupon payments") at periodic intervals, usually every six months. Upon the bond's maturity, the holder is repaid the face value of the bond. There are several accounting treatments associated with the issuance of bonds. Issuers and purchasers must learn to account for bonds by understanding each transaction involved.

Steps

Accounting For a Bond Issue

-

1Set up a Bonds Payable account. When a corporation issues a bond, they are essentially taking out loans from bondholders. The bond issuer must then make accounting entries to recognize the receipt of cash and the amount owed to bondholders. The amount owed back to bondholders at maturity is recorded in an account called Bonds Payable. Open or update this account to record bond entries.[1]

-

2Record the appropriate book entries upon issuing the bond. The first accounting treatment occurs when the bond originates and warrants an entry in the accounting journal. If the bond has been sold at face value, rather at a premium or discount, the entry made is very simple. Record a debit to the Cash account and a credit to Bonds Payable, both for the total face value of the bonds issued.

- To record the sale of a $1000 bond, for example, debit Cash for $1000 and credit Bonds Payable (a long-term liability account) for $1000.

- The face value of the bonds represents the amount at which they will be redeemed or paid off at maturity. This can also be called the par, stated, or maturity value of the bond.[2]

Advertisement -

3Make entries to record a bond premium or discount. Bonds not purchased at par are purchased either above par, at a premium, or below, at a discount. Specifically, zero-coupon bonds (bonds that do not pay regular interest payments) are a type of bond offered at a discount. If the bond sells at a premium or discount, three accounts are affected.

- To record the sale of a $1000 bond that sells at a premium for $1080, for example, debit Cash for $1080. Then, Credit Bonds Payable for $1000 and Premium on Bonds Payable (a liability account) for $80.

- A similar entry is made if the bond sells at a discount. Consider a $1000 bond selling for $950. To record the sale, debit Cash for $950 and Discount on Bonds Payable (a contra-liability account) for $50, and credit Bonds Payable for $1000.

- Similarly, a zero-coupon bond is recorded as a bond sold at a discount. For example, a $2,000 zero-coupon bond might be sold at a discount for $1,780. This would be recorded as a debit to Cash for $1,780, a debit to Discount on Bonds Payable for the difference, $220, and a credit to Bonds Payable for $2,000.[3]

-

4Allow for issuance costs. A bond issue will likely incur addition costs to the corporation. These might include any legal expenses, commissions, printing expenses, and registration costs associated with the issue. These expenses are recorded as a debit to Other Assets and a credit to the Cash account for the total amount of the costs. They may then be amortized (recognized in regular increments) over the life of the bonds.

Making Entries Over the Bond's Life

-

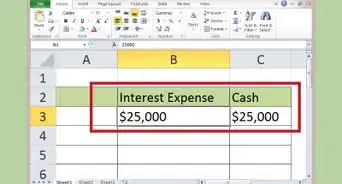

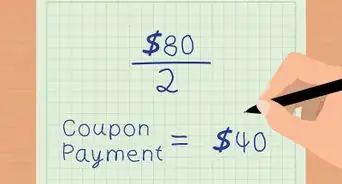

1Account for interest expenses. Many bonds make payments to bondholders known as coupon or interest payments. These are typically made either annually or semiannually and are calculated as the percentage of the bond's par value. The interest accumulating against the bond's face value must be recorded as it is incurred, and an entry must be made recognizing coupon payments. Consider a $1000 bond with a 12 percent coupon rate (for a total of $120 annually) that makes coupon payments semiannually.

- If the issuing company prepares financial statements annually or quarterly, the interest expense needs to be recorded only as the coupon payments are made. Using the previous example, there would be two entries per year in the general journal. Each entry would debit Interest Expense for $60 and credit Cash for $60.

- If the company prepares monthly financial statements, journal entries will also be needed each month to recognize the accrued interest. In the example above, each month the firm would debit Interest Expense for $10 and credit Interest Payable for $10.[4]

-

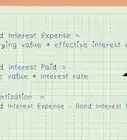

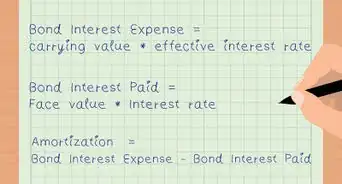

2Record the amortization of a discount or premium. If the bond sells above or below its face value, the discount or premium must be amortized (allocated to the income statement) evenly over the life of the bond.

- Consider a $1000 bond that sells for $1050 and has a coupon rate of 12 percent and a length of five years. When the bond is sold, the account named Premium on Bonds Payable will have a $50 credit balance. This balance needs to be amortized by the same amount each time a coupon payment is made.

- The amortization will be recorded in ten equal parts (semiannual payments for 5 years = 10 total payments). This means each part will be $50/10, or $5.

- When a coupon payment is made on the above bond, the journal entry will call for a debit to Interest Expense for $55, a debit to Premium on Bonds Payable for $5, and a credit to Cash for $60.

- An opposite entry is made to amortize a bond discount. Assuming the same bond terms but at a discount price of $950, the amortization would be recorded at each interest payment as a $65 debit to Interest Expense, a $5 credit to Discount on Bonds Payable, and a $60 credit to Cash.[5]

- A similar entry is made to account for zero-coupon bond interest. For example, imagine a zero-coupon bond sold at a discount for $1,780 with a face value of $2,000 and a duration of 2 years. This represent an annual "interest" rate of 6 percent.

- This 6 percent rate is recognized each year with a debit to Interest Expense and a credit to Bonds Payable, both in the amount of the interest that year. This would be $107 in year 1 and $113 in year two.[6]

-

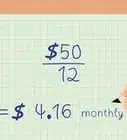

3Amortize bond issuance costs. Bond issuance costs may be also be amortized over the life of the bonds. To do so, divide the total issuance costs by the number of months until bond maturity and then recognize that amount each month in the Bond Issue Cost Expense account. When the bonds reach maturity, the issuance costs will be fully amortized.

- For example, imagine your bond issuance costs were $12,000 and your bonds mature in 5 years. Divide the $12,000 by the total number of months to maturity (60) to get the monthly expense, which would be $200.

- Each month, recognize a debit to Bond Issue Cost Expense (an Income Statement account) for $200 and a credit to Bond Issue Costs (a Balance Sheet account) for $200.[7]

-

4Make a journal entry at bond maturity. When the bond comes to maturity, the face value is given to the investor in cash. The journal entry for recording the maturation of a bond calls for a credit to Cash and a debit to Bonds Payable, both in the amount of the bond's face value. This holds true for bonds sold at a discount or premium as well, because the bond's book values will have been amortized to meet their face values at this point.[8]

- For example, a $1,000 bond's redemption would be recorded as a $1,000 credit to Cash and a $1,000 debit to Bonds Payable.

-

5Record bonds retired early. In some cases, it might be to the corporation's advantage to redeem bonds before their scheduled maturity. This means that the corporation will have to pay bondholders the "early call" price stated in the bond covenant. If the bonds were sold at a premium or discount, this could represent a loss or gain for the corporation. The gain or loss is calculated by determining the bond's current carrying value and subtracting it from the cost of early redemption.

- For example, imagine a bond with a par value of $1,000 that was sold at a premium that has been amortized down to $50, for a total carrying value of $1,050. The early call price is stated at $1,200.

- The loss on bond redemption would be the difference of these two prices, which is $150.

- The entries made would be debits to Bonds Payable for $1,000, Premium on Bonds Payable for $50, and Loss on Bond Redemption for $150. There would also be a credit to the Cash account for $1,200.[9]

Accounting For Bond Purchases

-

1Determine the bond terms. If a business or corporation purchases a bond, accounting entries must be made to record the purchase and subsequent payments. Start by determining the bond's terms, such as issue price (what you pay), face value (what the bond pays at maturity), and the frequency and amount of interest payments (if any). This information, along with other terms, will be listed in the bond covenant, which is a sort of investment agreement for bonds.

-

2Record the bond purchase. A bond purchase is recognized like other purchases a business might make. A debit is recognized to the asset account Investment in Bonds and a credit is made to the Cash account, both for the amount paid for the bond. This is true for bonds purchased at par, at a discount, or at a premium.

- For example, a $1,000 bond purchased at a premium for $1,050 would be recognized as a $1,050 debit to Investment in Bonds and a $1,050 credit to Cash.

- The Investment in Bonds Account is sometimes called Investment in Long-Term Securities so that other long-term securities may be included in the same account.[10]

- Bonds with a maturity date of less than one year are included in current assets. Long-term bonds are transferred from long-term assets to current assets in the year preceding their maturity.

- When they are transferred, bonds are valued at the lower of book value at the date of transfer and original cost.[11]

-

3Amortize discounts or premiums in interest payment entries. Interest paid to bondholders is recorded as an inflow of cash. The accounting entries made are a debit to Cash and a credit to Interest Income, both for the amount of the coupon payment. If a bond is purchased at a discount or premium however, interest should be recorded differently. The discount or premium is amortized over the life of the bond by either increasing or reducing the recognized amount of interest income.

- For example, imagine a $1,000, 3-year bond, that pays 5 percent interest semiannually. The bond was purchased at a premium for $1,060. The interest payment would be half of 5 percent of $1,000, or $25. However, the $60 premium must be amortized for $10 each time interest is paid because there are six total payments.

- So, the entries made would be a debit to Cash for $25 (the payment), and credits to Interest Income for $15 and Investment in Bonds for $10.

- For a discounted bond with the same terms sold at $970, the opposite entries would be made. This time, interest income would be increased from the $25 received to include some of the discount (specifically $5, as the $30 discount would be spread out over 6 payments).

- The entries made here would be debits to Cash for $25 and Investment in Bonds for $5, and then a credit to Interest Income for the sum, which would be $30.

-

4Make an entry to record bond redemption. Finally, when the bond reaches maturity and is redeemed by the bondholder, the bondholder must recognize the receipt of cash and the reduction in their Investment in Bonds account. Make entries for a debit to Cash and a credit to Investment in Bonds for the face value of the redeemed bonds.

Community Q&A

-

QuestionIn what account should government bonds be put?

Community AnswerGovernment bonds purchased by a business are placed into accounts according to their maturity. Very short term government bonds (with maturities under 3 months) are placed in cash and cash equivalents. Other bonds are recorded in the marketable securities account.

Community AnswerGovernment bonds purchased by a business are placed into accounts according to their maturity. Very short term government bonds (with maturities under 3 months) are placed in cash and cash equivalents. Other bonds are recorded in the marketable securities account.

References

- ↑ http://www.accountingcoach.com/bonds-payable/explanation/1

- ↑ http://www.accountingcoach.com/bonds-payable/explanation/2

- ↑ http://catalog.flatworldknowledge.com/bookhub/11?e=hoyle-ch14_s03

- ↑ http://www.accountingcoach.com/bonds-payable/explanation/2

- ↑ http://accounts.smccd.edu/nurre/online/chtr10fa.htm

- ↑ http://catalog.flatworldknowledge.com/bookhub/11?e=hoyle-ch14_s03

- ↑ http://www.accountingcoach.com/blog/bond-issue-costs

- ↑ http://accounts.smccd.edu/nurre/online/chtr10fa.htm

- ↑ http://accounts.smccd.edu/nurre/online/chtr10fa.htm

About This Article