This article was co-authored by Michael R. Lewis. Michael R. Lewis is a retired corporate executive, entrepreneur, and investment advisor in Texas. He has over 40 years of experience in business and finance, including as a Vice President for Blue Cross Blue Shield of Texas. He has a BBA in Industrial Management from the University of Texas at Austin.

This article has been viewed 298,602 times.

Bonds can be purchased from a government agency or a private company. When you buy a bond, you are loaning money to the issuer of the bond. This money, known as the "principal" of the bond, will be paid back after a certain number of months or years, when the bond is said to mature. In addition to paying back the principal, the issuer will make periodic interest payments to the bondholder until the bond reaches maturity. In order to determine how much those interest payments will be annually, semi-annually, or monthly, it is important to be able to calculate interest payments on a bond.

Steps

Understanding Bond Payments

-

1Learn what a bond is. Purchasing a bond can be thought of as purchasing debt, or, alternatively stated, loaning money to a company. The bond itself simply represents this debt. Like any loaned money, a bond entitles you to receive interest payments at fixed intervals for a specific time frame, at the end of which you will receive your initial amount back.[1] .

- Corporations and governments issue bonds to raise money to fund projects, or to finance their daily operations. Rather than simply going to the bank for a loan, issuing bonds directly to investors can sometimes be attractive since interest rates are lower, and bonds do not have the same amount of restrictions as bank loans.

-

2Learn the terminology for calculating a bond's interest payments. The world of bonds has its own unique terminology, and understanding these terms are necessary to be able to not only properly invest in bonds, but to calculate the interest payment of a bond.

- Face (or par) value. The face value of a bond can be thought of as its principal. That is to say, the amount you initially loan out, and that you expect to be paid back at the end of the bond's term.

- Maturity.The end of a bond's term is known as maturity. This is the date that the principle is to be returned to the investor of a bond. By knowing a bond's maturity, you can also understand the length of a bond's term. Some bonds for example are 10 years in length, others are 1 year, and some are as long as 40 years.

- Coupon. A coupon can be thought of as a bond's interest payment. A bond's coupon is typically expressed as a percentage of the bond's face value. For example, you may see a 5% coupon on a bond with a face value of $1000. In this case, the coupon would be $50 (0.05 multiplied by $1000). It is important to remember the coupon is always an annual amount.

Advertisement -

3Distinguish between a bond's coupon and a bond's yield. It is important to know the difference between a bond's yield, and a bond's coupon payment in order to not get confused when calculating interest payments.[2]

- Sometimes when you look at bonds, you will see both a yield and a coupon. For example, the bond's coupon may be 5%, and the bond's yield may be 10%.

- This is because the value of your bond can change over time, and yield is the bond's annual coupon payment as a percent of its current value. Sometimes bond prices go up and down, meaning the price of your bond can change from what your face value is.

- For example, pretend you purchased a bond with a face value of $1000. This bond pays you a 5% coupon, or $50 per year. Pretend now that the price of your bond dropped to $500 in the first year due to a change in interest rates in the marketplace. The yield would then be 10%. Since a bond's yield is the coupon payment as a percent of its current value, the coupon ($50) would be 10% of the current value ($500). As bond prices drop the percent yield goes up.[3]

- The reason bond market prices change is due to fluctuations in the market. For example, if long term interest rates rise from 5% (the coupon rate also) when the bond was purchased, the market price of a $1000 bond will fall to $500. Since the bond's coupon is only $50, the market price must fall to $500 when the interest rate is 10% to be marketable.

- While this may seem complex, you do not need to worry. This is because when calculating a bond's interest rate, you only need to worry about the coupon. If you noticed in both examples, while the percent is different, the payment is the same.

- Keep in mind that if you hold the bond until maturity and do not sell, you will receive back your principal, regardless of what happens to the price of the bond during the term.

Calculating Interest Payment on a Bond

-

1Look at the bond's face value. It is typically $1,000 or a multiple of that amount. Remember that the face value is the principal amount to be paid back when the bond reaches maturity.

- Pretend that in this case, the face value of the bond is $1000. This means you "loaned out" $1000, and expect $1000 back at the bond's maturity.

-

2Find the bond's "coupon" (interest) rate at the time it was issued. The rate is stated in the bond's paperwork. It may also be called the face, nominal or contractual interest rate.

- The coupon rate established when the bond was issued remains unchanged and is used to determine interest payments until the bond reaches maturity.

- In this case, assume the coupon is 5%.

-

3Multiply the bond's face value by the coupon interest rate. By multiplying the bond's face value by its coupon interest rate, you can figure out what the dollar amount of that interest rate is each year. [4]

- For example, if the bond's face value is $1000, and the interest rate is 5%, by multiplying 5% by $1000, you can find out exactly how much money you will receive each year.

- Remember when multiplying a number by a percent, to convert the number to a decimal. For example, 5% would be 0.05.

- $1000 multiplied by 0.05 would equal $50. Therefore, your annual interest payment is $50.

-

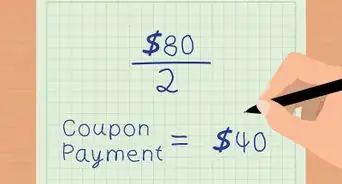

4Calculate how much each bond payment is. Interest is typically paid twice a year. [5]

- This information is stated when you purchase the bond.

- If a bond pays interest twice a year, the annual payment would be divided by two. In this case, every six months you can expect $25.

-

5Find the monthly interest. If the bond pays monthly, the exact same approach as above would be used, but the $50 would be divided by 12, since there are 12 months in a year.

- In this case, $50 divided by 12 is $4.16, which means you would receive $4.16 monthly.

- You earn the interest only for the days you own the bond. If you buy a bond between interest payments, the market price will include the interest owed to the previous owner for the days he or she held the bond.

Warnings

- Be aware that a bond may be "called" (or paid off before its maturity date). This tends to happen when current interest rates are lower than the rates prevailing at the time the bond was issued. The issuing company may decide to pay off the current bond and issue a new one at the lower rate to save themselves money on interest payments. The calling of a bond can be disruptive to a bondholder's plans for cash flow and will usually diminish the holder's income.⧼thumbs_response⧽

Things You'll Need

- Bond paperwork

- Bond's face value

- Coupon interest rate

- Time period for interest payments

References

- ↑ http://www.investopedia.com/articles/bonds/08/bond-market-basics.asp

- ↑ http://www.investopedia.com/university/bonds/bonds1.asp

- ↑ http://www.investopedia.com/ask/answers/020215/what-difference-between-yield-maturity-and-coupon-rate.asp

- ↑ http://study.com/academy/lesson/coupon-rate-definition-formula-calculation.html

- ↑ http://study.com/academy/lesson/coupon-rate-definition-formula-calculation.html

About This Article

To calculate the interest payment on a bond, look at the bond’s face value and the coupon rate, or interest rate, at the time it was issued. The coupon rate may also be called the face, nominal, or contractual interest rate. Multiply the bond’s face value by the coupon interest rate to get the annual interest paid. If the interest is paid twice a year, divide this number by 2 to get the total of each interest payout. If it’s paid monthly, divide the annual interest by 12. Keep reading for tips from our business reviewer on the difference between a bond’s coupon and its yield.